Government budget documents present wide-ranging data and information on how governments raise and spend resources. Most of these documents primarily focus on presenting numerical data about the sources of revenues and avenues of expenditure Some documents also provide information on other facets like the legal aspects of budgeting, on best practices, etc. Plans by the government to raise resources are based on analysis, projections and policy choices. Similarly, expenditure plans are based on several factors such as varying needs of different segments of the population, the political and economic landscape, and availability of resources. Given the range of information provided by government budgets, the entire set of budget documents can be categorised according to budgeting practices and functions. For example, the ‘Receipt Budget’ mentions various sources from which the government accrues money. However, its summary also appears in other documents such as ‘budget at a glance’ and ‘budget highlights’, etc. These documents provide the government’s projection of tax revenues for the upcoming financial year. However, changes in tax laws are mentioned in a separate document known as ‘Finance Bill’. Similarly, while the expenditure budget states the total amount to be spent on particular sectors or schemes, the targets of outputs, outcomes and indicators to measure the performance of schemes are given in another document called the ‘Outcome Budget Statement’. These examples highlight that a comprehensive understanding of the budget requires familiarity with budget documents as well as data and information reported in these documents. This chapter provides a list of all major documents associated with the budget along with corresponding explanations. It also identifies the sources where these documents – pertaining to both the Union and State governments – can be found.

Government budget documents can be divided into three broad categories

Main budget documents or statements: Essential to budgeting processes followed by the Union and State Governments, these documents are required by the Indian Constitution or mandated by Acts or laws passed by the legislature. Articles 110, 112 and 113 of the Indian Constitution outline requirements for such budget documents and statements. Further, the enactment of the Fiscal Responsibility and Budget Management (FRBM) Act requires governments to present a set of budget statements.

Supporting budget documents: Such documents provide additional information about the budget thus helping make budgetary information more precise, accessible, and understandable for common citizens. Though not constitutionally or legally required, these provide a more comprehensive picture of the budget.

Special budget documents – A result of specific government policies usually targeted at specific groups of the population or sectors. While the main provisions of these policies are already covered in ‘Main Budget Documents’, additional information is made available through special budget documents.

It is to be noted that the title and contents of some of these documents can change over time, reflecting changing budgetary practices or policy preferences of the government in power. Since state governments have independence over their budgets – barring the main budget document – other documents, statements, or reports presented in the second or third categories differ from state to state. The same document can also be differently titled across states.

Main Budget Documents

Of the following documents, the first four are constitutionally mandated while the fifth document is required by the FRBM Act.

i. Annual Financial Statement

Article 112 of the Indian Constitution lays down requirements for annual receipts and expenditure estimates which are placed before the lower and upper houses of Parliament (Lok Sabha and Rajya Sabha) for every financial year. These documents must provide expenditure categories mentioned in Article 112 which are to be incurred from the Consolidated Fund of India. This document is known as the ‘Annual Financial Statement’, or popularly known as ‘Budget’.

ii. Demands for Grants

While preparing the budget, the Ministry of Finance (MoF) asks all Ministries/Departments to prepare their planned expenditure for the upcoming financial year. Subsequently, these proposals are discussed among various branches of the executive, such as the MoF, concerned expenditure Ministries and Departments, economists and other relevant stakeholders. Finally, this process results in a document for each Ministry and Department, which provides detailed information about plans for expenditure along with a break up of different categories such as revenue versus capital, voted versus charged, schematic allocations, etc. These documents are then presented as a part of budget documents in Parliament or State legislative assemblies for discussion and vote. Such documents are known as ‘Demands for Grants’. Article 113 of the Constitution mandates that all proposals for expenditure be presented in the form of ‘Demands for Grants’ in Parliament or State legislative assemblies and should be voted upon. Demands for grants are presented or shared after the main budget (AFS) is presented for a detailed discussion.

iii. Finance Bill /Act

The ‘Finance Bill’ is a legal document presented along with the budget and contains the government’s proposals for changes in provisions for raising resources. A Finance Bill is a Money Bill as defined under Article 110 of the Indian Constitution. In each budget, along with expenditure, the Government also describes how it plans to raise resources. Such proposals contain changes in tax structure and other provisions which may affect the government’s resource raising abilities. For example, in the Budget 2021-22, the Finance Bill had provisions related to changes in rates of income tax, customs duty, central and integrated goods and services tax, the Life Insurance Corporation Act, Securities Contracts Regulation Act, etc. The changes in these provisions affect the nature and scale of resources that the government can raise in a particular year. The Finance Bill is put to vote before the legislature along with other budgetary documents. Its passage is essential for revenue proposals to be implemented. Once the Finance Bill is passed by both houses of Parliament according to procedures laid down by the Constitution and approved by the President / Governor of a State, it becomes the ‘Finance Act’.

iv. Appropriation Bill / Act

This is a bill introduced in the Lok Sabha/state legislative assemblies which contains provisions to enable the government to withdraw funds from the Consolidated Fund of India/ States for meeting voted expenditure during the financial year. After detailed discussions on various expenditure proposals and voting on demands for grants, the government introduces the Appropriation Bill in the Lok Sabha. The Appropriation Bill is a ‘Money Bill’, which deals with financial matters relating to expenditure needs of the Government as per Article 110 of the Indian Constitution. Once the Appropriation Bill is passed by both houses, it becomes the ‘Appropriation Act’.

v. Statement(s) as per FRBM Act, 2003

The Indian government introduced the Fiscal Responsibility and Budget Management (FRBM) Act in 2003 with a view to manage debt. This Act mandates the government to present the following documents in the budget.

Macroeconomic Framework Statement: This statement presents the government’s assessment of the economy as well as the rationale behind those assessments. It presents indicators such as growth rates of Gross Domestic Product (GDP), fiscal balance of the government and external sector balance.

Medium Term Fiscal Policy cum Fiscal Policy Strategy Statement: This presents the government’s forecast for key economic indicators for the upcoming three years, as well as the rationale behind those forecasts. Key economic indicators in this document include fiscal deficit, revenue deficit, primary deficit, tax revenue, non-tax revenue, etc. The document also explains that how government policies are in line with provisions of the FRBM Act - and in case policies do not correspond - how the government plans to respond.

Supporting Budget Documents

Such budget documents that are not required either constitutionally or by any other Act/ Law. Though, given the expansive and complex nature of the government budget, such documents help in simplifying the budget proposals. Also, since these are optional and not mandatory, these documents may or may not be available for all financial years. Also, their title and contents can vary between states and across years.

i. Budget at a Glance

This document briefly highlights receipts and disbursements along with broad details of tax revenues and other receipts. It also shows the revenue deficit, gross primary deficit and the gross fiscal deficit. Some indicators in the document include total expenditure and its breakup, total receipts and their major sources, collections from different taxes, sectoral expenditure, etc. This document is also known as Budget in Brief or Budget Summary.

ii. Budget Highlights

This is a summary document where the government chooses to highlight its major policy choices, achievements, major issues facing the country, etc. For example, the 2021-22 Union Budget included figures and trends for COVID-19 cases, Gross Domestic Product (GDP) trends during the COVID-19 pandemic, summary highlights of fiscal stimulus by the Union Government in reaction to the pandemic, as well as progress related to allocation for crucial ministries and schemes, length of roads, railways, metro rails built, etc. Budget highlights also include pictorial or graphical presentations of important budget information for citizens to access and understand.

iii. Budget Speech

When presenting the budget in the Parliament or State legislative assemblies, the finance minister delivers a speech comprising details of the government’s overall policy approach, achievements, the country’s economic situation, as well as major budgetary announcements – both for expenditure and receipts, etc. The Budget Speech document is the word transcript of the Finance Minister’s speech.

iv. Customs Notifications

In the case of international trade of goods, especially imports from abroad, countries impose a tax called customs tax or duty. Customs notifications provide the details of all such changes made to customs regulations as well as changes in the rates of taxes. In India, since it is the Union Government’s responsibility to frame customs regulations and also decide the rate of taxes on traded goods, these notifications are presented only in Union Budgets and not in State Budgets. Sometimes, these notifications are also accompanied by ‘Explanatory Notes’ which aim to make the notifications more precise or less ambiguous, and provide an easy and accessible explanation for the introduced set of changes.

v. Economic Survey

The Economic Survey is a document prepared by the MoF/ Department of Finance (at the level of State Governments) which provides details of the state of the economy for the ongoing financial year. The document is generally divided into two parts: the first part comprises the analytical or qualitative description of various sectors of the economy while the second part provides statistical data tables for all major sectors, as well as any other important data relating to socio-economic indicators. The first part is generally divided into various chapters focusing on a particular issue, topic or sector. For example - the Economic Survey for FY 2020-21 presented along with the budget for FY 2021-22 analysed issues like the impact of COVID-19 on the economy and livelihoods, relationship between debt and sustainability, India’s credit rating, healthcare in India, etc. The Economic Survey is an important document because along with relevant data, it provides insights into the government’s thinking and approach to different challenges and its strategies to address them.

vi. Expenditure Profile

The Expenditure Profile provides relevant data for all Ministries and Departments. The purpose of this document is to give an overall picture of the government’s financial performance. Along with information on expenditure planned by major ministries, it gives consolidated numbers for schemes, subsidies, investments, details of Public Sector Enterprises (PSEs), etc. This document also provides information about monetary allocations for important policies such as gender and child budgets, welfare of Schedule Castes/Schedule Tribes, etc.

vii. Expenditure Budget

The Expenditure Budget presents detailed information about the comprehensive expenditure which the government plans to incur in the upcoming financial year. Expenditure amounts are stated for each ministry as well further break up under each ministry. A brief explanation of each item under each Ministry is also presented in this document.

viii. Explanatory Memorandum

The Explanatory Memorandum is a document accompanying other budget documents or reports with the objective of simplifying and explaining content. Budget documents are often complex and consist of technical and legal details which are not easily accessible to lay persons. These explanatory memorandums or notes aim to make complex documents accessible in a non-technical language.

ix. Key to Budget Documents

This is an explanatory document which lists all budget documents presented in a particular financial year with corresponding explanations for each document. Such explanations help in differentiating between different documents and highlight specific objectives.

x. Receipts Budget

The government raises receipts from several sources. In each year’s budget, the government needs to provide a detailed explanation of the receipts it expects to raise from various sources. This document is known as the ‘Receipts Budget’. Crucial information in this document includes total tax revenues, revenues from individual taxes, total non-tax revenues and its major components, capital and receipts, borrowings, statement of revenues foregone due to tax incentives, liabilities of the government, etc.

Special Budget Documents

These budget documents are a result of the government’s policy choices and contain fiscal information and policy proposals for specific sectors, such as agriculture or climate change, or specific population groups such as women, children, Schedule Castes, Schedule Tribes, etc.

i. Agriculture Budget

The agriculture sector is significant to the Indian economy since it is the largest employer of labour. It is also important from the perspective of food security and population nutrition. Owing to its significance, some state governments present the ‘Agriculture Budget’ as a separate budget document in which major policies related to the agriculture sector as well as budgetary allocations are detailed.

ii. Child / Youth Budget Statement

Government budgets are multifaceted since they target multiple needs of various beneficiary groups. However, the varying needs of groups imply that one policy may not benefit all groups. Thus, policies must be designed considering the different needs of various groups. For example, the needs of children are different from other population groups. From a policy perspective, children’s need for nutrition, food and healthcare is different compared to the adult population. They are also more vulnerable to physical abuse. The differing needs of children require specifically formulated policy measures. Child budgeting is a policy framework where policies are designed according to specific needs of children. The child budget document or statement comprises such policies and also mentions corresponding policy allocations. In some cases, the scope of budgeting practices is expanded to include adolescent groups. In such cases, the document is known as ‘Youth Budget’.

iii. Climate Budget Statement

Climate change is one of the most defining challenges of the 21st century. There is global agreement that countries need to implement wide ranging measures to reduce the impact of climate change, much of which is on account of human actions. Climate budgeting is a policy framework which evaluates the impact of policy measures on climate change. By doing so, it either tries to minimise the negative impact on climate change, or explicitly tries to mitigate the effect of measures which contribute to climate change. The ‘Climate Change Budget / Statement’ details policies which fully or partially target climate change and related budgetary allocations.

iv. Gender Budget Statement

The overall goal of the government budget can be defined as welfare of the entire population. However, a country’s population is not homogenous and widely varies according to occupation, social hierarchies and access to public goods like health, education, employment, justice, etc. These differences become even more significant in the context of gender, especially in terms of employment opportunities, wages, education, access to healthcare, mobility in public space, responsibility of unpaid care work, types of crime committed against, etc. This means that the government must consider these differences while making policies to achieve desired outcomes for the population, especially women. Gender budgeting as a policy framework incorporates gender wise differences while framing policies. This may also be known as the ‘Women Component Plan’ which implies that either the entire policy is aimed at women, or that 30 per cent of the allocation, is allocated for women specific policy items. This document which gives details of such policy measures through schemes and programmes and the corresponding budget allocation and utilisation is known as ‘Gender Budget Statement’.

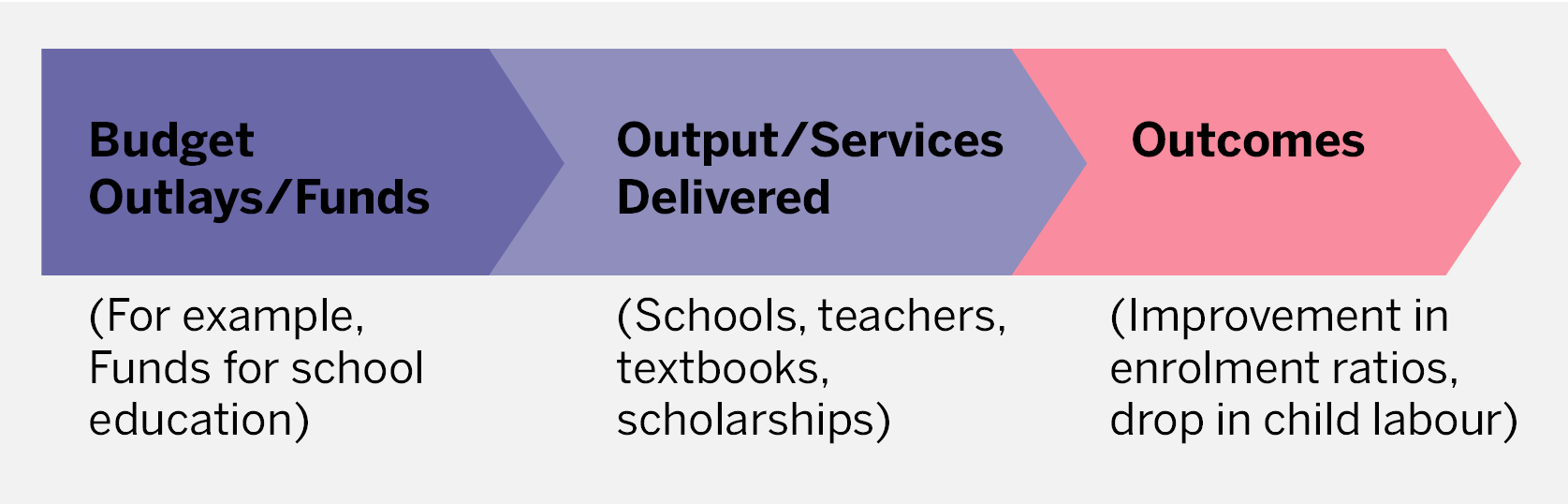

v. Outcome Budgets

Government policies aim to achieve specific objectives. For example – the main objective of education related policies is improving education levels of the targeted group. This entire process of policies achieving desired results is divided into three steps – inputs, outputs, and outcomes. Inputs refer to the policy design, budgetary allocation or outlays and the implementing agency. Output refers to the physical result of the policy while outcome refers to the desired impact on society. Ideally, when policies are properly implemented with adequate allocation, it leads to desired results. Let us take the example of the education scheme. Policies regarding education, schemes, budgetary allocation and the implementing agency (bureaucracy) consist of inputs. These inputs result in the creation of classrooms with teachers and other education related facilities, referred to as outputs. The outcome refers to improving education levels of the population in the geographic area of the school. Traditionally, governments have focused more on inputs and somewhat lesser on outputs. However, it is accepted that inputs do not necessarily lead to desired outputs. Similarly, outputs do not necessarily lead to desired outcomes.

Outcome budgeting is a policy framework which places the focus on policy outcomes. Budget inputs and outputs are accordingly designed. It also lists the desired outcomes of each policy in measurable terms, preferably within a specified time period, so that the policy is assessed in terms of success in achieving outcomes.

vi. Statement on Allocation for Welfare of Scheduled Tribes

Owing to the socio-economic deprivation and disadvantages suffered by Scheduled Castes (SCs) and Scheduled Tribes (STs), the Indian government has adopted measures and policies to reduce the deficit in development of these communities. The need was explicitly recognized by the Indian Constitution which mandates special protections and provisions for SCs and STs. An expert committee was set up in 1972 for preparing a comprehensive policy for protection, welfare and development of STs in India. This process gave birth to the Tribal Sub-Plan (TSP) strategy in 1976. TSP was adopted for the first time by the Fifth Five Year Plan to bridge the gap in socio-economic development indicators of STs in a time-bound manner. The TSP’s main objective was to channel Plan funds for development of ST communities according to their proportion in the total population. Under the TSP strategy, Plan funds were earmarked for STs under a separate budget head ‘796’ for each ministry implementing TSP. This was a strategy to channelise the flow of funds and benefits from general sectors, provided in the Union and state budgets, for the progress of STs. The erstwhile Planning Commission issued various guidelines for Ministries, States and Union Territories to form, implement and monitor the TSP. Current NITI Aayog guidelines specify new arrangements for earmarking funds under TSP where Union Government ministries must report the allocation of funds for STs in individual schemes. The Ministry of Tribal Affairs monitors the Scheduled Tribe Component (STC) of Ministries and Departments through an online monitoring system (http://stcmis.gov.in). These policy and budgetary provisions are documented in ‘Statement on Allocation for Welfare of Scheduled Tribes.’

vii. Statement on Allocation for Welfare of Scheduled Castes

In 1980-1985, during the Sixth Five Year Plan period, the Indian government adopted the Special Component plan (SCP) renamed as the Scheduled Caste Sub-Plan (SCSP) in April 2006. This was further renamed as Allocation for the Welfare of Scheduled Castes (AWSC) in February 2017. The SCSP’s main objective was to channel Plan funds for the development of SCs according to the community’s proportion in the total population. Under the SCSP strategy, Plan funds were earmarked for SCs under the separate budget head ‘789’ for each Ministry implementing the SCSP. After the Planning Commission was scrapped in 2014, funds are no longer divided into ‘Plan’ & ‘non-Plan’ categories. Instead, the NITI Aayog has formulated new guidelines for allocating funds to Scheduled Castes under the AWSC provision. The policy details and budgetary provisions are reported in a statement on ‘Allocation for Welfare of Scheduled Castes’.

In this section, the source of all data and documents mentioned in previous chapter are given. The sources have been arranged according to the governments, i.e. – first all the sources are given for Union Government, and then for all State Governments in alphabetical order.

Statement on Allocation for Welfare of Scheduled Castes

https://www.indiabudget.gov.in/doc/eb/stat10a.pdf

Statement on Allocation for Welfare of Scheduled Tribes

https://www.indiabudget.gov.in/doc/eb/stat10b.pdf

State Government

While each state government publishes its budget on its own website, not all states have same format, neither do all states publish all the documents mentioned in case of Union Government. Open Budgets India has compiled all state budget documents for recent years in one place, which can be accessed through following links –