The Indian political governance system is known as Federal System, in which power to raise resources, and the responsibilities towards public provisioning are divided across different tiers of governments. In India, this means that the political governance is organised at three levels – Central or Union Government, State Governments, and Local Governments which are also known as Local Bodies. Local Governments in India are entrusted with the governance of areas like a city, a town, a block, or a village. Local bodies can be put into two categories – Urban or Rural – depending on the area they govern. As the name suggests – Urban Local Bodies (ULBs) are the governance entity for the urban areas.

Types of Urban Local Bodies (ULBs)

There are three different types of ULBs depending on the type of urban area. They are –

Municipal Corporations / Nagar Nigam – For large urban areas

Municipal Councils / Municipalities / Nagar Palika – For smaller urban areas

Town Area/Notified Area Councils / Nagar Panchayats – For areas in transition from a rural to an urban area

It is up to the states to define the specifics of each three types of ULB. Meaning what constitutes a large urban area and what parameters define a small urban area – the Indian Constitution has left the responsibility to decide such specifics to the state governments. Hence, there are differences across states in terms of actual definitions of these terms. Generally, the criteria used for such definition are – population, population density, revenue for local administration, and proportion of workforce in non-agricultural activities.

While some form of local government, at least for urban areas have existed in India from the time of British rule, their functioning was ineffective or absent in most cases even after independence. One possible reason for this was that while the Constitution made elaborate provisions for Union and States, the significance given to local bodies was rather weak. Recognising their weakness, Constitution was amended in 1992, which made elaborate provisions about the power, role, responsibility, resource sharing, structure as well as the process of electing the representatives in these local bodies. These amendments provided constitutional authority to the local government.

What does the Constitution say?

The 74th Constitutional Amendment, carried out in 1992, made wide-ranging provisions about the responsibilities of the Urban Local Bodies. Article 243 of Constitution of India lists the authority and responsibility of the ULBs. They are

Urban planning, including town planning.

Regulation of land-use and construction of buildings.

Planning for economic and social development.

Roads and bridges.

Water supply for domestic, industrial and commercial purposes.

Public health, sanitation conservancy and solid waste management.

Fire services.

Urban forestry, protection of the environment and promotion of ecological aspects.

Safeguarding the interests of weaker sections of society, including the disabled and mentally retarded.

Slum improvement and upgradation.

degradationUrban poverty alleviation.

Provision of urban amenities and facilities such as parks, gardens, playgrounds.

Promotion of cultural, educational and aesthetic aspects.

Burials and burial grounds; cremations, cremation grounds; and electric crematoriums.

Cattle pounds; prevention of cruelty to animals.

Vital statistics including registration of births and deaths.

Public amenities including street lighting, parking lots, bus stops and public conveniences.

Regulation of slaughter houses and tanneries.

All these functions are divided into two categories – obligatory and optional/discretionary, and it is up to the states to decide which function to be put in which category. Because of this, there is a wide variance across States in terms of the assignment of overall functions and within that, obligatory and discretionary functions to the ULBs. Similar to Union and State Governments, ULBs also carry out their responsibilities through various schemes or services. Given this wide variation of functions assigned to ULBs by different states, across the country, it is difficult to generalise in terms of how these units of ULBs are spending their resources. Case study of two municipal corporations expenditure budget has been presented below.

South Delhi Municipal Corporation

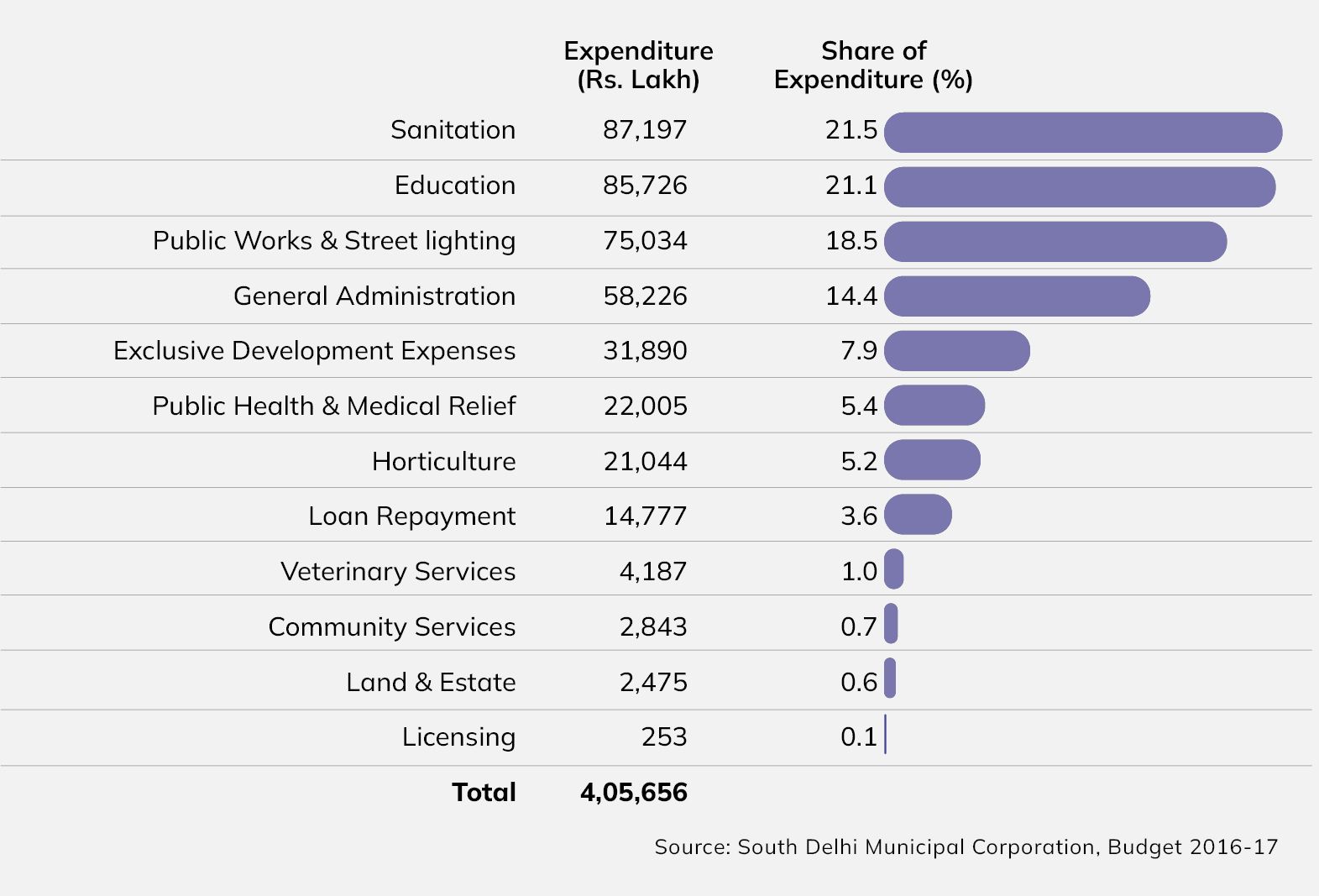

South Delhi Municipal Corporation (SDMC) is among the richest municipal corporation in the country helped by the fact that it is in the National Capital Region, and also the area under governance is economically well to do. Because of this, SDMC is able to raise resources much more than most MCs. Its expenditure statement is given in Figure 1.

Figure 1: South Delhi Municipal Corporation’s Expenditure for 2016-17 (Rs. Lakh)

Three biggest expenditure items are sanitation, education, and public works, with expenditure share of 21.5%, 21.1% and 18.5%, respectively. Further break up of these expenditure items is also available in the full budget. For example – on salaries, on maintenance, on buying new items, payments made to other entities, etc.

Bhubaneswar Municipal Corporation (BMC)

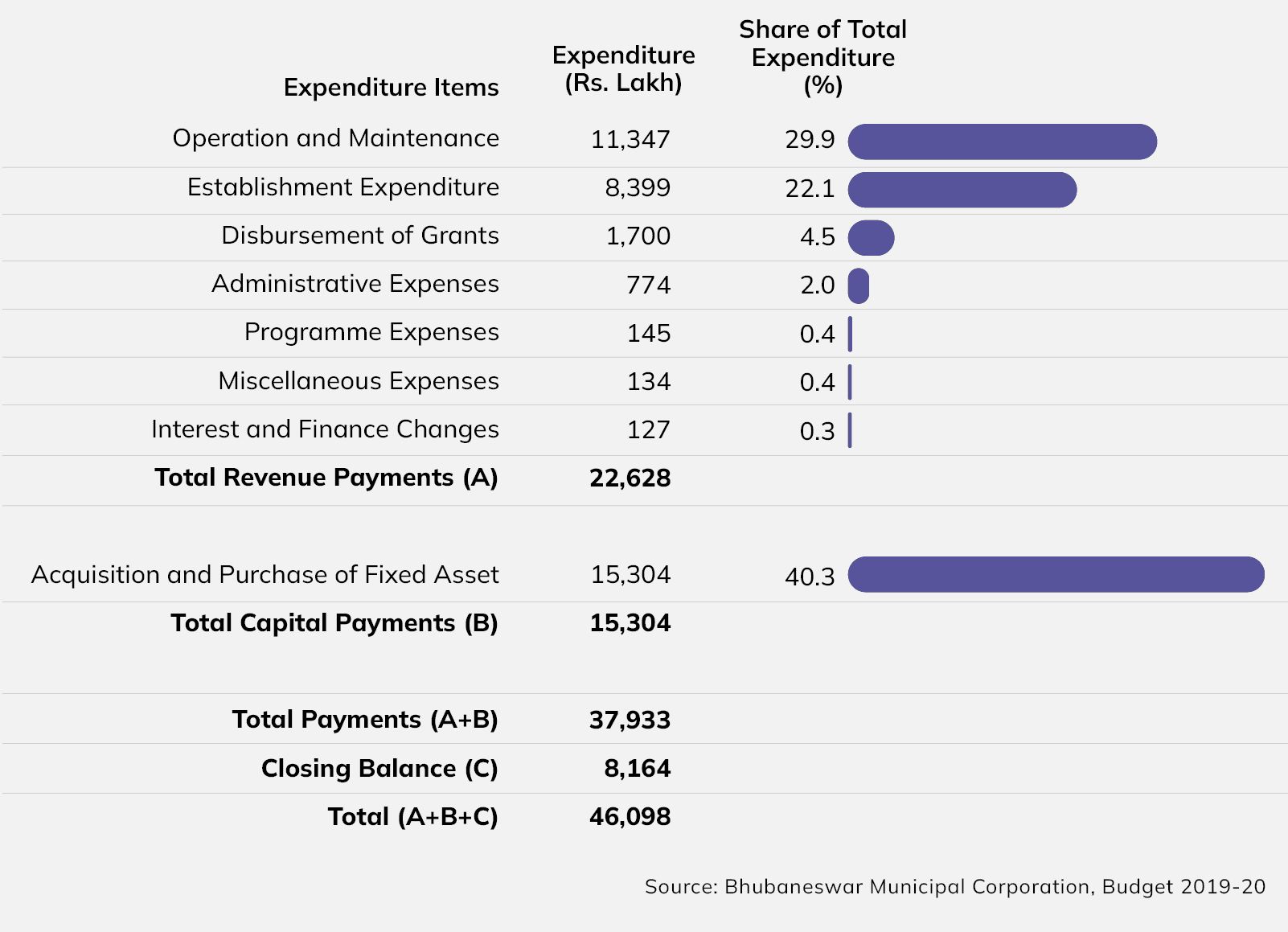

The implementation of various flagship programmes and schemes has enhanced the flow of resources to BMC in recent times which further reinforces the need for strengthening the delivery of basic services as well as infrastructural development in the ULB. The size of the expenditure budget of BMC displays an increase from approx. Rs. 3,500 lakh. in 2004-05 to Rs. 37,933 lakh in 2019-20.

Figure 2: Bhubaneswar Municipal Corporation’s Expenditure (Rs. Lakh)

Out of total revenue expenditure, which comprises 59.6 per cent of the total expenditure, operation and maintenance holds the biggest share (29.9%) followed by establishment expenditure (22.1%). Out of the total expenditure (A+B) for 2019-20 budget, 27.2 per cent has been allocated to the urban poor, leaving 72.7 per cent for the non-poor population.

The ULBs, depending on the area they govern, are pretty heterogeneous. As a result, their sources of receipts are also quite different. Nonetheless, there are some common sources which are applicable for all ULBs. This section first discusses the common sources and then uses the examples from two municipalities – South Delhi Municipal Corporation (SDMC) and Bhubaneswar Municipal Corporation (BMC). The examples have been chosen with the aim of having snippets from two very different municipalities, in terms of area, the scale of resource, etc.

Own Tax Revenue

MCs have the power to levy following taxes – • Property Tax – it is generally levied on non-movable property like land and building. The rate of tax is defined for a particular area. It is the largest sources of revenue for most municipal corporations in India. • Tax on Transfer of Property – It is levied when the immovable property in area under MC changes the ownership. In other words, it is levied on the sale of land and/or building. • Taxes on Vehicles – it is levied on the sale/use of vehicle within an MC. The rate is generally decided as the percent of price of vehicle. • Advertisement Tax – It is levied on the advertisement put on the property within a MC, but doesn’t include advertise on newspaper, TV or radio. Primarily, it targets the banners / hoardings for advertisement. • Toll Tax – also known as entry tax, is levied on certain vehicles when they enter the MC area. Which vehicle to be taxed and at what rate is decided by the respective municipal corporation. • Entertainment Tax – it is levied on the various forms of commercial entertainments, like – movie theatre, sports events, art exhibitions, amusement parks, etc. It is generally levied as a per cent of the ticket price.

Own Non-Tax Revenue

Major sources of non-tax revenues for ULBs are – • License fee: Earned by issuing trade licenses to private markets, cinema houses, slaughterhouses, burial grounds, commercial animal stalls etc. • Gate Fees: Entry fees obtained from the highest bidder, who, in turn, regulates entry based on certain fees. Major sources of gate fees are public markets, public parking and halting places, public slaughterhouses etc. • Income from Property (Rent): Rent from buildings, lands, cloakrooms, comfort stations etc. • Income from property other than rent: Proceeds from sale of rights to collect river sand, sale of rights to fish, sale of usufructs etc. • Permit fees: These are of two kinds – fee for building permits and fee for permits for the construction, establishment or installation of factories, workshops or workplaces where electricity is used. • Registration fees: Registration of hospitals and paramedical institutions, tutorials, births and deaths, contractors (only in Urban Local Governments), etc. • Service Charges: Charges collected for the use of utilities and amenities provided by Local Governments. Charges are levied on the direct recipient of a service.

Transfers from State Government

Among the many provisions, the 74th Constitutional Amendment Act, one was about the sharing of resources of States Governments with their respective local governments. Broadly, all transfers from state governments to the municipalities can be of two types – • Mandatory Shared Resources – based on the recommendations of the state finance commissions. It is generally the share in the divisible pool of resources raised by the respective states, where the divisible pool can be defined as per the state laws. • Discretionary Transfers/Grants-in-Aid: local bodies receive such aid from State Governments. There is no specific system of grants-in-aid, and these depend on the policies of the government of the day. The grants can also be given either to incentivise tax efforts or to match the effort in the maintenance of services.

Borrowing

Similar to Centre and State Governments, Municipal Corporations can raise resources by selling bonds in the open market. This is still a relatively underdeveloped area, as out of all MCs, only those having reasonably good amount of resources from own sources and credentials can raise resources through borrowing by selling bonds. In other words, the ability to sell bonds depends on the trustworthiness of MC that it will be able to repay in future.

Currently, only a few MCs raise money through borrowing. Nonetheless, there has been some development on this front, where MCs are encouraged to raise resources through this channel.

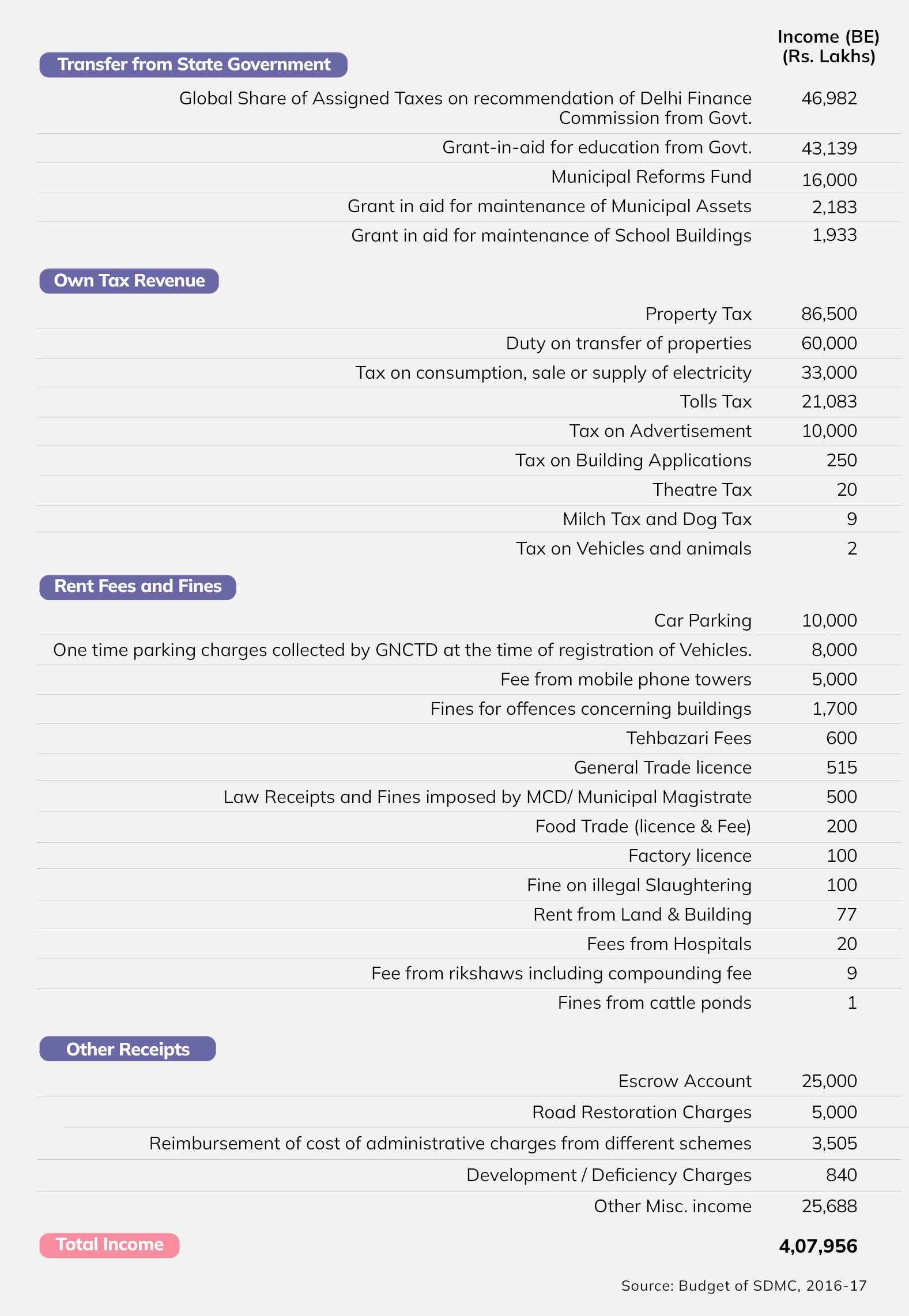

Receipt Budget of South Delhi Municipal Corporation (SDMC)

The sources of income for SDMC has been presented in table below –

Figure 3: Income of SDMC, 2016-17 (Budget Estimates) (Rs. Lakhs)

The four biggest sources of income for SDMC are – Property tax, Duty on transfer of properties, Tax share transfer from the state government, and Grants in aid for education with a share of 21%, 15%, 12% and 11% respectively.

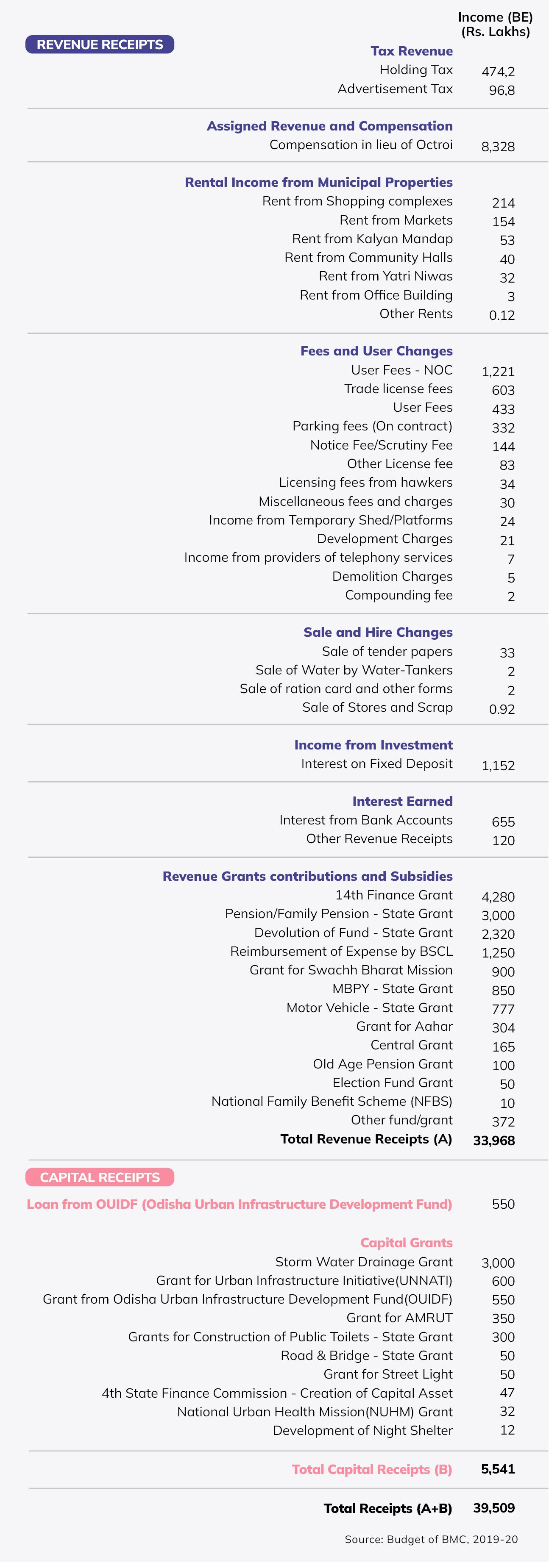

Bhubaneswar Municipal Corporation (BMC)

The major sources of income for BMC can be divided into revenue receipts and capital receipts. In 2019-20, under revenue receipts, the major share has been received from the revenue grants contributions and subsidies (36%) followed by assigned revenue and compensation (21%) and tax revenue (14 %). For capital receipts, significant share has been received from the state government grants, followed by the grants received from other government agencies and from the central government. The share of grants appears much higher in the BMC budget than the tax revenue generated, even though grants are not as much dependable a source as own tax revenues. The sources of income for BMC are given in Figure 4 below.

Figure 4: Income of BMC, 2019-20 (Budget Estimates) (Rs. Lakh)

A sizeable amount of the revenue is generated from revenue grants contributions and subsidies, followed by the local tax collected on certain goods when brought into the city for personal consumption (octroi) and its own tax revenues.

In the early 2000s, it was proposed that Municipality Budgets need to be presented in a structured manner so as to bring uniformity in the formats and codification of Municipality Budgets across the country. Accordingly, a National Municipal Accounting Manual - India was prepared, which proposed the codification structure to be used by Municipalities so as to facilitate capturing all types of financial information within an ULB. Subsequently, a number of States, such as Karnataka, Andhra Pradesh, have also developed their own accounting Manual.

The National Municipal Accounting Manual

The National Municipal Accounting Manual - India, recommended the following mandatory groups for all local bodies: • Functions: Functions are meant to represent the various functions or services carried out by the urban local body. • Account Heads: Account Heads are meant to represent the nature of the income or expenditure. In addition to these mandatory groups, there can be three optional groups in which Municipality Budgets can be presented. These are: • Functionary (Responsibility centre/department) – Municipalities are centered around their functions, which are provided through various responsibilities centres called departments. • Field (Geographical centre) - In order to monitor the geographical dispersion of these activities, many Municipalities identify their receipts/income and expenditure budgets at function, functionary (department) and field level. • Funds – Several Municipalities also set up various funds for meeting certain objectives. Receipts/ income and expenditure under these funds are to be identified and disclosed separately. In all, there can be five groups, namely:

Function

Account Heads

Funds

Functionary, and

Field

Function, Functionary and Field are called Budgeting centres. As per the manual, the first level in Function and Account Heads are mandatory for all Municipalities, and other levels are left to the states to define. The manual also noted that all ULBs are required to use the function codes and account codes as defined in the manual. For other levels, each State can define the codes “though some of them may be mandatory at the State level”. Similarly, the manual also noted that it is mandatory to budget for the functionary group, with the proviso that each State can define these heads based on its internal organisation structure. Similarly, States or cities, which have decentralised accounting zones/boroughs, etc. and prepare their budgets at these levels, are expected to use the field group as mandatory.

Issues in Budget Documents of MCs

From the tables given earlier about the budgets of SDMC and BMC, the difference in the scale of budget is clear. However, major difference between the two municipalities is also about how they report their expenditure. While SDMC also gives break-up of total expenditure into sector/issues, like heath, education, sanitation, etc.; BMC only provides the breakup in terms of function, and not in terms of sector/issues. Similarly, the reporting of income differs between the two MCs as well. While these are the examples from two MCs only, it is a much more prevalent issue. There is little to no consistency in the budgets reported by most MCs. Even when there are recommended formats, MCs don’t necessarily follow them.

Where the Municipal Budgets Need Improvement

Based on CBGAs’ work with a number of different MCs budget, following are the main issues in the budget document published by the MCs – • Incorrect classification – The building blocks of the budget are revenue receipts, revenue expenditure, capital receipts and capital expenditure. While a number of Municipalities follow the broad structure given in the above-mentioned manual when presenting their budget, there is a lot of variation in the way the details are presented across Municipalities. Likewise, even when a large number of Municipalities present revenue receipts and capital receipts separately on the receipts side and revenue expenditure and capital expenditure separately on the expenditure side, in their budget documents, there are some Municipalities which do not make such differentiation and provide data only for overall expenditure and receipts (e.g., Ludhiana). • Incorrect Codes – the codes used for various heads of expenditure and receipts vary from Municipality to Municipality and do not necessarily follow the code structure given in the National Municipal Accounting Manual: India. • Unreadable Docouments – While it can be assumed that the doumcents are prepared at least in some stage in the electronic form, and hence simply uploading this final documents would be easily readable, that is not the case with many municipalities. There are municipalities which upload documents that are not in machine readable form, and there are MCs which upload the document after scanning the hard copy, but done in a manner that the content of document is not clear. In such cases, they are not only unreadable by machines, but even by human eyes. • Time Lag – in case of many MCs, there are large gaps between the budget presentation and legislative approval, and the availability of same document for public, at least online. The quality of budget reporting is one place where local bodies fall far behind from not only the standards of Union Government and State Governments, but also from the minimum standard of budget transparency.