The government of a democratic country works to achieve multiple objectives at the same time. For instance, while the government works towards achieving economic growth, it must also ensure that the fruits of this growth are distributed equitably and reach the marginalised sections of the population. Budgetary strategies are formulated with a view to fulfilling competing needs with limited resources

What is a Budget Strategy?

The set of budgeting practices followed by the government keeping in mind specific sectors, population groups, or targeted outcomes, are called budgetary strategies. These strategies constitute some of the public finance management (PFM) tools used to address the concerns of sectors of the economy or sections of the population.

What are some of the main Budgetary Strategies?

Broadly, all budgetary strategies can be divided into three broad categories –

Focused on a particular population group - examples include Gender Budgeting which is also known as Gender Responsive Budgeting (GRB), Budgeting for Children which is also known as Child Responsive Budgeting (CRB), and Budgeting for Scheduled Castes and Scheduled Tribes.

Focused on a particular sector / geography – examples include Budgeting for Nutrition, Agriculture and Green Budgeting or Budget for Climate Change Actions. There are recent initiatives on budgeting for Sustainable Development Goals, District Budgeting, and Budgeting for Panchayats.

Focused on efficiency and/or effectiveness of budgetary practices – these strategies arenot restricted to any specific sector or population groups but span across various categories. Examples include initiatives on Outcome Budgeting and Budgeting for Sustainable Development Goals.

This chapter discusses some important budget strategies, their significance, and how they are being carried out by the Union and the State governments. It also provides information on special budgets, also known as special budget statements.

Women grapple with a range of structural disadvantages within various domains such as health, education, nutrition, and employment. They also face barriers to participation in governance, politics and other socioeconomic opportunities. Transgender persons also face a number of challenges in different domains. Budgets can be an effective tool to address many of these concerns of sexual and gender minorities including women and transgender persons.

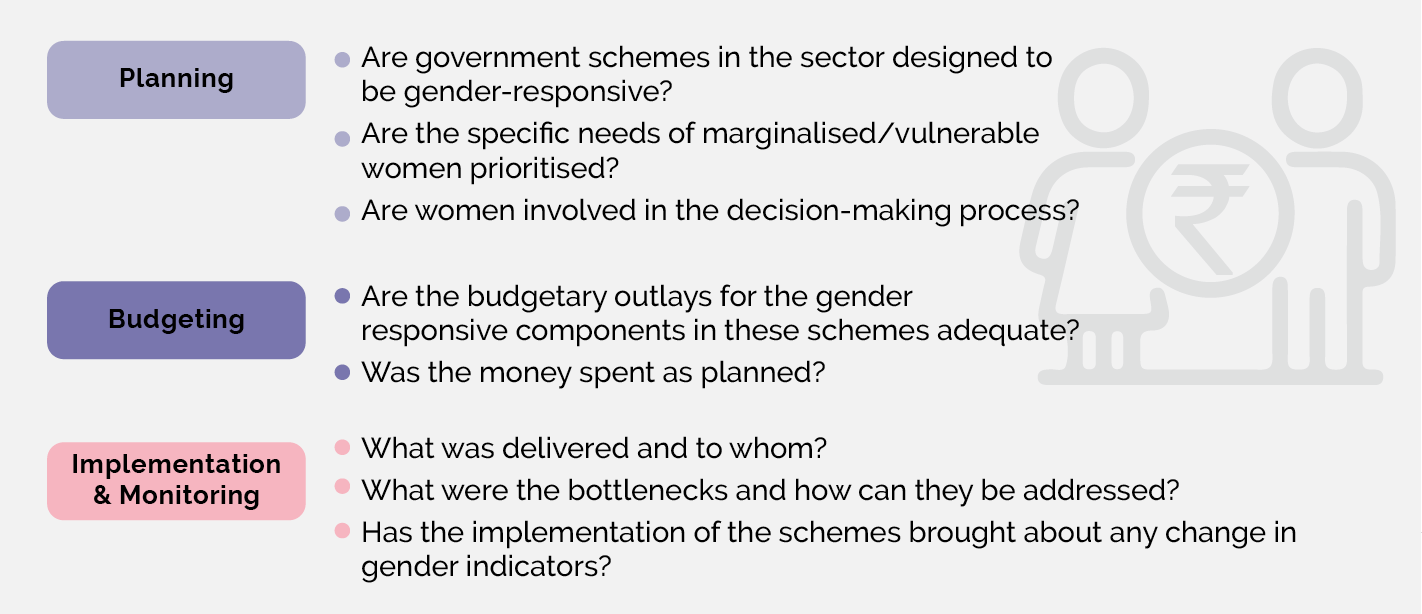

Gender Budgeting or Gender Responsive Budgeting (GRB) is a strategy comprising a range of tools that governments at all levels can use to address gender concerns. It involves applying a gender perspective to the entire policy process for translating the government’s commitments on gender issues into budgetary outlays. It is a strategy that, ideally, runs through all the stages of a budget cycle, i.e., planning, budgeting, implementation / monitoring, and review / audit. GRB is aimed towards ensuring that governments allocate and spend money in a manner that recognises the needs of women and gender minorities, removes barriers they may face, and improves their overall status. According to the Ministry of Women and Child Development, “Gender Budgeting is concerned with gender-sensitive formulation of legislation, policies, plans, programmes and schemes; allocation and collection of resources; implementation and execution; monitoring, review, audit and impact assessment.”

The following infographic explains how GRB can be applied to the different stages of a budget cycle.

Figure 1: How Gender Budgeting is carried out across various stages of a budget cycle

Why is there a need for Gender Responsive Budgeting?

While women’s issues have received policy attention over the years, they continue to experience various forms of socio-economic deprivations following their intersectional disadvantages. To illustrate, only 47 per cent of women worldwide participate in the labour force compared to 74 per cent of men. In India, 30 per cent of women report having suffered some form of domestic violence; and only 13 per cent of women who suffer any physical or sexual violence seek help. As many as 53 per cent of Indian women of reproductive age are anaemic. Experts suggest that at the current rate, it will take more than 135 years to close the gender gap globally.

The numbers quoted above are reflective of the fact that women often do not have equal access to the benefits and opportunities created by economic growth and development. The problem is especially compounded for women from marginalised communities who tend to be intersectionally disadvantaged. Public provisioning of services in different sectors including health, education, work participation, and social protection by the government plays a critical role because many women get the opportunity of availing these services, otherwise inaccessible to them, from government funded schemes and programmes. Gender Responsive Budgeting is, therefore, a strategy to ensure that governments adequately fund and effectively implement programmes with the potential to improve gender outcomes.

What are some of the Tools and Strategies used in Gender Responsive Budgeting?

Some of the commonly used GRB tools in India are:

Dedicated Institutional Structure: To take forward the initiative of gender budgeting, a dedicated committee or cell can be instituted within the government that works on making budgets gender responsive;

Legal Provisions: Certain legal provisions have been put in place which makes it mandatory to earmark a certain portion of the budget for women;

Disclosure Documents: An annual Gender Budget Statement which presents the funds allocated for women and girls has been published in many instances;

Capacity Building: Trainings and workshops are conducted to make government officials more gender sensitive and orient them about the need for GRB;

Gender Disaggregated Data: Efforts have been made to collect gender-disaggregated data to monitor impact and improve the design of government programmes.

How has GRB been carried out in India?

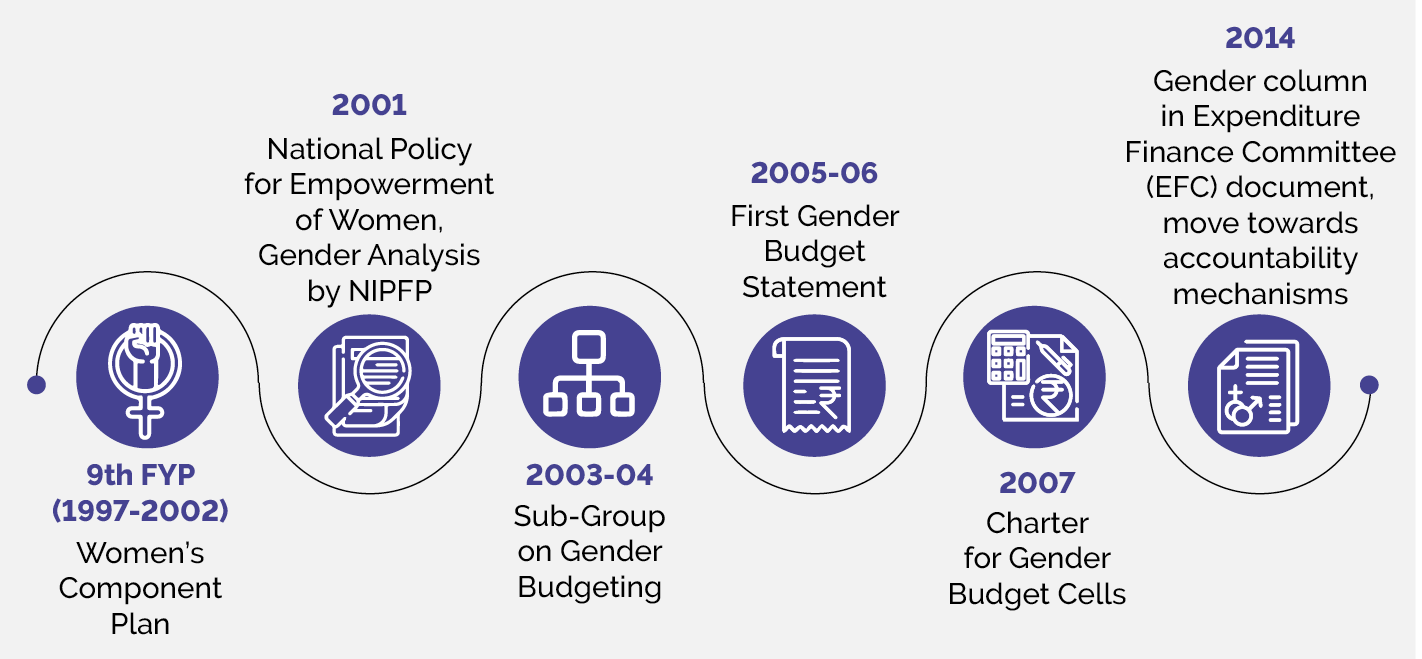

In 2005-06, the Government of India brought out its first Gender Budget Statement which has been part of the Union Budget documents every year since then. In 2007, India began setting up Gender Budget Cells within select Union Ministries. Since then, there have been initiatives to evaluate expenditure and budget outcomes from a gender lens. A number of training sessions have been held to orient officials towards practising GRB. A timeline with major milestones in the journey of GRB in India has been depicted in figure 2.

Figure 2: Major milestones of Gender Responsive Budgeting in India

The Government of India has initiated a number of GRB practices. These include:

Formation of Gender Budget Cells: - Gender Budget Cells have been createdacross 57 Union Ministries/Departments. These are supposed to integrate gender perspectives into budgeting processes and oversee other GRB initiatives.

Capacity Building – Capacity buildinginitiatives such assensitisation and training workshops have been carried out for government officials at the Union and the State levels, and for the nodal government representatives attached to Gender Budget Cells.

Knowledge Products: Handbooks, training manuals and other such resources have been developed as knowledge products in the domain of GRB.

Accountability Mechanisms: A gender perspective has been included in documents such as the Output Outcome Framework to strengthen the accountability mechanisms.

Publication of Gender Budget Statements: Gender Budget Statements have been published alongside the main Union Budget documents every year.

What is a Gender Budget Statement (GBS)?

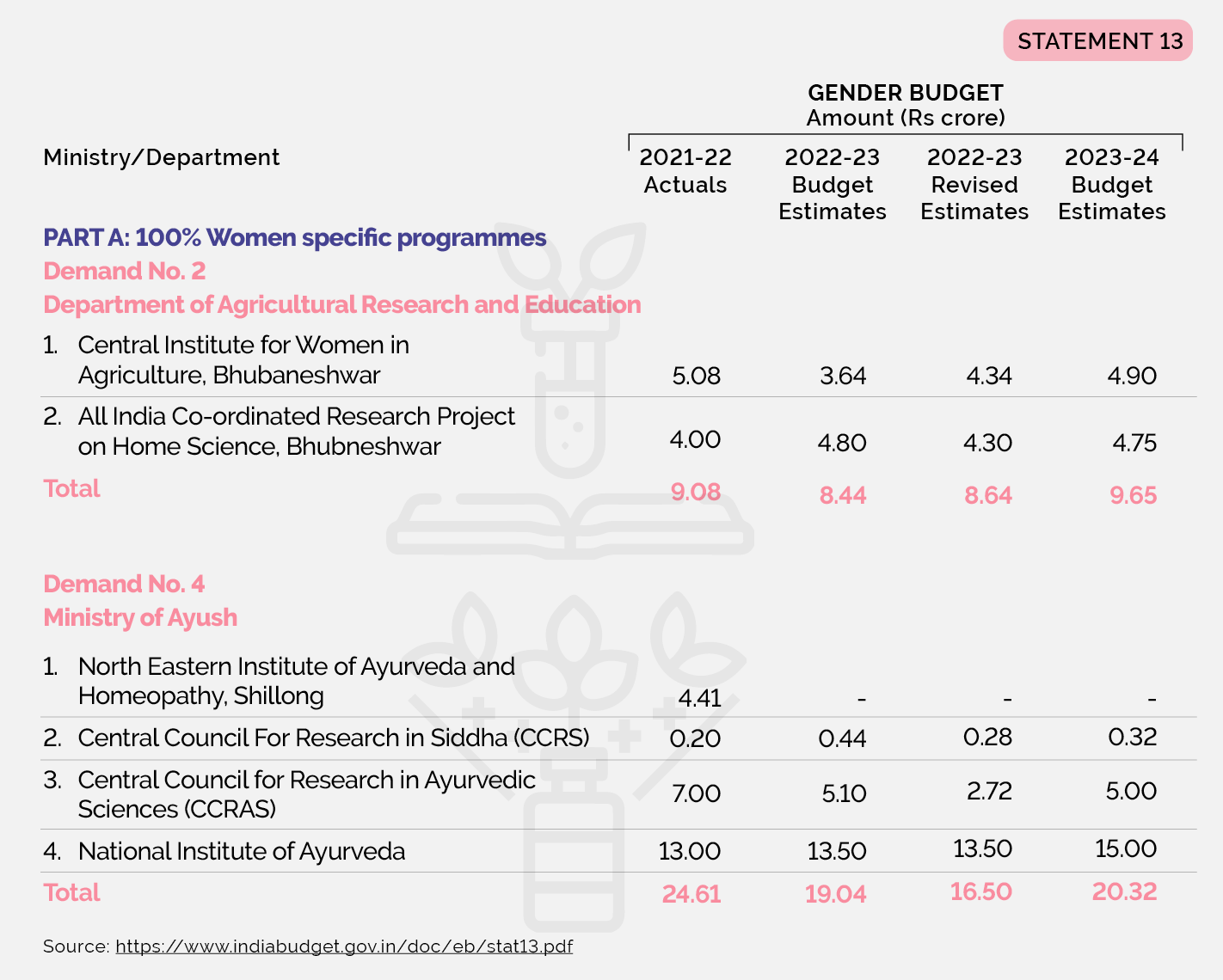

The GBS is one of the most commonly used tools to implement GRB in India. Since 2005-06, it is published every year along with the other documents of the Union Budget of India. It is compiled by identifying, categorising and listing the budgetary allocations and expenditures which are meant to address gender concerns from the main budget. It should be emphasised that a GBS is not a separate budget, but a part of the annual budget publications. It can be located under Statement 13 of the Expenditure Profile section of the Union Budget. It has been segregated into two parts – A and B.

Part A shows the budget for schemes which are exclusively targeted at women and girls, i.e., schemes with 100 per cent of their budget allocation for them (e.g., Beti Bachao Beti Padhao scheme)

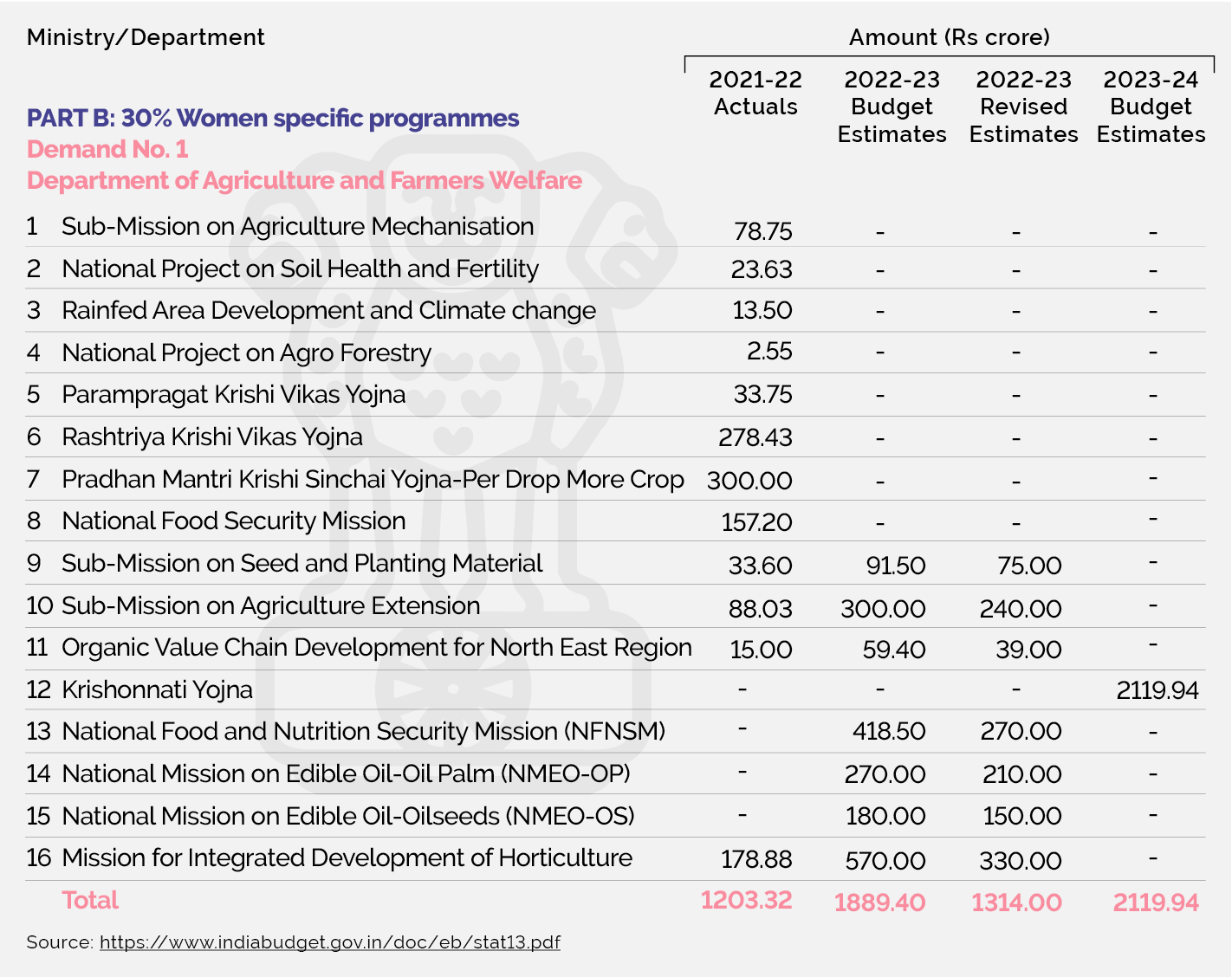

Part B shows the budget for schemes targeted partially at women and girls, i.e., schemes with 30-99 per cent of the total allocation earmarked for them (e.g., part of the budget for MGNREGS allocated for women workers)

Figure 3: Gender Budget Statement (Part A) of the Union Government for the Year 2023-24

Figure 4: Gender Budget Statement (Part B) of the Union Government for the Year 2023-24

Which States have adopted Gender Responsive Budgeting?

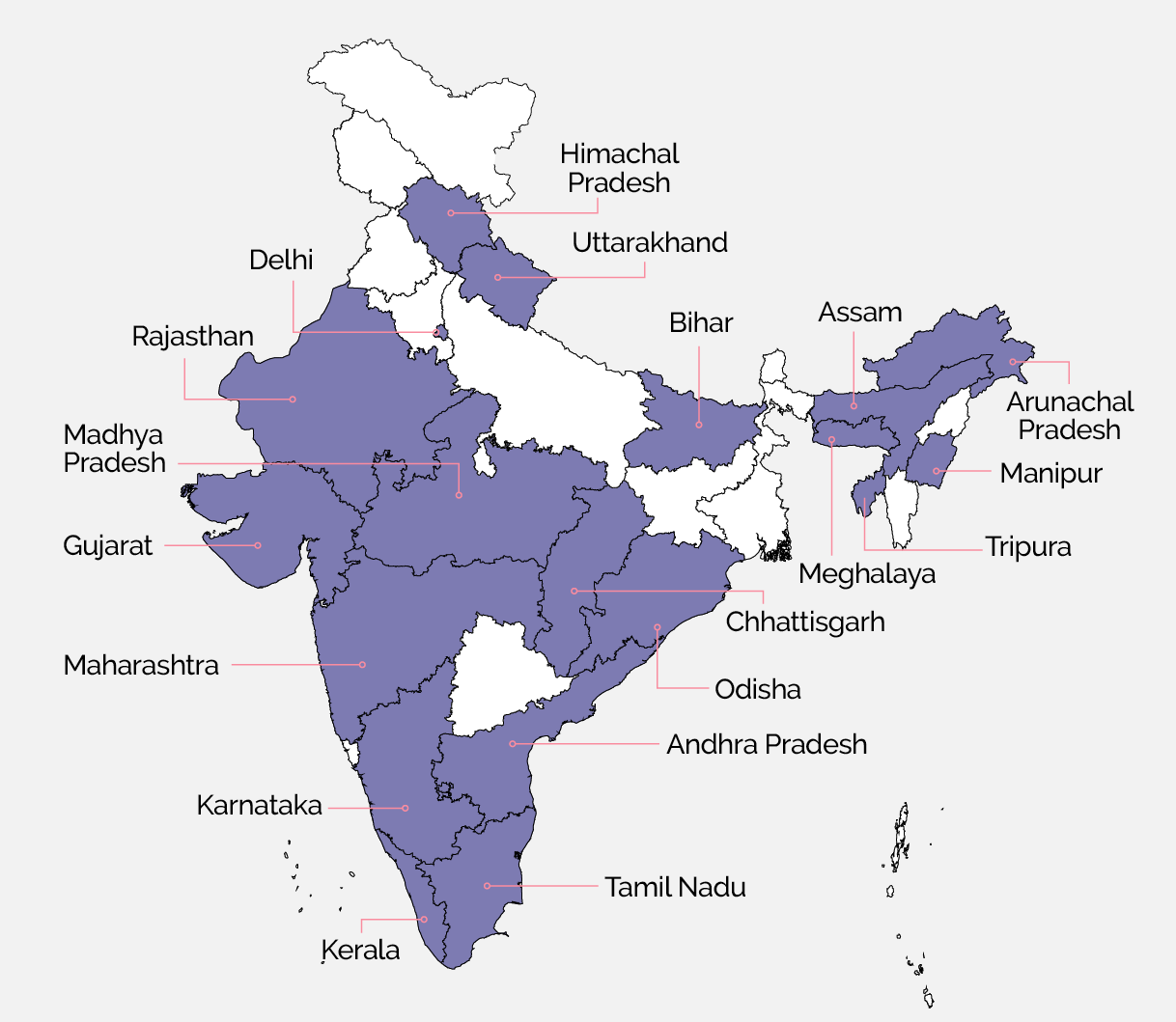

Along the lines of the Government of India, GRB as a budgetary strategy has been adopted by a number of States in the last few years. At present, at least 19 states in India are publishing their own Gender Budget Statements.

Children in India are exposed to various forms of vulnerabilities ranging from low immunisation levels and poor health vitals, to child labour and human trafficking. For instance, eight children were trafficked and exploited in our country every day in 2021. A child budget, also known as Child Responsive Budget (CRB), recognises the vulnerabilities of children and aims to address the same by committing financial resources under relevant interventions. Child budgeting is a PFM strategy which promotes responsiveness of government budgets to the rights and needs of children. It acts as an analytical tool for assessing the priority accorded to children in public spending by the government through various schemes, programmes and institutions.

A Child Budget Statement is not a separate budget but is derived out of the annual budget of the government by recognising and collating the interventions (from different ministries/ departments in the Union and the State Governments’ annual budget) which are either directed exclusively towards children or have substantial benefits for them.

The Ministry of Women and Child Development, in 2007-08, pointed out that “…the total magnitude of budget outlays on child-specific programmes/schemes, is what we refer to as the Child Budget”. Child budgeting is not only about the quantum of funds allocated for children in the annual budget. It includes looking at all stages of the budget cycle - planning and programming, budgeting, utilisation of funds, and monitoring of outcomes, through the lens of children’s needs.

Why is Child Budgeting needed in India?

Children constitute around 40 per cent of India’s total population which makes it one of the youngest nations in the world. Government provisioning for children is important for addressing the challenges they face across sectors such as health, nutrition, education, and protection. It is important to have a comprehensive listing of interventions backed by adequate public provisioning to address needs of children for their overall wellbeing. This is especially crucial for the most disadvantaged sections of children who depend primarily on access to critical public services for their sustained development.

As a signatory to the United National Convention on the Rights of the Child (UNCRC), India has committed to ensuring the rights and wellbeing of its children in accordance with UNCRC’s mandate. The UNCRC’s approach that all children must have an equal opportunity to survive, develop and reach their full potential without discrimination or exclusion has also been adopted in India in the form of the National Policy for Children in 2013 and the National Plan of Action for Children in 2016. The latter has specified that “a comprehensive analysis of budgetary provisions for children should be undertaken which should include total allocation and expenditure by Central and State Governments as well at Panchayats and Urban Local Bodies (ULBs)”.

The main objectives of undertaking budgeting for children are:

Better planning leading to formulation of child sensitive interventions in the form of policy measures

Higher allocations for children in public budgets aimed towards realising national development outcomes

Improved utilisation of allocated provisions

Improved outputs and outcomes for children, which can be monitored through observable and measurable changes in child related indicators.

How has Child Budgeting evolved in India?

Child Budgeting requires a multi-dimensional approach involving a number of stakeholders. While the most prominent and commonly used tool has been the publication of the Child Budget Statement (CBS), it is not the only strategy for ensuring a child responsive Budget. Along with the development of the CBS, some of the other important strategies that have been adopted by the Union and the State Governments of India are:

Orientation and regular capacity building of government departments working on child related schemes and programmes on the need for child budgeting and the steps that can be taken in this regard

Bringing out budget circulars with the details of the process to be followed by the implementing departments for reporting in the CBS

Establishing Child Budget Cells within the government framework as nodal entities for driving the initiative on a yearly basis Conducting regular monitoring and evaluation of the departments in terms of the progress made in strengthening their child responsiveness

How is Child Budgeting carried out in the Union Budget?

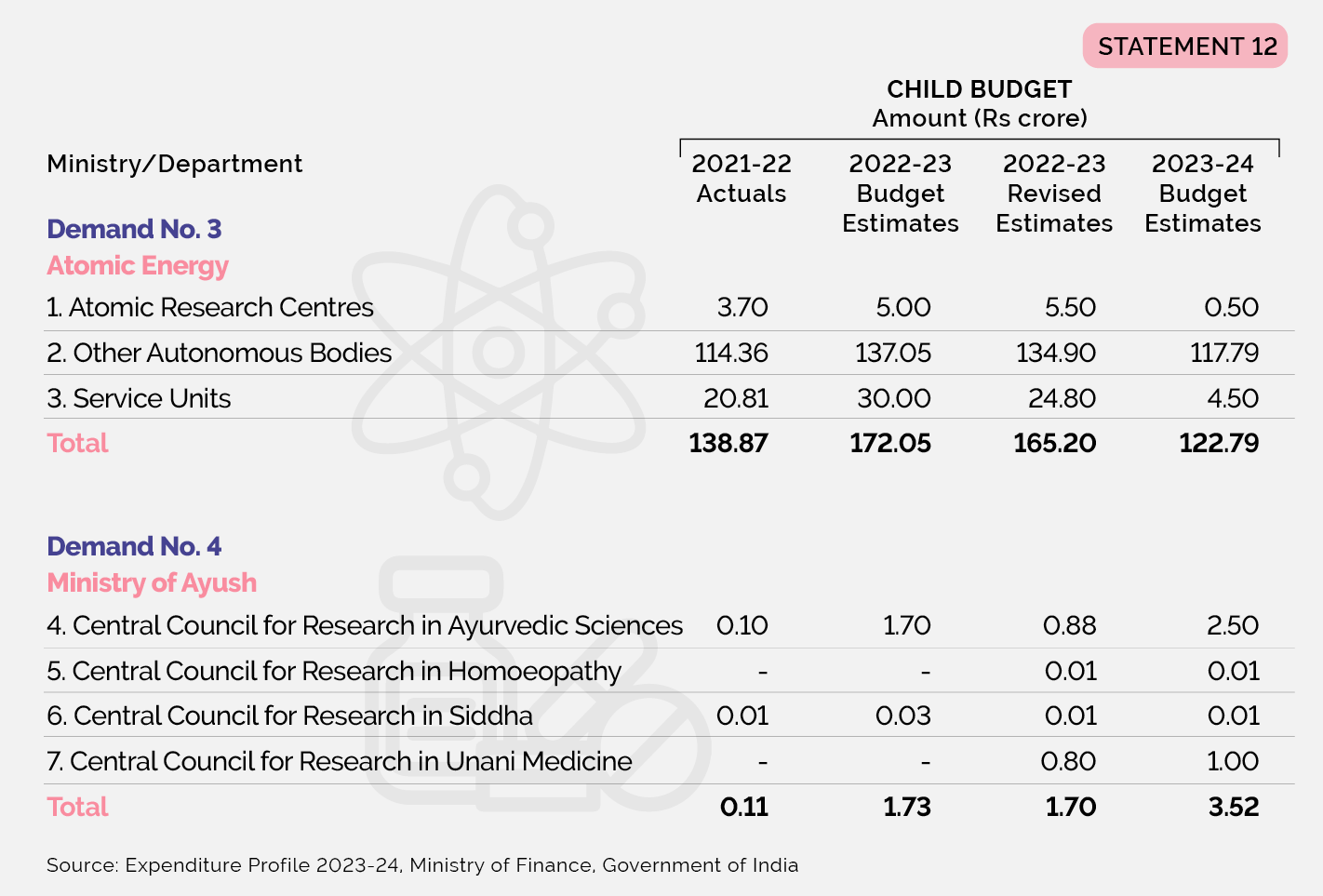

The Union government adopted the strategy of child budgeting in the early 2000s. The Ministry of Women and Child Development (MWCD) had dedicated a chapter to Child Budgeting in its Annual Report for the first time in early 2003. This trend continued over the next few years. In February 2008, the Union Ministry of Finance introduced the first Child Budget Statement (CBS) titled “Budget Provisions for Schemes for the Welfare of Children”. Thereafter, a CBS capturing all child specific schemes and programmes of the Union government has been a regular part of the Union Budget documents every year. It has now been renamed as ‘Allocations for the Welfare of Children’ (Statement 12).

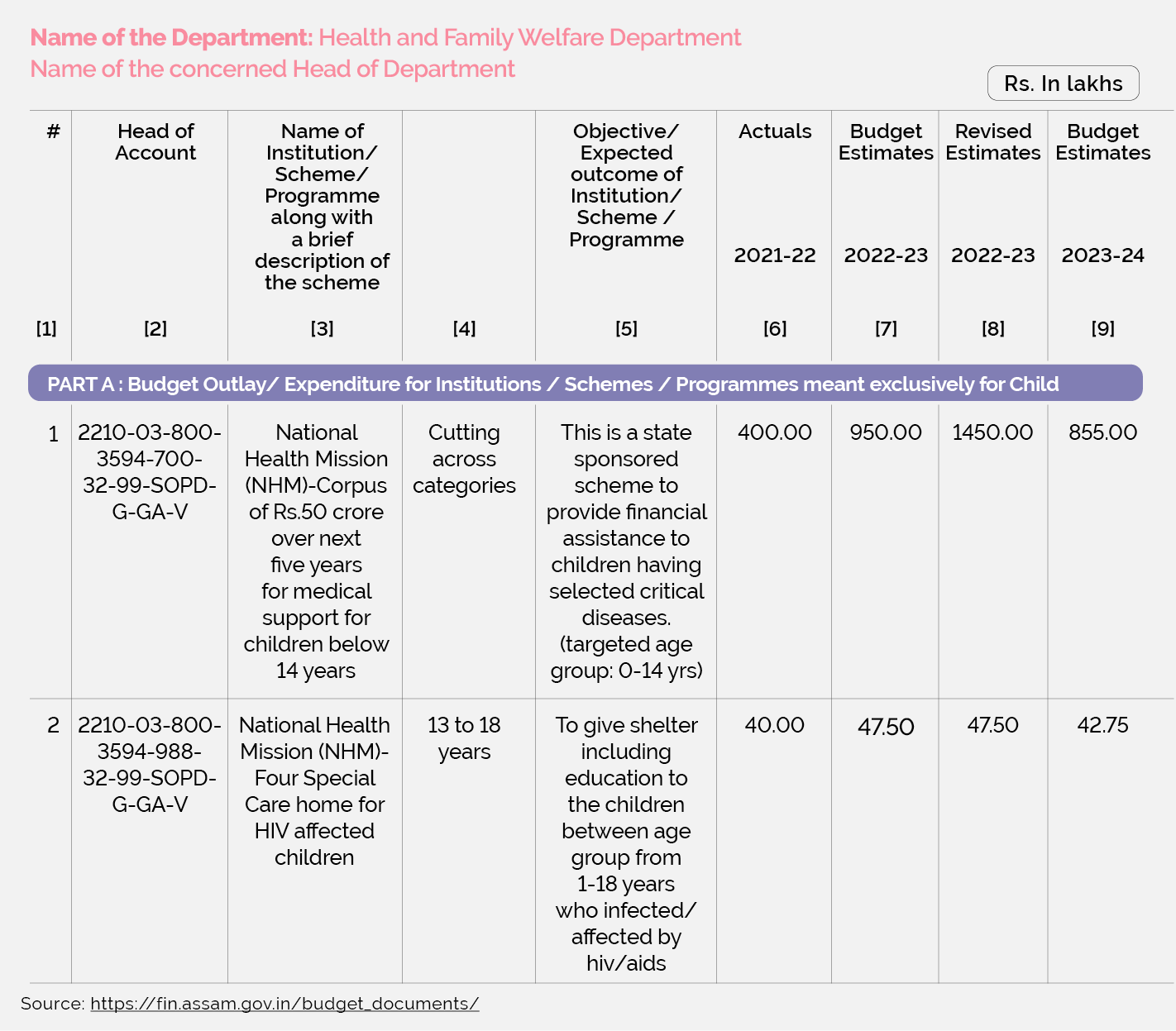

Figure 5: Child Budget Statement in the Union Budget of India for 2023-24

What is a Child Budget Statement?

A CBS is compiled by identifying, categorising and enlisting the budgetary allocations and expenditures which benefit children from the main budget. By looking at the policies and programmes budgeted for children, one can assess the commitment of the government towards them. Thus, the CBS serves as an important policy tool for assessing the priority given to children by the government as well as for identifying gaps in the resource needs for children. CBSs are published by the Union government as well as by a number of State governments.

The Union Budget publishes such a statement every year (Statement 12) as part of the Expenditure Profile section of the budget. For States, CBSs can be accessed alongside the respective State budget documents on the State finance department websites or budget portals.

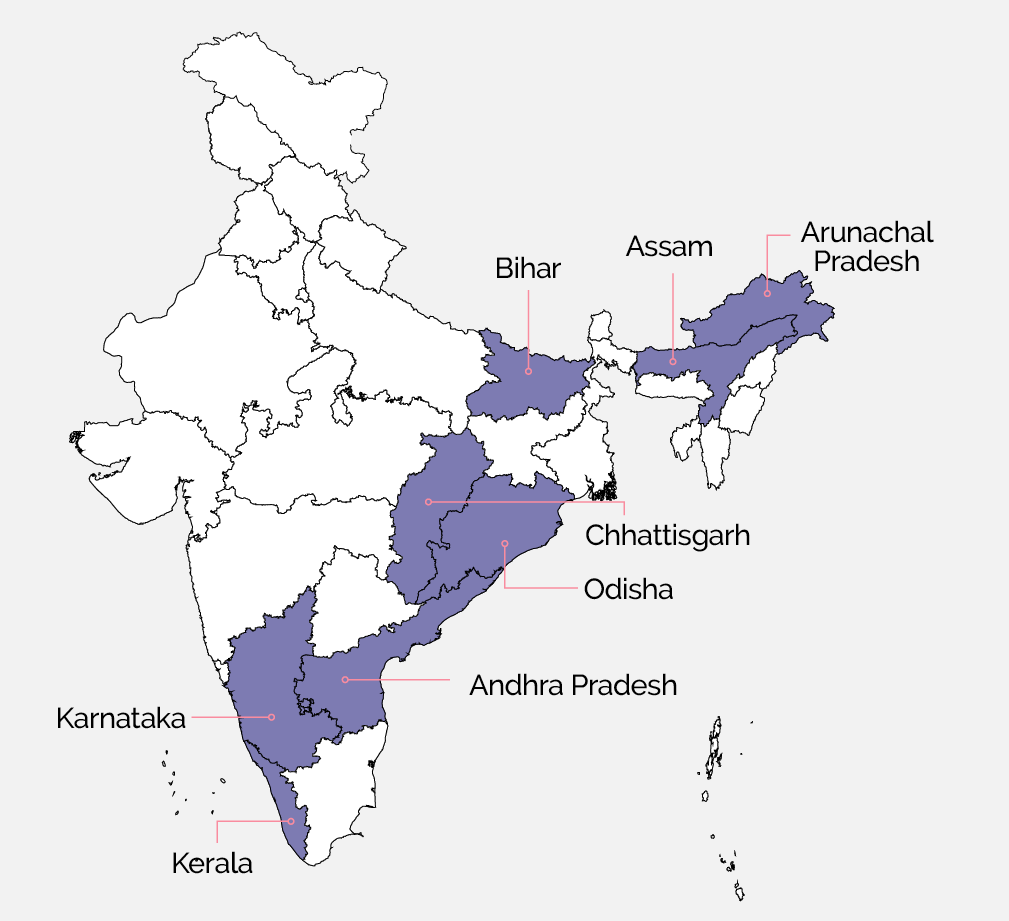

Which States of India have adopted Child Budgeting?

Several State governments have been engaging in budgeting for children. One of the most common tools used for this has been the publication of a separate CBS along with the annual State budgets, initiated by the State government of Bihar in 2013-14. Several other State governments have undertaken a similar exercise in recent years.

Map 2: States publishing Child Budget Statements

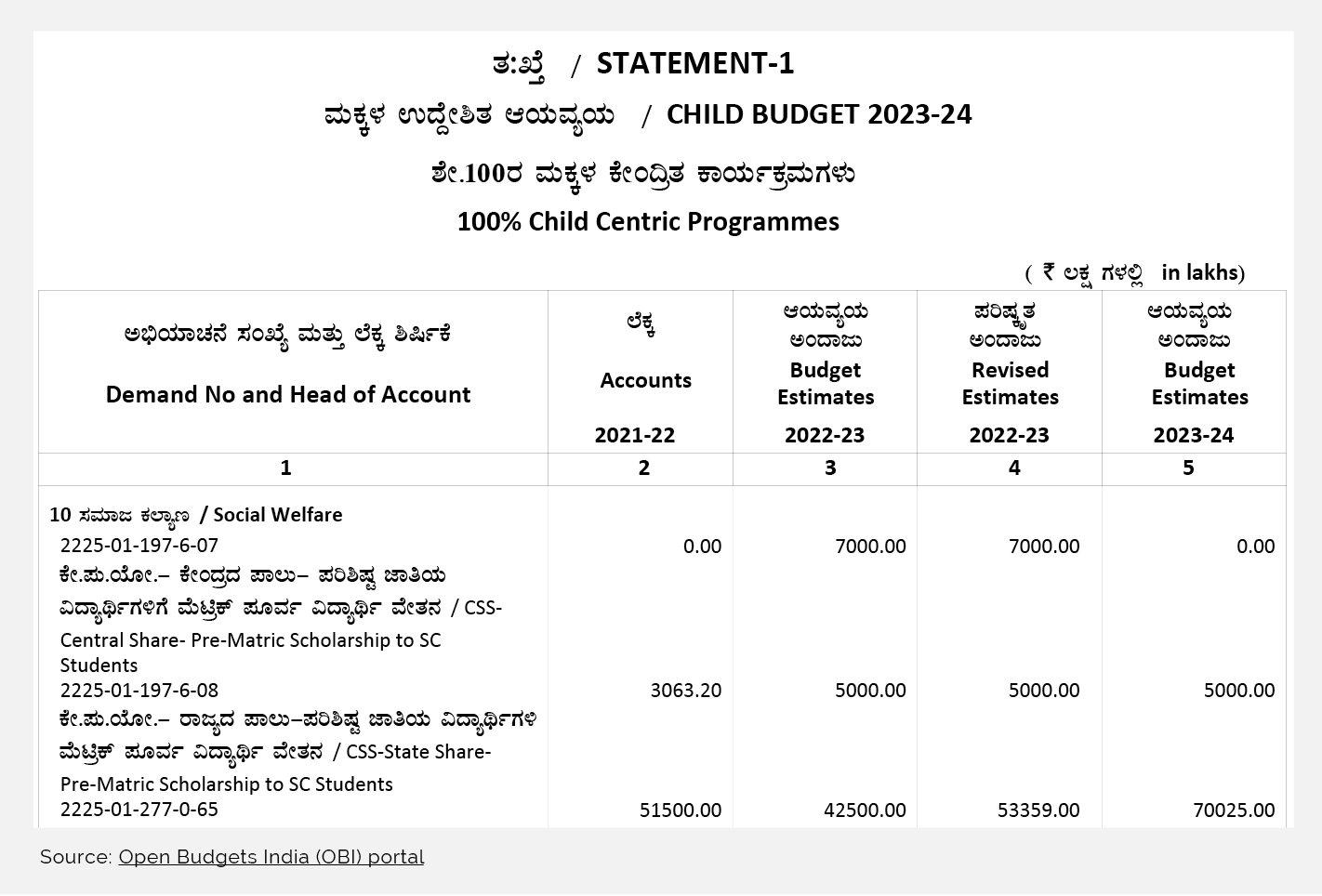

Figure 6: Karnataka Child Budget Statement for 2023-24

Figure 7: Assam Child Budget Statement for 2023-24

The format of CBSs differs from State to State. For instance, States such as Assam and Karnataka segregate the schemes and programmes into sections called Part A and Part B. Part A denotes schemes and programmes which are exclusively meant for children (e.g., Integrated Child Protection Scheme and Mid-Day Meal). Part B consists of child inclusive composite schemes which are not specifically targeted for children, but have an overall bearing on the development of children. Example of a Part B scheme is the Post Matric Scholarship scheme.

4.

Budgeting for Scheduled Castes and Scheduled Tribes

Why is Budgeting for Scheduled Castes and Scheduled Tribes needed?

Scheduled Castes (SCs) in India continue to be one of the most deprived sections of the society. Persistent discrimination is one of the major factors resulting in critical gaps in their socio-economic development. Despite affirmative action by the governments for their overall development for several decades, there are visible deficits in almost all spheres.

As per the National Family Health Survey 2019-21 (NFHS-5), more than half of SC households (51 per cent) fall in the two lowest wealth quintiles in India. Further, almost 36 per cent of SCs have had no schooling and the under-five mortality rates remain high. The NFHS-5 further found the nutritional status of SCs to be poor with 43 per cent of SC children being stunted, 39 per cent of them being underweight, and almost 56 per cent of SC women being anaemic.

Similarly, the Scheduled Tribes (STs) in India also face serious vulnerabilities and shortfalls in their overall development. The NITI Aayog’s Three Year Action Agenda noted that STs are nearly twenty years behind the average Indian population. NITI Aayog further noted that STs have low enrolment ratios in secondary education and high unemployment rates. Further, there exist inconsistencies in the implementation of legislations pertaining to them.

Given the socio-economic and geographical vulnerabilities of SCs and STs, government interventions providing a range of public services through targeted planning, and budgeting and implementation of schemes for these communities becomes especially important. The budgeting strategies for SCs and STs were referred to as the Scheduled Caste Sub Plan (SCSP) and Tribal Sub Plan (TSP) respectively, and have been in practice at the level of the Union as well as the State governments. Since 2017-18, these have been renamed as the Development Action Plan for Scheduled Castes (DAPSC) and the Development Action Plan for Scheduled Tribes (DAPST), respectively.

What is the Scheduled Caste Sub Plan (SCSP)?

The Constitution of India has provided for instituting a series of protective and development measures and ensuring affirmative action to cater to the overall development of SCs. Consequently, the Government of India has followed a two-pronged strategy for their upliftment – introducing a dedicated fiscal strategy for ensuring targeted policy-driven benefits across sectors, and instituting a nodal ministry for their welfare. In 1979, the government introduced the Scheduled Caste Sub Plan (SCSP), a strategy envisaged towards earmarking funds for development of SCs across sectors, at least in proportion to their share in the overall population of the country (16.6 percent as per Census 2011). SCSP was instituted as a budgetary strategy during the Sixth Five Year Plan period.

According to the guidelines of the Scheduled Caste Sub Plan, 2006, , “The Special Component Plan has been formulated as a mechanism for channelising a due share of benefits in physical and financial terms from the various programmes of every sector in favour of SCs.” This earmarking was supposed to be done from the Plan Expenditure of the Consolidated Fund of India. However, after the merger of plan and non-plan heads of expenditure in the Union Budget from 2017-18 onwards, the Union government has asked the ministries/departments to allocate funds for the SCSP now known as DAPSC from the total scheme allocations. A nodal department for welfare of SCs by the name of the Department of Social Justice and Empowerment (DSJE) has also been constituted.

The SCSP guidelines of 2006 further specified that the schemes which are to be considered a part of the SCSP must have quantifiable benefits to the SC households, enhance the income of the target community and lead to the development of assets in sectors such as agriculture, animal husbandry, dairy development, and fisheries. Further, interventions providing basic minimum services such as primary education, health, drinking water, nutrition, rural housing, link roads, and electrification to SC villages will have to be prioritised by the States while engaging in budgeting for the SCs.

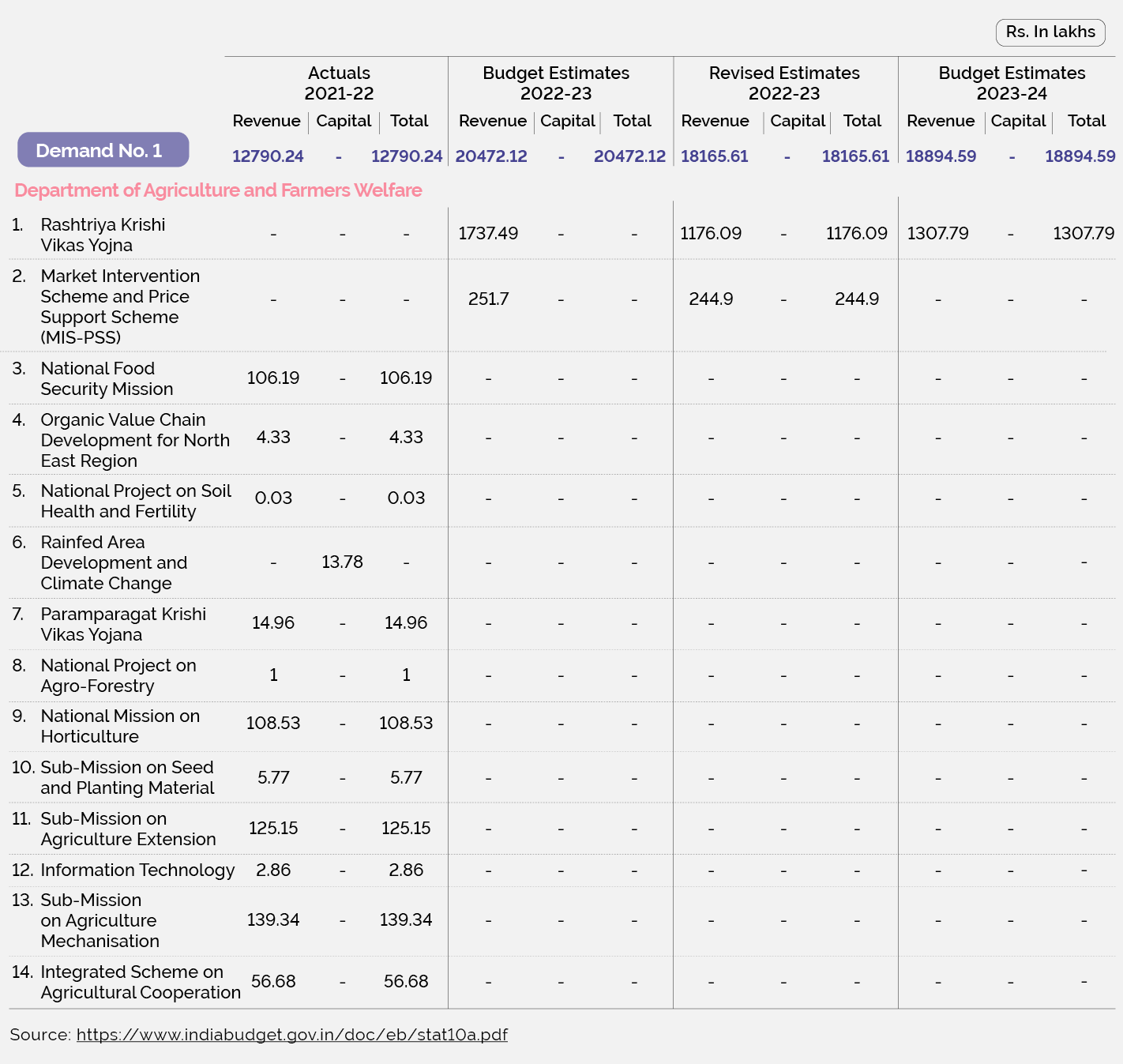

The Union government brings out a separate statement with department-wise details of funds which have been earmarked for the Scheduled Castes in a particular year. This Statement 10A of the Expenditure Profile is titled ’Allocation for Welfare of Scheduled Castes’.

Figure 8: Statement on Allocation for Welfare of Scheduled Castes in the Union Budget

This statement provides the details of budgetary allocations which have been earmarked for Scheduled Castes by different ministries and departments.

A number of States (e.g., Andhra Pradesh) also publish separate statements with details of funds earmarked for SCs, while other States include such budget heads under their Detailed Demands for Grants for the relevant department (e.g., Gujarat and Maharashtra).

What is the Tribal Sub Plan (TSP)?

Taking cognisance of the multiple deficits faced by the ST community, the Government of India introduced the strategy of Tribal Sub Plan (TSP) in 1974-75. The TSP envisaged earmarking funds from the plan budget of the government for the welfare of STs across ministries, at least in proportion to their share in the total population (which is 8.6 percent as per the Census 2011). After the merger of Plan and Non-Plan expenditures, the TSP was renamed as Scheduled Tribe Component (STC) by the Ministry of Finance. 42 Union Ministries/Departments have been identified for earmarking funds for the STC as of 2023-24. Besides, State governments are supposed to earmark TSP funds in proportion to the ST population as per the Census 2011 in the State with respect to total State Plan. The monitoring of TSP was being done by erstwhile Planning Commission until 2017-18. The STC is being monitored by the Ministry of Tribal Affairs since 2018-19.

In its revised guidelines for implementing the SCSP and TSP published in 2014, the Planning Commission mentioned, “The objective of the Tribal Sub-Plan (TSP) is to bridge the gap between Scheduled Tribe (ST) population and others by accelerating the development of STs by securing to them:

Human resource development by enhancing their access to education and health services;

Enhanced quality of life by providing basic amenities in tribal areas/localities including housing;

Substantial reduction in poverty and unemployment, creation of productive assets and income generating opportunities;

Enhanced capacity to avail opportunities, gain rights and entitlements and improved facilities at par with other areas, and

Protection against exploitation and oppression.”

The Ministry of Tribal Affairs (MoTA) was set up in 1999 as a nodal ministry for the welfare of STs and to design and implement schemes exclusively for them.

Despite being the nodal ministry for STs, the scope of the MoTA has remained limited to interventions related to education, art and culture, and livelihoods of the ST community. All other kinds of development deficits are to be addressed using the TSP funds across sectors. The schemes and programmes which form a part of the TSP must have a clearly defined and quantifiable benefit for the community. These should also cover a number of sectors like education, income generation, improving access to irrigated land, entrepreneurship, employment and skill development projects, and access to basic amenities, in addition to having in-built mechanisms/monitoring systems to ensure optimum utilisation of funds meant for the intended purpose.

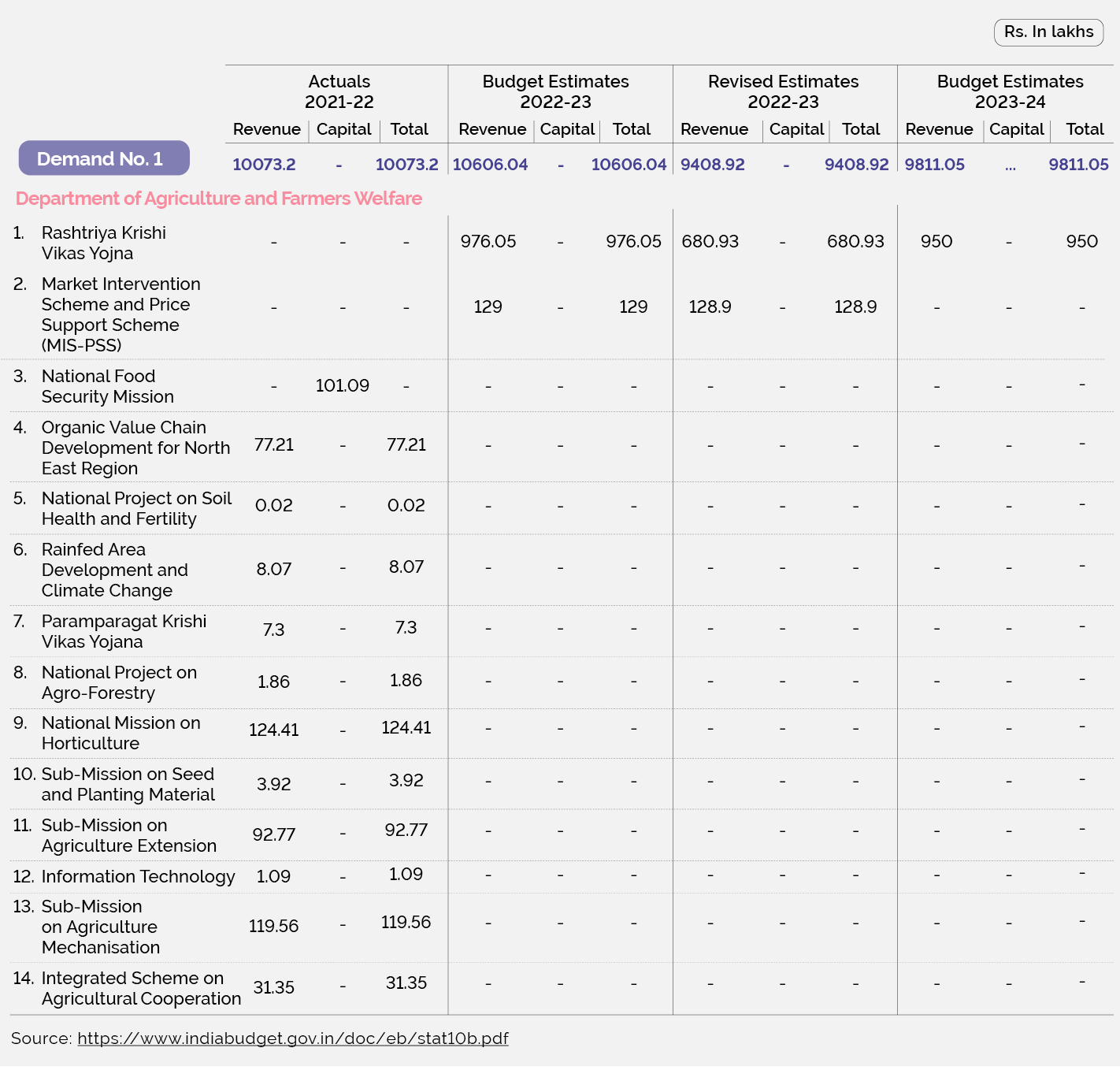

Similar to the special statement for the SCs, the Government of India publishes a separate statement with budgetary details for the STs as well. This Statement 10B in Expenditure Profile is titled ‘Allocation for Welfare of Scheduled Tribes’.

Figure 9: Statement on Allocation for Welfare of Scheduled Tribes in the Union Budget

This statement provides the details of budgetary allocations which have been earmarked for Scheduled Tribes by different ministries and departments.

Outcome Budgeting is a PFM tool with the purpose of mapping resources/outlays to outputs and outcomes. It is similar to a report card for assessing the progress made in government schemes and programmatic interventions, in terms of the financial as well as the physical targets set. This practice of mapping outlays to outcomes was initiated by the Government of India in 2005-06 as an annual exercise. Outcome Budgets involve not only the short-term outputs that are needed to be delivered by a particular government intervention but also the longer-term outcomes that are expected to be achieved out of it.

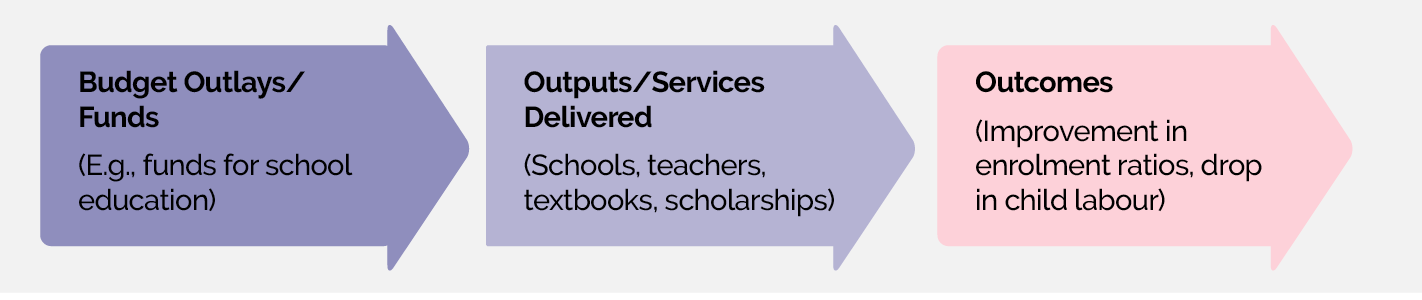

The following example illustrates how outlays in the form of funds for school education can be translated into outcomes.

Figure 10: Stages of Outcome Budgeting

Budgets earmarked for school education (considered as outlays/funds in this chain) have a defined objective of delivering services such as running schools, paying for teachers’ salaries, providing textbooks and scholarships to students etc. These services when delivered effectively in the short term can lead to desired outcomes like improvement in enrolment ratios of students and a visible drop in child labour statistics in the longer time-frame.

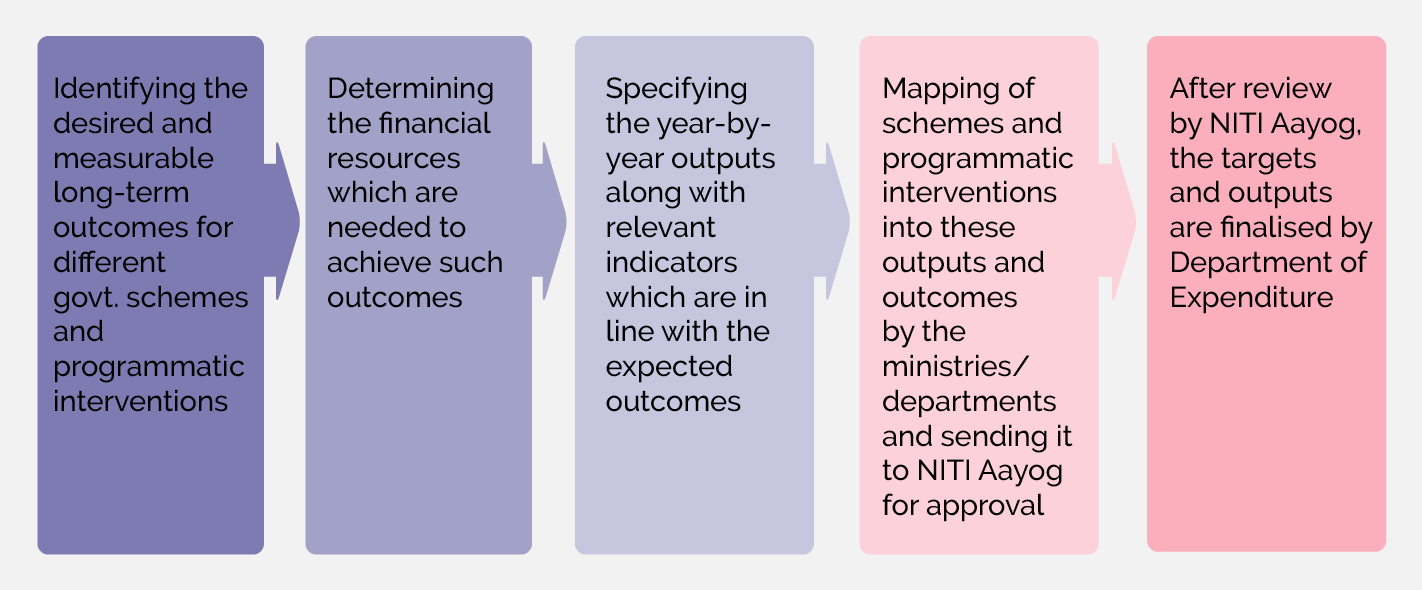

Outcome Budgeting involves the following steps for the government:

Step I: Defining the desired long-term outcomes as well as the intermediate outputs for the concerned government ministries or departments;

Step II: Identifying the interventions (schemes, programmes, etc.) which are required to achieve the targeted outputs and outcomes;

Step III: Determining the expenditure required for implementing the identified interventions which then forms a line item in the budget for that particular year.

How does Outcome Budgeting improve budgetary practices?

One of the central discourses around public policies is the question of how well the budget outlays translate into outputs in terms of services to the people, and how that output leads to improvement in development outcomes for the people and the country.

A typical budget is a simple financial document which only shares information about the money allocated and spent under various heads. This does not give any detail in terms of outputs delivered or outcomes achieved. It is crucial that spending of these limited public resources enable the fulfilment of clearly defined goals, ensuring transparency and accountability of the government. Outcome oriented budgeting is an important step in that direction and calls for greater scrutiny of the budgets earmarked for particular goals.

How is Outcome Budgeting carried out?

The most commonly used tool used by governments for Outcome Budgeting has been the annual publication of Outcome Budget Statements (OBS) in addition to the other budget documents. The Union government began the practice of bringing out an OBS in 2005. Several States have also started publishing these statements along with their annual budgets.

Following is a step-by-step process for preparing an OBS.

Figure 11: Steps for preparing an Outcome Budget Statement

The format for preparing the OBS is outlined in the Budget Circular each year, well ahead of the actual presentation of the budget. It must be mentioned that bringing out an OBS is not the only step towards ensuring an outcome orientation to budgets. It has to be complemented by other initiatives like orientation of the implementing departments as well as the Finance Departments on the importance of undertaking this exercise, regular capacity building of the government officials in charge of implementing various schemes, proper implementation of the latter in line with the targets and outcomes set, and monitoring of the same.

What is the Outcome Budget Statement of the Government of India?

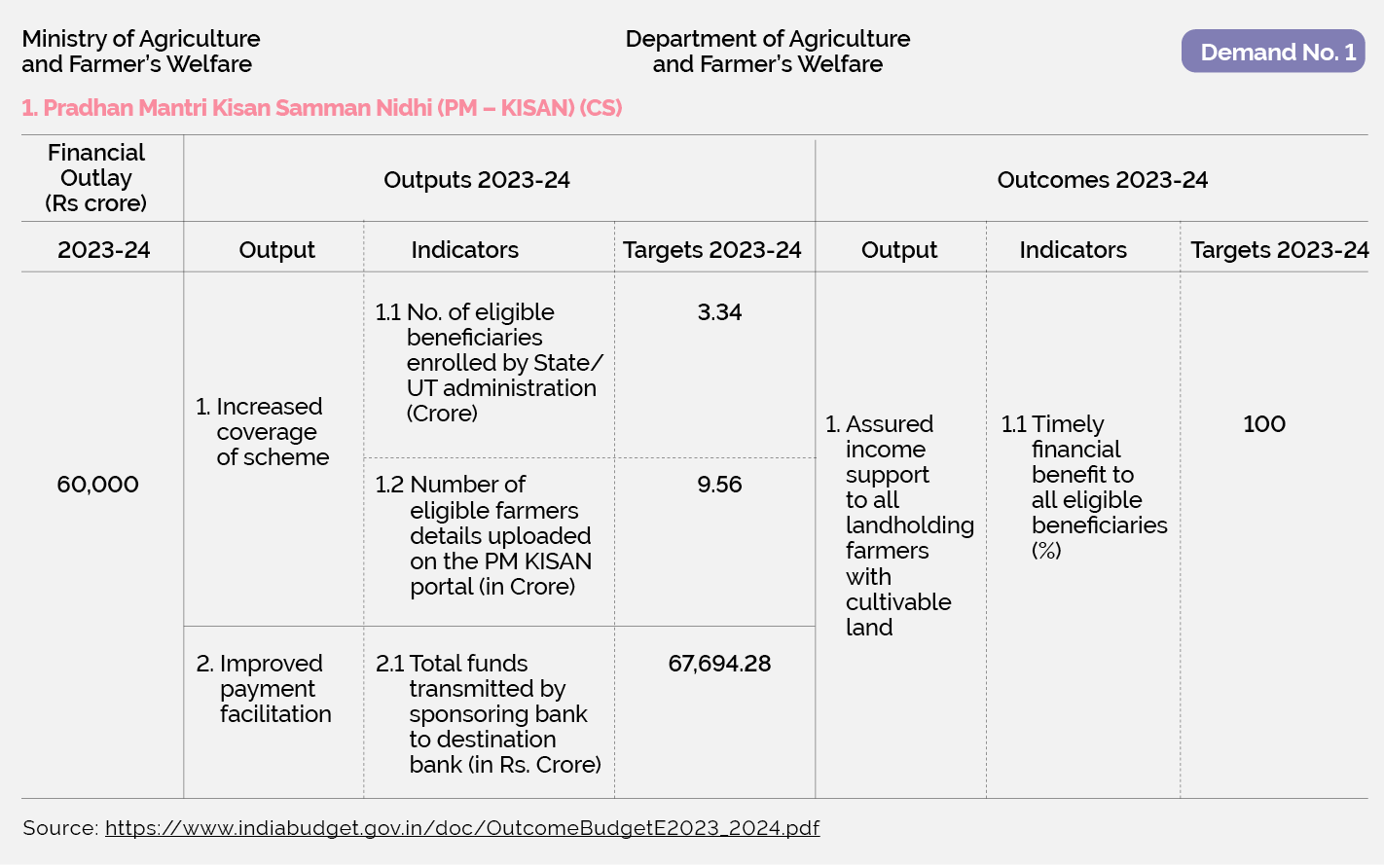

The Union government brings out an annual statement by the name of the Output-Outcome Framework for Schemes along with the other budget publications. This document provides scheme-wise details of both the financial outlays and the physical targets (in terms of outputs and outcomes) for different departments. At present, out of 101 central departments, only 50 contribute to the Union government's OBS. In the snapshot below, the mapping from financial outlays to outputs and then to outcomes can be seen for the income support scheme for farmers Pradhan Mantri Kisan Samman Nidhi (PM – KISAN) (CS).

Figure 12: Outcome Budget Statement in Union Budget 2023-24

The Union OBS includes the details of outputs that have been planned, the relevant indicators through which the progress can be monitored, the targets set, as well as the long-term outcome that is to be achieved through the concerned output.

Which States of India publish Outcome Budget Statements?

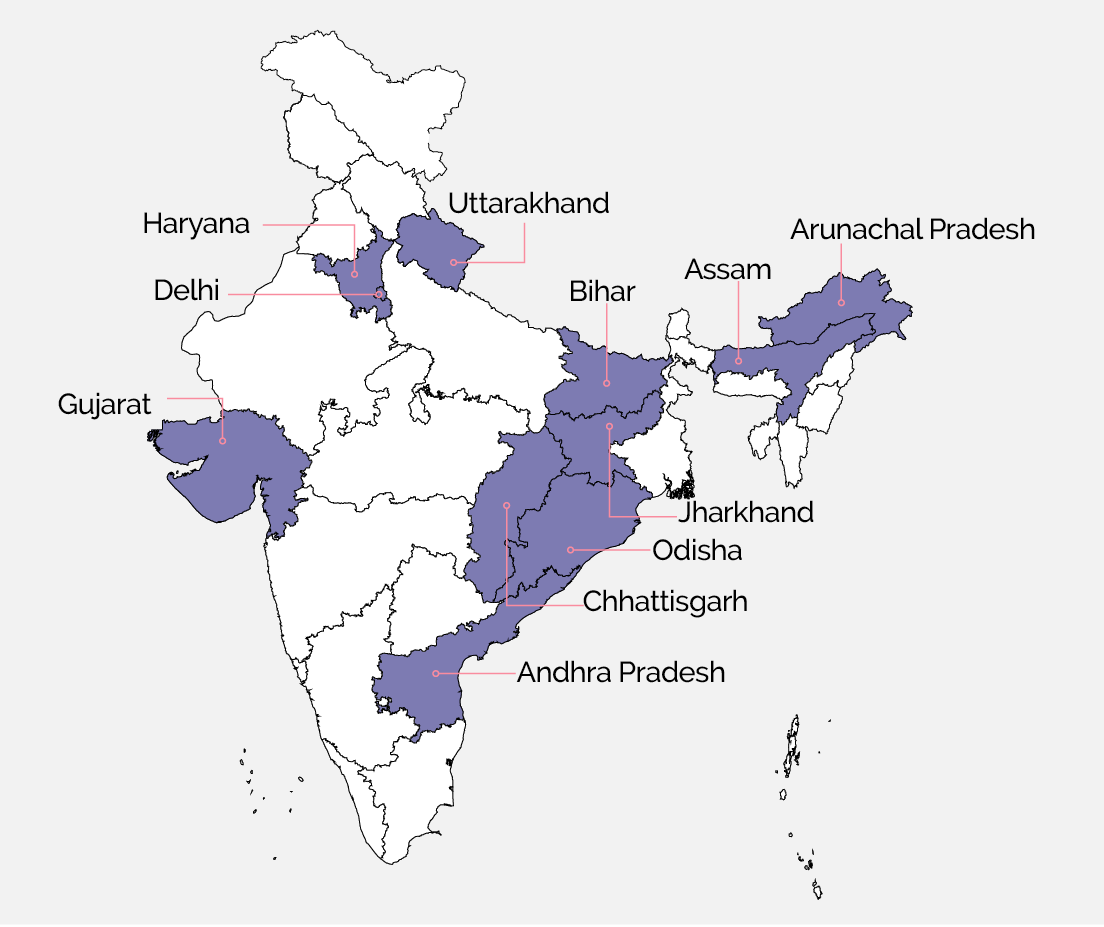

In addition to the Union government, several states also bring out Outcome Budget Statements along with their respective state budgets. Currently, as many as 11 states have adopted this annual exercise.

Map 3: States publishing Outcome Budget Statements

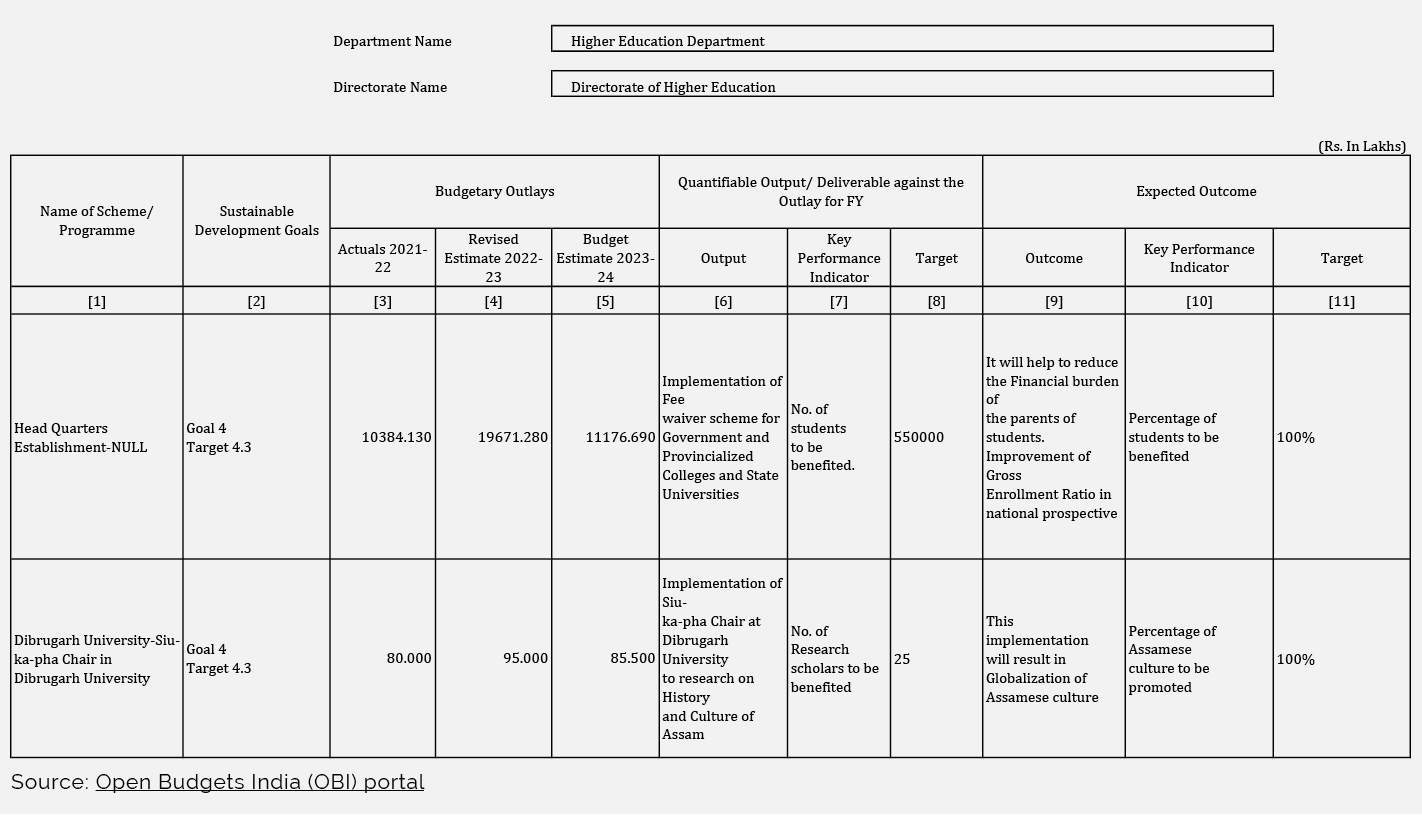

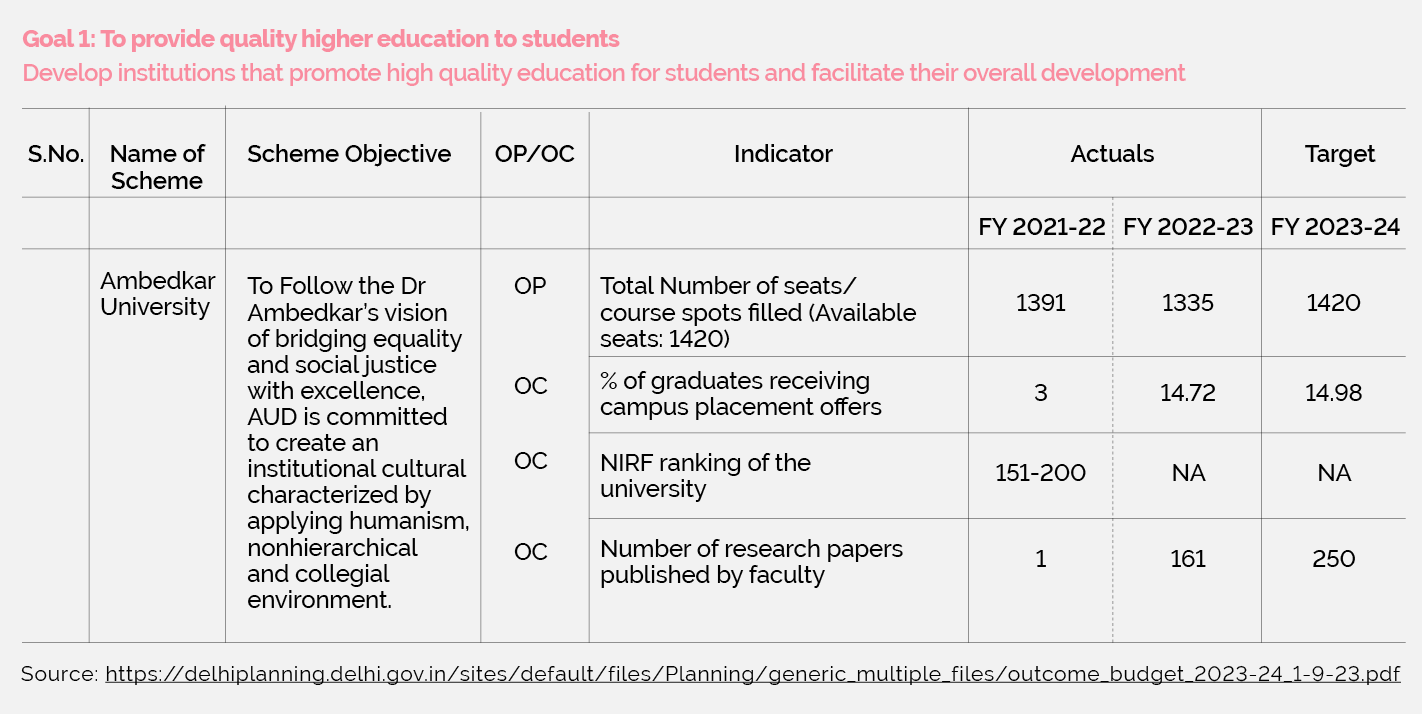

The name as well as the format of the outcome budget related statements have varied across States, as the following examples from Assam and Delhi illustrate. For example, in 2021-22, Odisha brought out an outcome budget by the name of Sustainable Development Goals Budget. A few States such as Odisha, Assam, and Haryana have adopted the framework of the Sustainable Development Goals (SDGs) in their respective statements. Similar to the Union OBS, not all departments in the States contribute to their OBSs. Delhi also brings out mid-term assessment reports on the progress of the outcomes.

Figure 13: Outcome Budget Statement 2023-24 for Assam

Figure 14: Outcome Budget Statement 2023-24 for Delhi

A number of States in India have focused their attention on addressing the issues in particular social and economic sectors such as nutrition, agriculture, and climate change through planning, budgeting, and proper implementation of the sector specific schemes and programmes. The broad objective of engaging with focused budgeting for particular sectors is to address the PFM related challenges existing therein, and to achieve long-term goals or visions defined by the responsible government and/or international standards like the Sustainable Development Goals (SDGs).

One of the most commonly used tools to engage with budgeting for a particular sector is the publication of special analytical statements or documents, which highlights the commitment of the government (for example, sectoral budget speech documents) towards achieving the goals for that sector. These analytical statements identify and collate relevant budget heads pertaining to the specific sector under consideration, which helps to analyse how well the sector has been performing in the State. The last few years have witnessed several such efforts on the part of the States in sectors like nutrition, agriculture, and climate change. The following sub-sections bring together key observations on these statements.

Nutrition Budgeting

What is the need for budgeting for nutrition?

The Global Nutrition Report 2015 indicates that almost 40 percent of the world’s stunted (short-for-age) children under the age of five and nearly 50 per cent of the wasted (low weight-for-height) children live in India. Given that India is one of the world’s fastest growing economies, this raises serious questions regarding the disconnect between economic achievement and the equitable access to publicly provisioned nutrition services. The Union and the State governments in India have accorded high priority to combating under-nutrition; yet, the levels of under-nutrition remain persistently high with significant regional disparities. This makes it extremely important that adequate budgetary resources are allocated to schemes and programmes that deliver nutrition. Nutrition budgets are spread across multiple ministries and departments, and are often integrated within other sectors or programmes, making it difficult to track and disaggregate the same.

How is Nutrition Budgeting carried out in India?

The Nutrition Budget Statement is a strategy employed to make public expenditure more responsive to issues related to nutrition. This is a special budget statement published along with the annual state budget documents, which provides details of all funds allocated to expenditures related to nutrition. A Nutrition Budget, like other special budgets, is not a separate budget but a disaggregated expenditure on nutrition from the overall budget for the State. It is prepared by identifying and collating nutrition related budget heads and collating them in a systematic manner.

Which States of India publish a Nutrition Budget Statement?

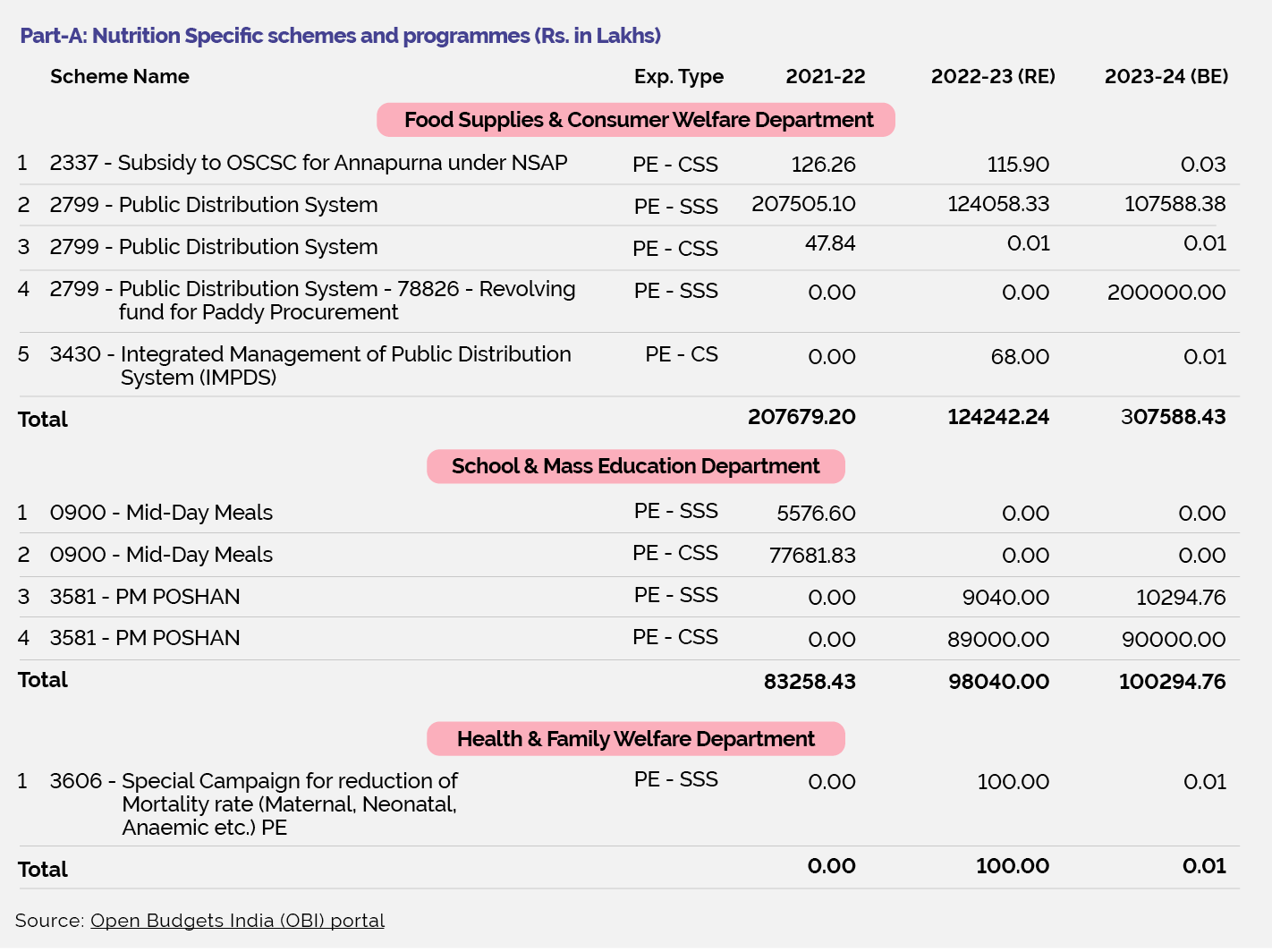

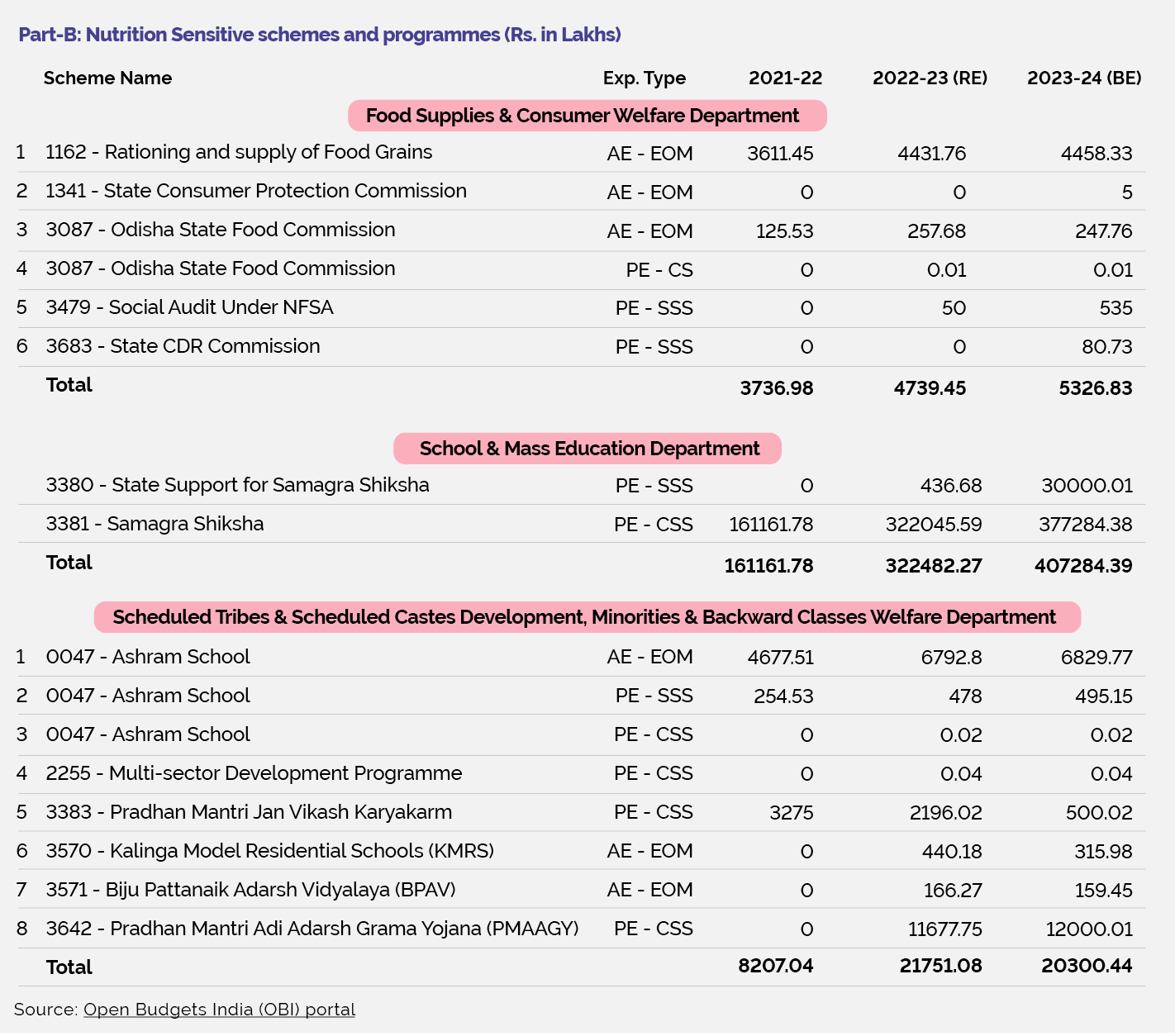

At present, Odisha is the only State which has started publishing a Nutrition Budget Statement alongside its state budget.

Figure 15: Odisha Nutrition Budget 2023-24 (Part A)

Figure 16: Odisha Nutrition Budget 2021-22 (Part B)

The Nutrition Budget Statement records both nutrition specific schemes (in Part A of the Statement), and nutrition sensitive schemes which may not be specifically directed towards providing nutritional services to targeted groups but certainly have a bearing on the nutritional outcomes of the State’s population (in Part B of the Statement). Important examples of nutrition specific interventions are Mid-Day Meal (MDM), Integrated Child Development Services (ICDS), and the Mamata scheme which is a State-sponsored conditional cash transfer scheme for pregnant women. Nutrition sensitive schemes, on the other hand, have a longer list and include the National Rural Health Mission, rationing and supply of food grains, and the Samagra Shiksha Abhiyan, among others. Both these categories cover schemes across a number of departments.

Agriculture Budgeting

What is an Agriculture Budget?

An Agriculture Budget is prepared by identifying and collating agriculture related budget heads and presenting them in a systematic manner.

What is an Agriculture Budget Statement?

An Agriculture Budget Statement is a special budget statement published along with the annual State budget documents, which provides the details of what a particular State is doing or intends to do with respect to the agriculture and allied sectors.

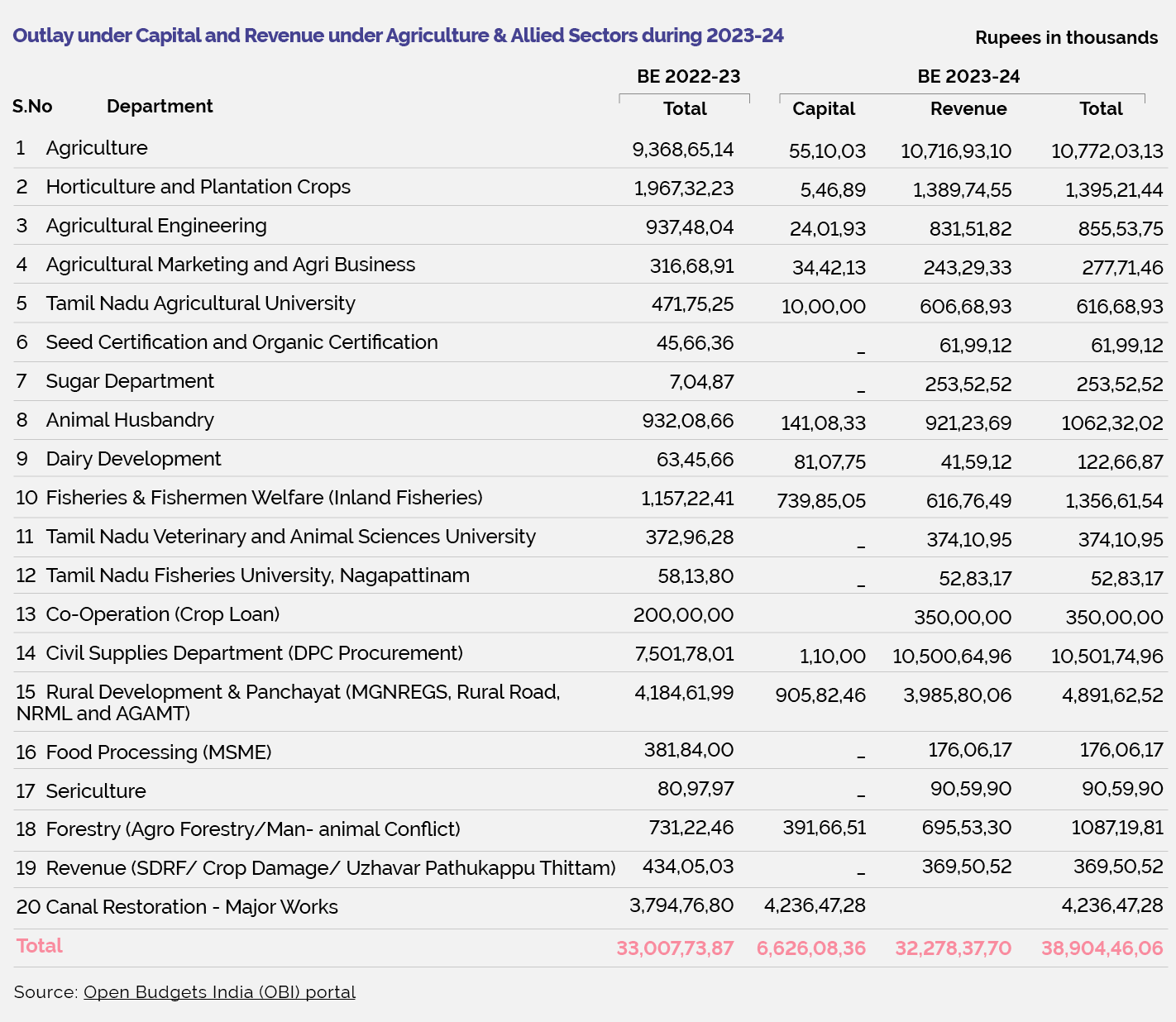

Which States of India publish an Agriculture Budget Statement in India?

At present, the Agriculture Budget Statements are being published by a few States as a part of their annual budget publications, but not by the Union government. Some of the States publishing this Statement are Odisha, Chhattisgarh, Madhya Pradesh, and Tamil Nadu. While the formats of these statements differ across States, the overall objective is to focus on the agriculture and allied sectors through higher budgetary resources and address the PFM related issues within the sector.

Figure 17: Agriculture BudgetStatement 2023-24 for Tamil Nadu

Figure 18: Agriculture Budget (Krishi Budget) 2023-24 for Chhattisgarh

Climate Budgeting

How is Climate Budgeting carried out in India?

The most common tool for climate budgeting is the publication of a Climate Budget Statement or Green Budget Statement. This is a special budget statement published along with the annual State budget documents which provides the details of what a particular State is doing or intends to do to address the challenges pertaining to climate change.

This is not a separate budget but a part of the overall budget for the State and is prepared by identifying and collating relevant budget heads directed towards improving climate resilience and mitigation outcomes, and presenting them in a systematic manner. Odisha is the first State which has initiated the practice of publishing a separate Climate Budget statement since 2020-21. Consequently, Bihar and Delhi have also started presenting Green Budget Statements.

The overall objectives of presenting this analytical budget statement are:

Identifying the climate mitigation or adaptation benefits of public expenditure earmarked for the sector and planning of future investments in this domain

Facilitating the re-alignment of the objectives of various schemes run by different departments to make these more sensitive to the needs of the state for achieving greater climate resilience in future;

Predicting future loss and damage arising out of climate change by taking different climate scenarios (regional projections) with the current state of adaptation and mitigation efforts of the State, and

Standardising domestic and international climate action as well as reporting of expenditure in this sector with the adoption of the framework of SDGs

Climate/Green Budget Statements provide a glimpse into several facets of climate change action by the States and related statistics on it. They also present budget allocations made in relevant schemes and programmes in this sector, for the current year as well as the previous year.

Which States of India produce Climate Budget Statements?

Climate Budget Statements are being published by a few states such as Odisha and Bihar as part of their annual budget publications, as shown below. However, the structure and content varies from State to State. This practice has not been adopted by the Union government as of 2023-24.

There have been a number of budgetary strategies adopted both at the levels of the Union and the State governments of India for addressing the needs and concerns of specific sections of population and sectors of the economy. Further, these strategies, as PFM tools, have been successful in assessing the state of resource allocation targeted towards particular sectors or sections of the population, besides evaluating the policy priorities of governments. Apart from this, these strategies have also been useful tools for monitoring and evaluating policy implementation. However, there is a long way to go in actualising the desired outcomes of adopting these strategies. Governments should look beyond preparing financial statements alone, and make concerted efforts towards implementing the visions associated with these numbers.