India is a vast country, not only in terms of geography, but also in terms of populace. This vastness requires a similaraly expansive political governance structure that can cater to the different needs of the populace.

The existing political governance system has accordingly been designed where the three tiers of the government have been assigned different roles and responsibilities. The three tiers are – Union Government, State Governments, and Local Governments / Bodies. Local Bodies are further divided into two categories – Urban Local Bodies (ULBs), and Rural Local Bodies (RLBs).

This section focuses on Rural Local Bodies which are also known as Panchayati Raj Institutions (PRIs).

As the name suggests – RLBs are institutions for the governance of rural areas.

Types of Rural Local Bodies

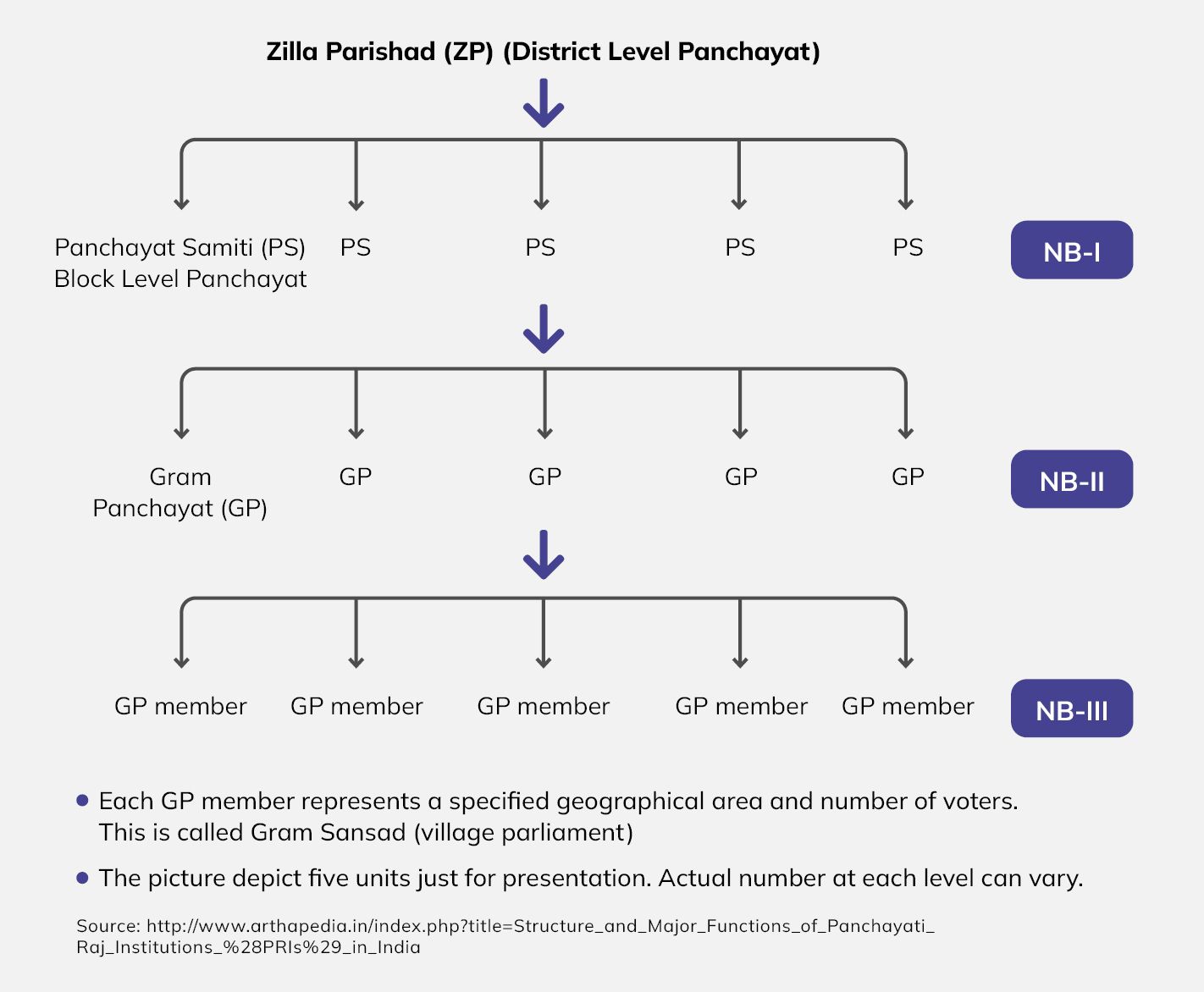

Depending on the area they govern, RLBs can be divided into three different types.

Gram panchayats – these RLBs operate at village level. Generally, the head of gram panchayat is called ‘Sarpanch’.

Mandal or Taluka Panchayats or Panchayat Samiti – these RLBs operate at Block level, and are generally headed by a chairperson or deputy chairperson. These panchayats act as a link between grampanchayats and zila panchayats.

Zilla panchayats or Zila parishad – these RLBs operate at District level. Its office is located at the district headquarters. The chairpersons of all mandal panchayats are members of Zila parishad. These members elect a chairperson to head the Zila Panchayat. The ‘District Collector’, or ‘District Magistrate’ or the ‘Deputy Commisionor’ acts as the convening secretry of Zila Panchayat.

While in case of Zila panchayat and Mandal panchayat, their areas coincide with the administrative boundries of district and blocks respestively, the area of a gram panchayat does not have to coincide with a particular village. It is created on the basis of population, and may include more than one village.

The states or Union Territories which have less than 20 lakh inhabitants, there would be only two levels of PRIs namely Gram Panchayats and Zilla Panchayats.

Some of these terms, like zila, mandal or gram might differ across states mainly because of the language differences.

Figure 1: How the Three layers of Panchayats are Connected

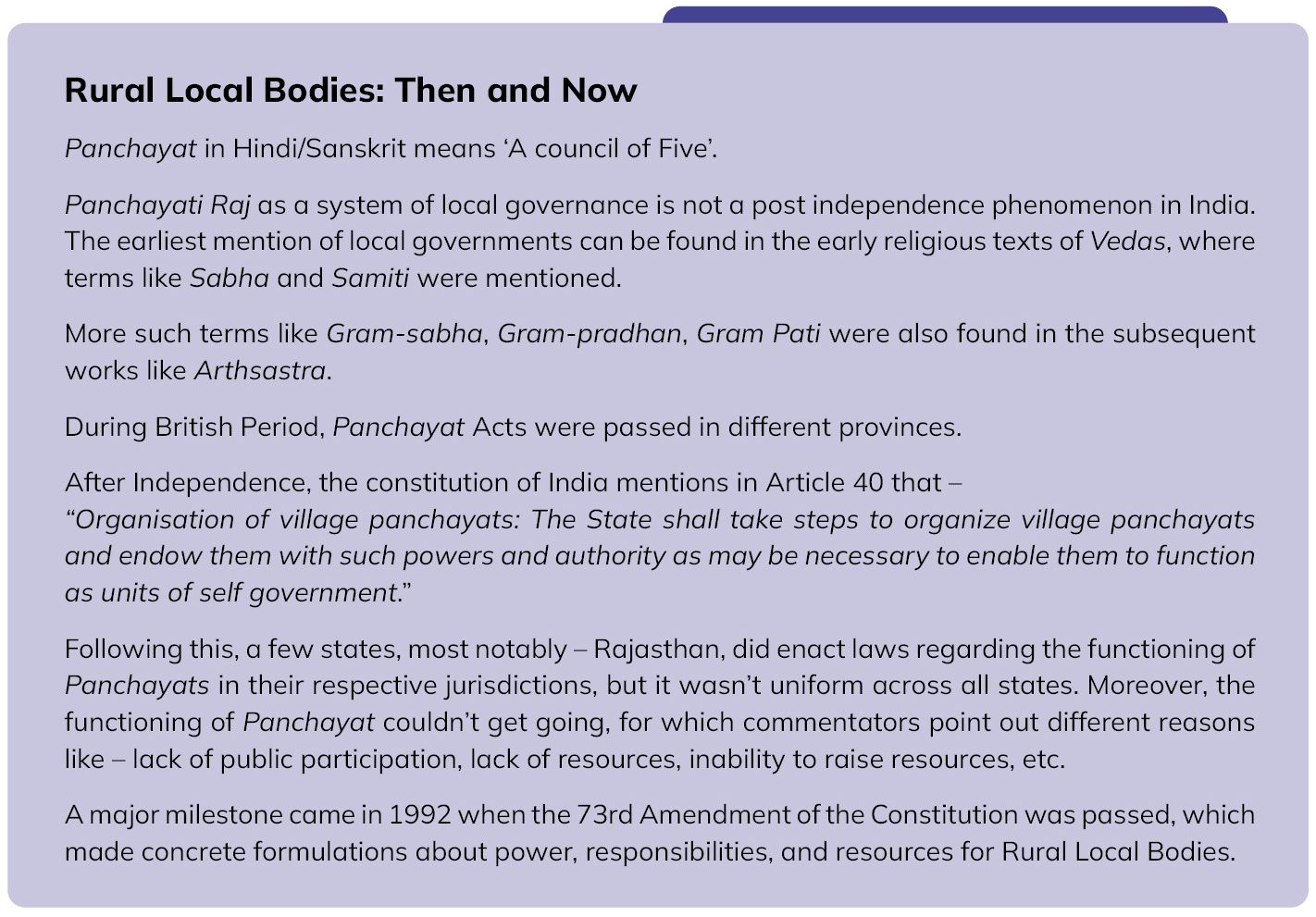

Like Union and State Governments, Rural Local Bodies also derive their powers, functions and responsibities from the constitution of India.

What does the Constitution say?

In the original constitution formulated in 1949, panchayts were envisioned as the units of self governance. The constitution mentioned a directive principle as –

“The State shall take steps to organize village panchayats and endow them with such powers and authority as may be necessary to enable them to function as units of self government.”

(Article 40, Constitution of India, 1949)

However, panchayats couldn’t achieve the role of local governance that was envisaged. Commentors point out various reasons for this, like – it being merely a directive principle and not obligatory policy, limited powers assigned, neglible resources, public non-participation due to various socio-political reasons.

Over the years, different committees made different recommendations for improving the functioning of RLBs. In this process, the most important step came in 1992, when changes were made in the constitution with regard to RLBs.

These changes, known as 73rd Amendment to the constitution, made it a constitutional obligation on the states to enact Panchayati Raj Acts. The constitution has mandated concrete provisions for the structure of panchayats, election, reservation, duration, formation of state finance commission for resource sharing between states and local bodies, etc. However states have also been given some autonomy to organise panchayats according to their own geographical and political-administrative system.

What are Powers and Functions of RLBs

States are required by the constitution to enact necessary laws so that RLBs have necessary powers to function as units of self governance. Constitution lists out the areas where RLBs are supposed to work in the eleventh schedule. There are 29 subjects where the RLBs have power. These are listed in Figure 2.

Figure 2 : Powers and Functions of RLBs (Eleventh Schedule of Constitution)

While these 29 subjects are listed in constitution, this list is an indicative list and hence is not mandatory for the states. States have been provided with some flexibility in framing their own panchayati raj acts, and hence there are differences across states in overall powers and functions assigned to the rural local bodies. Other than working on their own in these 29 subjects, panchayats can also work as an administrative unit of implementation in Central or State schemes.

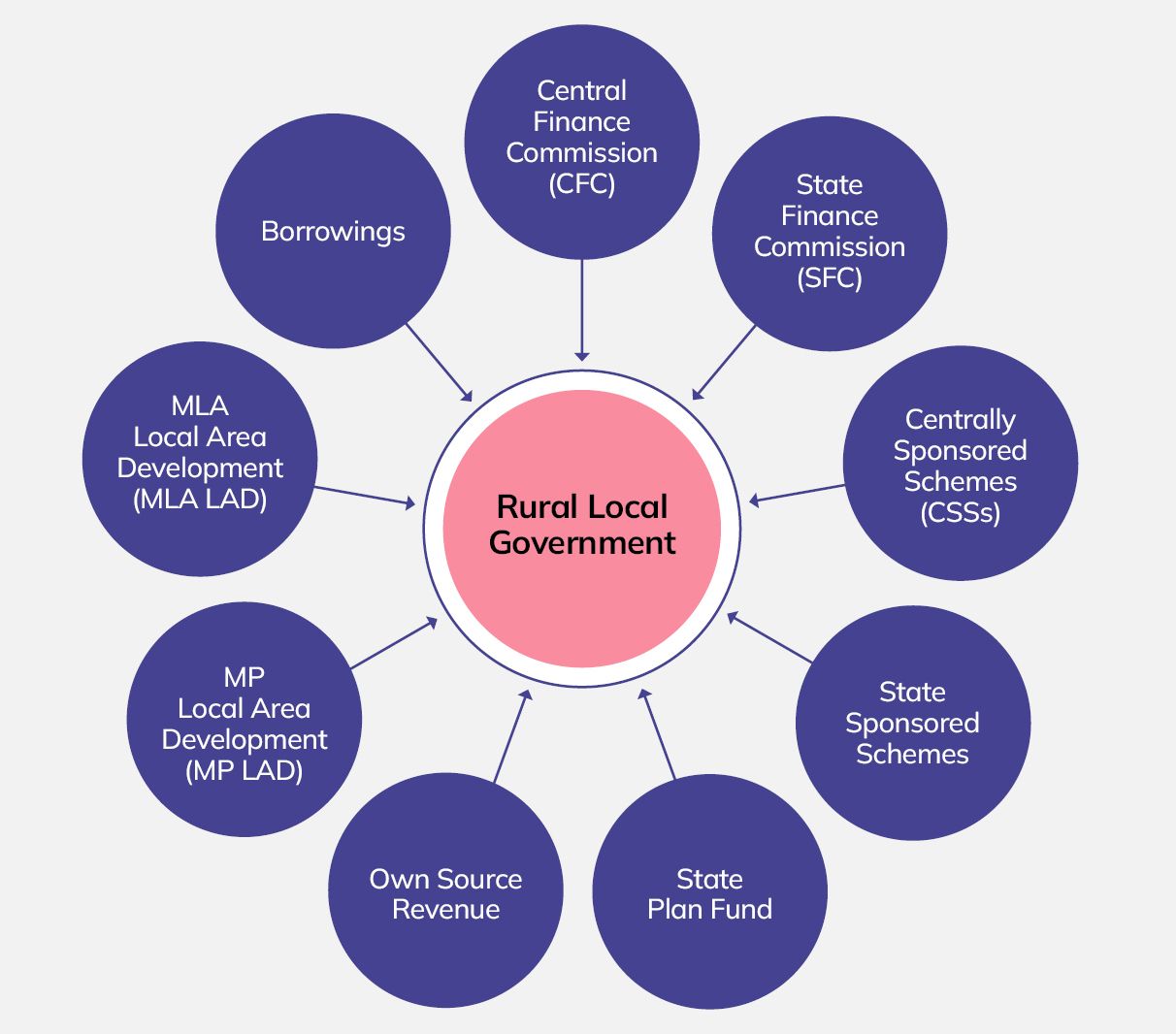

Panchayats can raise financial resources mainly from four sources. These are (i) own tax revenue; (ii) own non-tax revenue; (iii) trasnfers from union and state governments; and (iv) borrowing. The full potential of these four sources continues to be underutilised by most RLBs.

Own Tax Revenue

Major cources of own tax revenue of RLBs are as follows:

House building tax/Property tax – it is generally levied on non-movable property like land and building.

Profession tax – this is a tax levied on the professionals who have salaried jobs within the area of RLB or some of the other commercial activities.

Vehicle tax – it is levied on the sale/use of vehicle within a RLB. The rate is generally decided as the percent of price of vehicle.

Tax on fairs and other entertainments – it is levied on the various forms of commercial entertainments, like – movie theatres, sports events, art exhibitions, amusement parks, etc.

Tax on advertisement – it is generally levied on the advertisement (banners/hoardings) displayed on buildings or land.

Levy on factories in lieu of taxes – this is levied on the manufacturing units located within the panchayat

As mentioned earlier, powers of individual panchayats are derived from the panchayati acts of individual states. Hence, all these taxes are not likely to be assigned to all panchayats in the country, but there will be state level variations. Also, even when a panchayat has the power to levy certain tax, in practice, it has been seen that very few RLBs actually implement and enforce taxes. This might be due to local socio-polotical factors, or the local governments lacking administratve capacity to enforce tax collection.

Own Non-Tax Revenue

Major sources of own non-tax revenue of RLBs are as follows:

Water fee – this is levied for suppy of water for drinking, agricultural, or industrial use.

Street cleaning fee/ Drainage fee – this can be levied in lieu of service employed by the RLBs to clean streets, garbage collection, or maintain drainage.

Sanitary fee for public latrines – this is levied as the user fee in the public toilets.

Fee for the use of panchayat shelter – the buildings / land owned by panchayats which are not used regularly can be leased out for user fee.

User charges for hospitals and schools – certain services provided by schools and hospitals can invite user fee.

Fee on markets and weekly bazaars – in rural areas, bazaars are generally held in public land. Fee can be levied on such bazaars.

Birth and death registration fee– the RLBs are also entrusted with the task of issuing birth and death certificates. They can charge a certain amount for the same.

Similar to taxes, not all non tax revenue sources are available to all panchayats as it depends on the state legislations about panchayats.

Transfers from Union and State Government

The 73rd amendement of the constitution also provides a provision where the state governments have to constitute State Fiannce Commissions (SFCs) every five years. The SFC will make recommendations about sharing of resources between state and the local bodies (both rural and urban).

Thus, transfer from state government is another major sources of revenue for the RLBs. These revenue can be broadly divided into two parts –

Mandatory Shared Resources – It is based on the recommendations of the SFC, which is generally the share in the divisible pool of resources raised by the respective states, where the divisible pool can be defined as per the state laws.

Discretionary Transfers/Grants-in-Aid: The local bodies receive such aid from State Governments from time to time. There is no specific system of grants-in-aid, and these depend on the policies of the government of the day. The grants can also be given either to incentivise tax efforts or to match the effort in the maintenance of services.

Though, constitutionally all states are required to constitute SFCs every five years, not all states have done so. On the other hand, Union Finance Commisions have recommended to the Union Government to provide grants for local bodies starting from 10th Finance Commission onwards.

Broadly, the transfer from Union Government to the RLBs can take following form –

Tied Grants – these grants are generally received by the RLBs to carry out activities as part of national schemes. For example – under Fifteenth Finance Commisson’s period, panchayts are to receive fund to implement a Centrally Sponsored Scheme known as ‘Jal Jeevan Mission’. Similalry, RLBs also have been receiving funds to implement other Centrally Sponsored Schemes (CSS) like MGNREGS etc.

Untied Grants – these are grants which the RLBs can spent their own discretion. The guiding principle is that this amount is to be spent on the 29 subjects listed in the eleventh schedule of the constitution.

Figure 3: Sources of Funds for the Rural Local Bodies

Borrowing

While RLBs, like other tiers of government, can raise money through borrowing, currently it is still a more theoratical idea in India than the one actually practiced. The ability to raise money via borrowing ultimatey depends on the perceived ability to repay the loan as well as interest arising out of these borrowings. Currently, most RLBs lack significant and regular sources of revenue other than transfer from Union and State Governments.

Other than these four sources, in some states, RLBs can have few additional sources of revnue too. For example in states like Rajashthan and Kerala, the budget books of RLBs also reflect the MP/MLA Local Area Development (LAD) funds. And in Kerala, RLBs receive transfer from state government in the form of state plan fund for implementing state scheems too. However, these specific sources are practiced only in a few states in India.