Much like the Union Budget, State budgets, too, are typically associated with the State Finance Minister presenting the Budget in the State Assembly/Vidhaan Sabha. While that exercise is the public presentation of the State budget, there is a lot of work that goes on in the background to draw up the budget, as well as to execute it. At the outset, it is critical for a State Government to get a sense of where it can raise money for its Receipts Budget and how much. Simultaneously, the government also needs to assess where the money raised will be spent, to draw up its Expenditure Budget. In addition to receipts and expenditure, the State Budget will need to include a few other key documents, such as the Detailed Demand for Grants, Gender Budget Statement and Statement on the Welfare of Children, etc. Given all these factors, it is crucial to gain an understanding of the multi-dimensional aspects of State budgets and the various steps involved in finalising them. With this in mind, the current chapter has been divided into the following parts:

Where the State Governments raise money from

Where the State Governments spend money on

What the main budget documents are

All three points are discussed in greater detail in the sections that follow.

The budget process of the State Governments is fairly complex and long. For a discussion on the different stages of budgetary process of State Governments, please refer to chapter 6.

It should be noted here that States have some degree of autonomy with regard to their budgets. So, there can be differences across States in each of these three aspects.

State Governments have a number of sources to raise money from. Given below is the list of sources from which State Governments may raise money:

States’ share of Central Taxes

According to the Constitution of India, the Union Government is required to share a part of all the tax revenue that it raises with State Governments. This part of the tax collection that the Central Government shares with State Governments is known as the States’ Share in Central Taxes.

States’ Own Tax Revenue

There are many taxes that are either levied by State Governments, or where the collection goes directly to State Governments. Except Goods and Services Tax(GST), the rates of such taxes are determined by State Governments, and hence there is a variance across States. The main taxes that contribute to state governments’ revenue are:

Goods and Services Tax (GST): While GST is levied at the national level and the decisions regarding GST are taken by the GST Council, components of the total GST collection, known as State GST (SGST) and part of integrated GST (IGST) goes directly to State Governments.

State Excise Duty: As with Union excise duty, this is levied on the production of goods that are not under GST. After the introduction of GST, the main item on which State excise duty is applied is alcohol.

Sales tax and VAT: There are certain items whose sale is not covered by GST. The sale of such items falls under the State sales tax or State value added tax (VAT).

Stamps and Registration Duty: This is generally levied on the sale of land and/or immovable properties such as flats/houses/buildings.

Vehicle Registration Tax: As the name suggests, this tax is applied on the registration of new vehicles or in the case of a change in the ownership of a vehicle.

Entertainment Tax: This levy is generally applied on the sale of movie tickets, etc.

States’ Non-Tax Revenue

Apart from tax revenue, States also have other sources to raise revenue from. The most important among these are:

Lease/sale of natural resources – states can either sale or lease out natural resources for the economic purposes for which they receive receipts. Lease of minerals is major source for many states, such as Odisha, Jharkhand and Chhattisgarh, among others.

Economic services: there are certain services provided by the government for which it charges the user, such as - irrigation, health, education, forestry and wildlife, etc. The user charges are not done with the purpose of profit, and are generally much lower than the charges by private sector. Nonetheless, they do provide some revenue to the government.

Sale of lotteries – some states engage in the activity of selling lotteries, and the net proceeds from these goes to the government funds.

Interest receipts – state governments can provide loans to certain entities like public sector undertakings (PSUs), local bodies, etc. This the interest received on such loans.

Borrowings

As with the Union budget, when the expenditure of a State Government exceeds the receipts, it borrows money to bridge the gap. This borrowed money, however, needs to be repaid with interest.

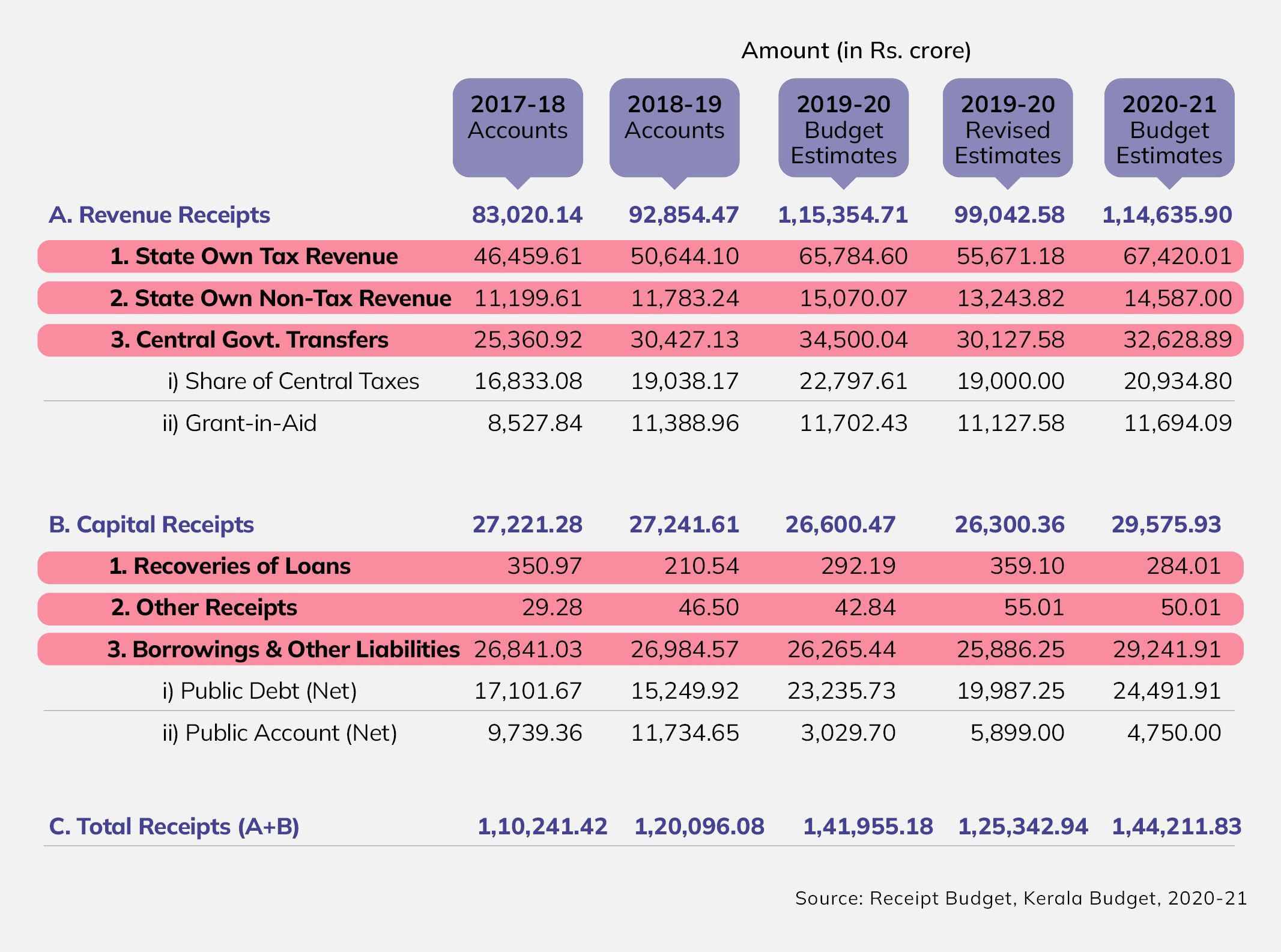

Figure 1 provides a snapshot of Kerala’s Receipts budget for 2020-21.

Figure 1: Kerala Receipts Budget, 2020-21

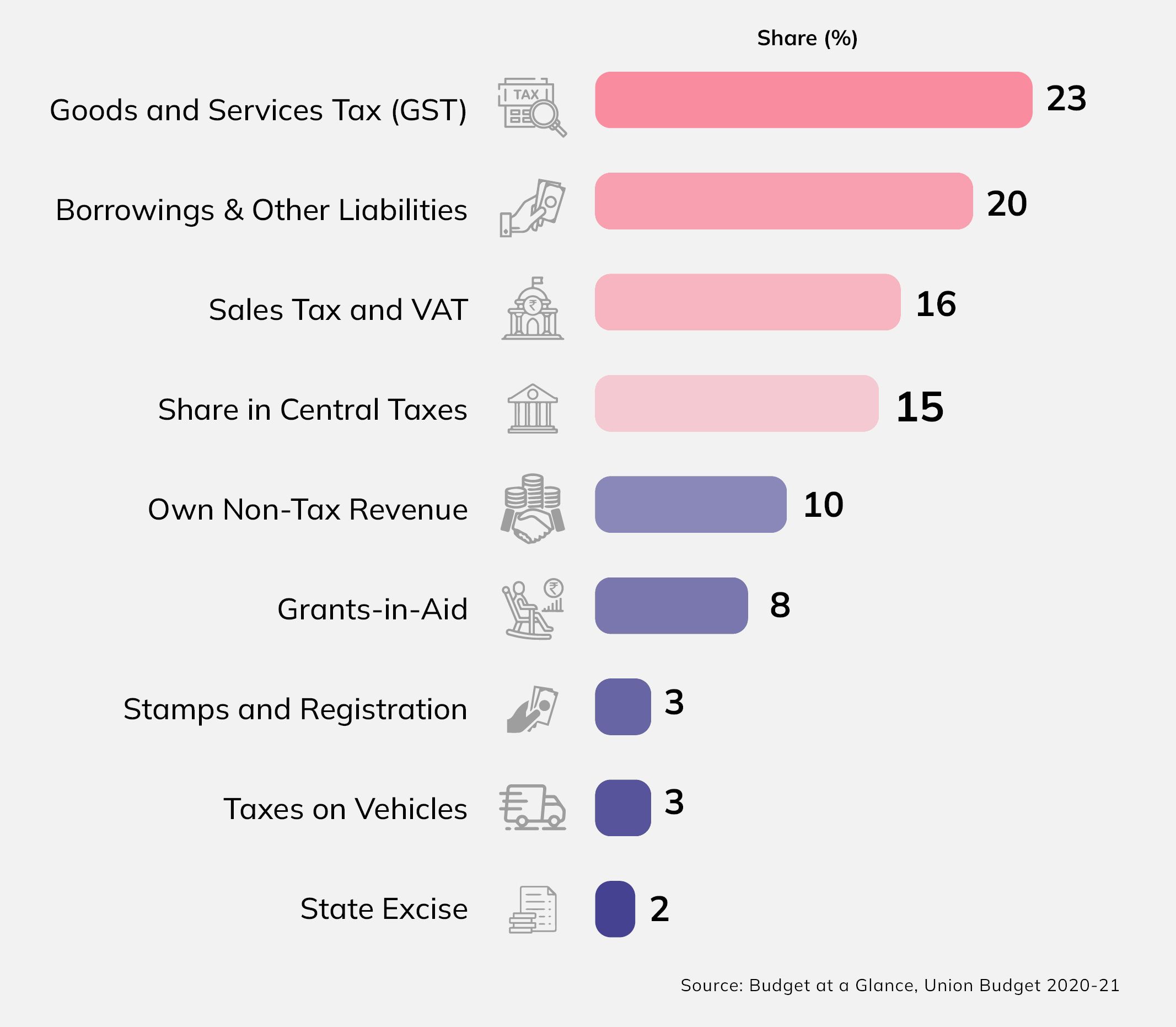

Figure 2 provides a further breakup of Kerala’s receipts, and presents them in an analytical form.

Figure 2: Components of Kerala’s Receipts Budget 2020-21

Kerala’s own tax revenue consists of GST, sales tax and VAT, stamps and registration, taxes on vehicles, and State excise. All these combined contribute 47 per cent of Kerala’s total receipts, and are the largest source of revenue for the State, with its share in Central taxes being the next largest source.

It should be noted that different components contribute differently to the receipt kitty across different States. In other words, for States other than Kerala, the share of contribution of these sources will be different.

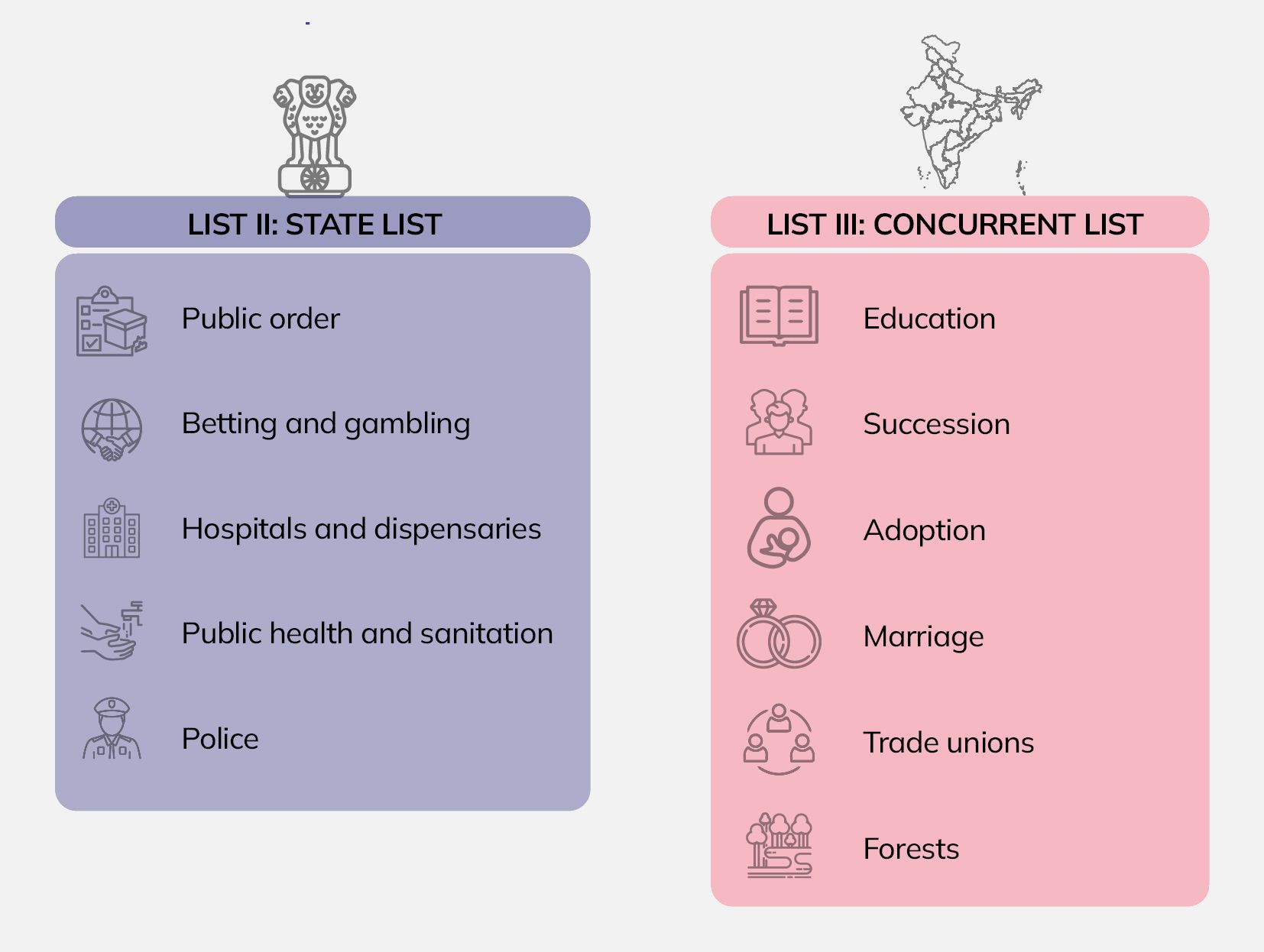

The Constitution of India mentions the areas/items for which State Governments are responsible, either fully or jointly, with the Union Government.

Figure 3: Responsibilities of State Governments

The State list refers to those areas for which State Governments are solely responsible, while the Concurrent list contains items that are the joint responsibility of both State and Union Governments. These responsibilities decide where the State Governments spend their money.

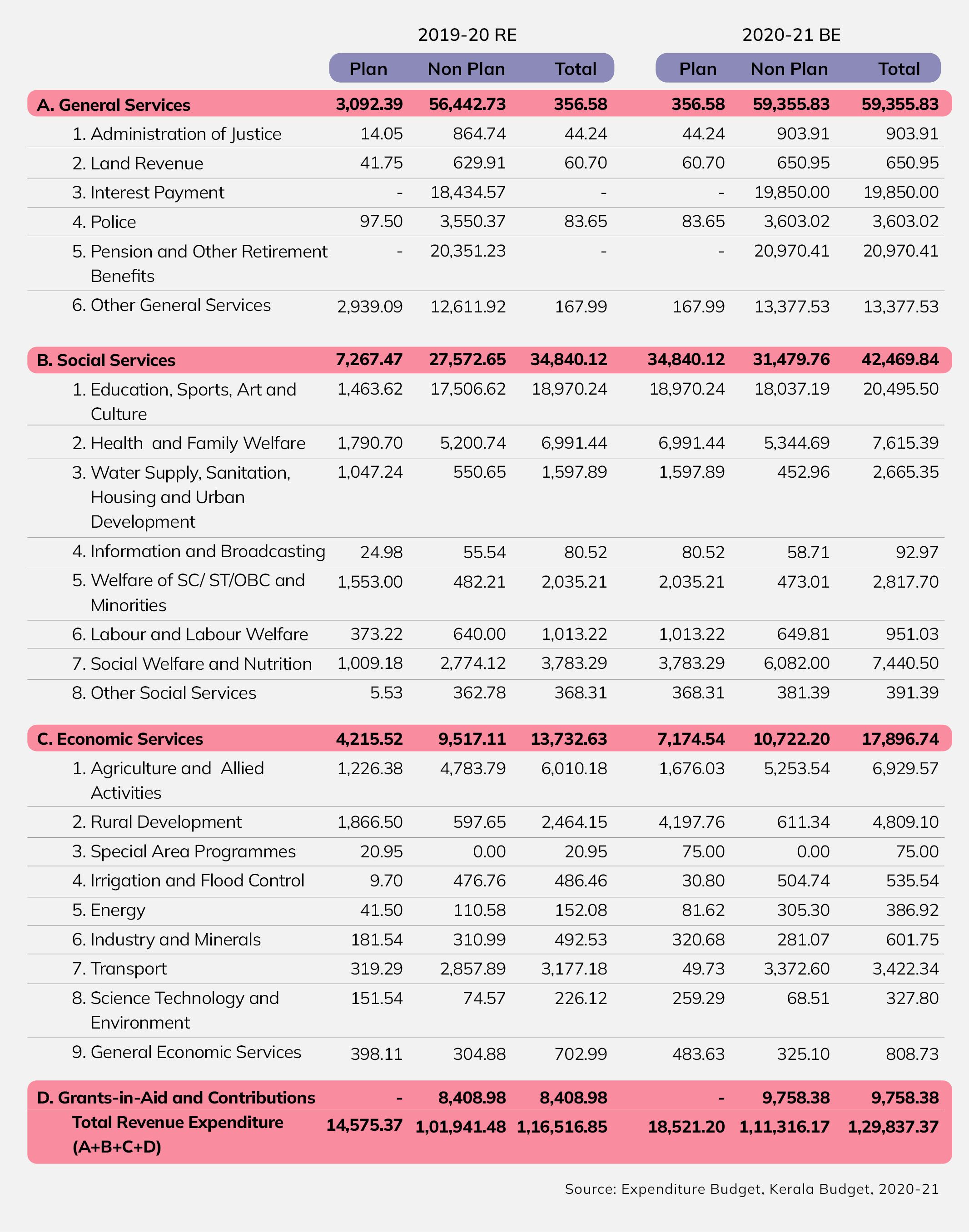

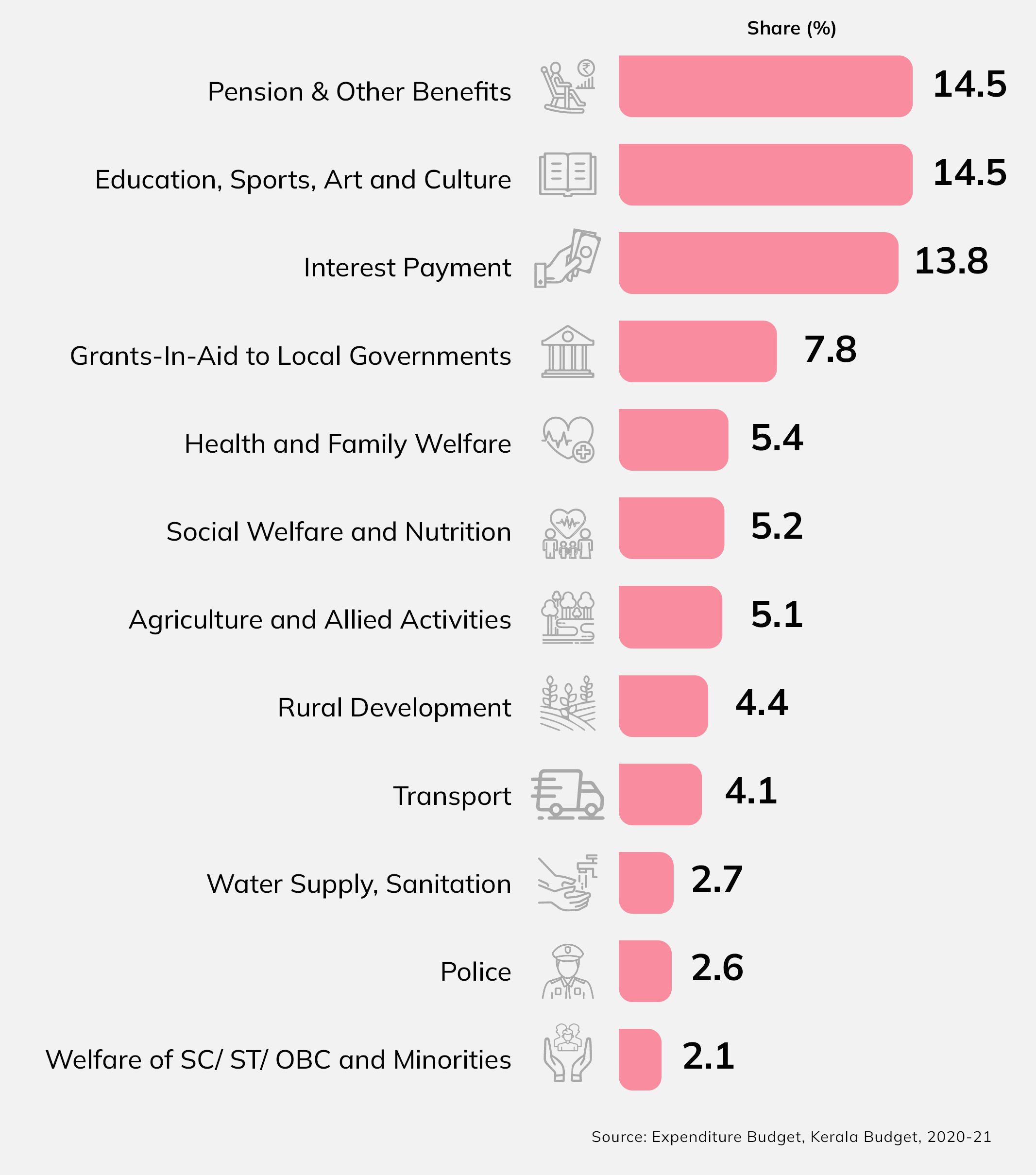

Figure 4 provides a snapshot of the list of items on which the Kerala Government planned expenditure in its 2020-21 budget.

Figure 4: Revenue Expenditure in Kerala’s 2020-21 Budget

While this only refers to revenue expenditure, State Governments also spend funds under the capital account. Nonetheless, column 1 of Figure 3 provides the major categories on which State Governments spend their money.

Figure 5 provides the total of revenue and capital expenditure, and its share in the overall budget of the Kerala Government.

Figure 5: Broad heads of Expenditure for the Kerala Government, Budget 2020-21

This is not an exhaustive list of all the expenditure items. The items mentioned in Figure 4 accounts for about 82 per cent of the State’s total expenditure.

4.

What are the Budget Documents for a State Government?

Similar to Union Government, State governments are also required by constitution to present a few essential documents for budget process. These are –

Annual Financial Statement: Under Article 202 of the Constitution of India, a statement of the estimated receipts and expenditure of the State for each financial year has to be laid before the State Legislature. This Statement is known as the “Annual Financial Statement” (AFS) or “Budget”. It is the core budget document that presents the estimated receipts and expenditure of the State Government for the forthcoming financial year. This document also provides revised estimates of the current fiscal year as well as actual receipts and expenditure made during the last fiscal year.

Demands for Grants - Article 203 of the Constitution mandates that the estimates of expenditure from the Consolidated Fund of the State are voted by the Legislature. The statements of these expenditure are to be presented to the legislature in the form of Demands for Grants. Generally, one Demand for Grant is presented for a Ministry or Department. However, in the case of large Ministries or Departments, more than one Demand can also be presented. Each Demand for Grants classifies the total expenditure into 'voted' and 'charged' and 'revenue' and 'capital' heads of account. Generally, there are two documents associated with ‘Demands for Grants’ - one summary and one detailed. In the summary document, the total for each ministry/department is given with the breakup into voted and charged. In the detailed documents, further breakup of expenditure into the level of minor head is given.

Finance Bill – This is the document with proposals from the government regarding changes in the tax regulation of the state. This is to be voted by the legislature, and passing of it is essential for the proposals to come into effect. The Finance Bill is a money bill and the requirement to present a finance bill in the budgetary process is mandated in the Articles 198, 199 and 207 of the constitution of India.

Appropriation Bill – this is the document presented to the legislature for voting that provides the state governments necessary legal authority to spend money from the consolidated fund of the state. The requirement for presenting an Appropriation Bill is given under article 204 of the constitution of India, while according to the articles 205 and 206, no expenditure can be incurred from the state’s consolidated fund without the passing of such appropriation bill by the state assembly.

Supplementary Grants – Sometimes state government feel the need to spend more money than approved in the annual budget. In such cases, Article 205 of the Constitution allows the State Government to present the proposal for extra spending to the state assembly in a format similar to ‘Demand for Grants’. These proposals are known as ‘Supplementary Grants’. It is not compulsory for a state to present Supplementary Grants. States do present them when they feel the need to incur expenditure over and above the amount authorised in annual budget. A state can present maximum three Supplementary Grants in a financial year.

While these five documents are constitutionally required, due to the expansive nature of budget, State Governments also present a number of other documents which helps explaining the budget, as well as can be used to highlight specific details of the budget.

Budget Speech: A word transcript of the speech that the finance minister makes while presenting the budget in the State legislature or Vidhaan Sabha.

Budget Summary: A summary of the main features of the budget. Sometimes it is also called ‘Budget at a Glance’ or ‘Budget in Brief’.

Key to Budget Documents: Provides a brief introduction to all the other budget documents, and explains what information they contain.

Receipts Budget: Provides detailed information of how the Government intends/expects to raise money from different sources. It gives the estimated amount with corresponding sources.

Expenditure Budget: Provides detailed information about all the expenditure that the Government plans to incur during the year. It provides the amount corresponding to different ministries/ departments and further breakup.

Expenditure Profile: A summary of the total expenditure of all ministries. It also presents expenditure according to different categories of interest, that is, the summary of funds allocated to schemes for women, children, scheduled castes, scheduled tribes and religious minorities.

Economic Survey - It is a document prepared by the ministry of finance which provides details of the state of economy of the ongoing year. The entire document is generally divided into two parts, where the first part presents the analytical/qualitative description of economy and country in general, second part provides the statistical data of all major sectors, as well as any other important economic data.

Memorandum: This supplementary document to the Finance bill explains the various legal provisions of the Finance Bill.

Documents under Fiscal Responsibility and Budget Management (FRBM) Act – FRBM act was passed by Union Government in 2003, and State Governments also enacted their own FRBM acts with a view to manage debt. The Act requires publication of documents. While the actual title of the documents may differ across state, most common titles are - Macro-Economic Framework Statement, and Medium-Term Fiscal Policy cum Fiscal Policy Strategy Statement. These both documents combined provide the government estimates of near future growth, its estimates about debt and few other macroeconomic indicators.

Gender Budget Statement: This statement refers to schemes and programmes prepared and implemented under the gender budgeting framework. It generally contains details about schemes that have 100 per cent allocation for women, or at least 30% allocation for women.

Child Budget Statement: Refers to schemes and programmes prepared and implemented under the child budgeting framework. It generally contains details about schemes that have 100 per cent allocation for children, or at least 30% allocation for children.

Outcome/Performance Budget Statement: Outcome Budgeting is a framework for goal setting for a particular policy or department, as well as evaluation of the performance of policy/department against those goals. These goals are defined quantitatively and generally the time period is also given. The Outcome Budget Statement presents the details of such goals for each policy/department, as well as state’s performance in achieving last year’s goals

Statement on Allocation for Welfare of Scheduled Castes: Given the lagging development status of schedule castes, many state governments make plans/schemes which are aimed at the welfare specifically of schedule castes. This document provides the allocation for schemes which are either fully or partially aimed at welfare of scheduled caste.

Statement on Allocation for Welfare of Scheduled Tribes: Similar to ‘schedule caste’, the schedule tribes also lag in the development indicators relative to general population. To correct this, many state governments make specific plans/schemes for scheduled tribe. This document provides the allocation for schemes which are either fully or partially aimed at welfare of scheduled tribes.

Agriculture Budget Statement: This document refers to the policies/schemes meant specifically for agriculture. The document provides the details of the policies as well as the corresponding allocations.

Nutrition Budget Statement: Many states have prioritised the goal of improving the nutrition level. Such states make specific policies aimed at improvement of nutrition. This document provides the details of such policies and the corresponding allocations.

Citizen Budget: while the budgets are made for the welfare of common citizen, traditionally they have no role in the preparation of budget. Some states have taken initiative where the citizens can provide feedback or make demands regarding budget. This can be done either in physical form, such as pubic meeting of government officials with citizens, or through other means such as online responses. A budget prepared taking the views of common citizen is known as Citizen Budget. This document generally provides the initiatives the government took to get the vies of the citizens, as well as how many demands/feedbacks were put to use in the actual budget.

Since State Governments have freedom with regard to formulating their budgets, not all State Governments present all the documents mentioned above. In fact, variance in the documents presented across states, especially the documents which are aimed at specific policy/group, like gender budget statement, child budget statement, etc. can be used to gauge the differences in the policy priority of the different State Governments.