While India’s national ‘Budget’ is typically associated with the finance minister’s presentation in Parliament, that is only a small part of the entire budgeting exercise. There is much more to it. The entire budgetary process is a fairly lengthy and drawn-out process, and hence understanding the different stages / steps is important in order to understand the Union Budget of India.

Firstly, since any budget is essentially a statement of anticipated receipts and expenditure, it is imperative to understand the sources from which the government can raise — and does raise — money. Similarly, it is important to know on what the government can spend — and does spend — the money raised. In the budget, both these details are presented in documents known as receipt and expenditure budgets, respectively. However, receipt and expenditure budgets are not the only documents presented in the budget. Due to the complex nature of a Government budget, a few other documents are also presented.

Keeping in mind the need to understand these multi-dimensional aspects of the budget, this chapter has been divided into three sections:

1. Where the government raises money 2. What the government spends money on 3. What the main budget documents are

All three of these are discussed in greater detail in the sections that follow.

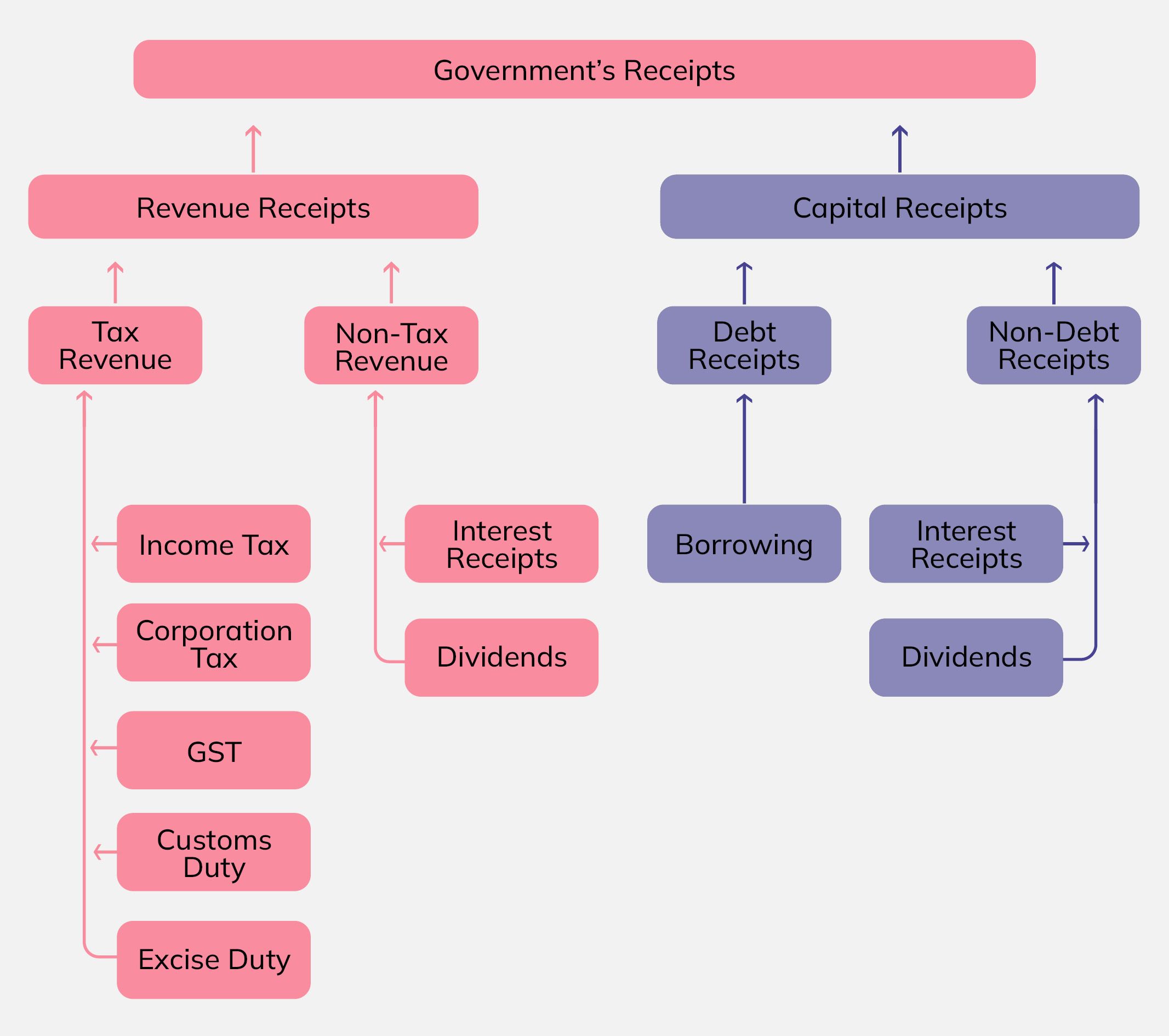

The Union government has many sources from which to raise resources, and there are different ways to categorise those sources. Figure 1 provides the breakup of the Union government’s receipts, classified as capital and revenue receipts.

Figure 1: Sources of Union Government’s Resources

Each of the sources is discussed below in detail:

Tax Revenue

Income Tax: This is a tax on the income of individuals, firms etc. other than companies, under the Income-tax Act, 1961. This head also includes other taxes, mainly the Securities Transaction Tax, which is levied on transactions in listed securities undertaken on stock exchanges, or more popularly known as share market.

Corporation Tax: This is a tax levied on the income earned by companies, under the Income-tax Act, 1961.

Goods and Services Tax (GST): GST is a tax on supply of Goods or Services or both except on supply of fuel, alcoholic liquor for human consumption and a few other items. It was introduced on July 1, 2017.

Customs Duty: This duty is levied on the international/cross-border trade of goods.

Excise Duty: This levy is imposed on the manufacture of goods. Since the introduction of GST in 2017, excise duty is levied only on the manufacture of goods not covered by GST.

Wealth Tax: This is a tax on the stock of wealth owned at a particular time. Generally, the tax code also defines which assets are taxable under wealth tax, and how to value them for the purpose of taxation. In India, wealth tax used to exist but abolished in 2015-16. The reason given was insufficient revenue collection, and high cost of collection.

Non-Tax Revenue

Interest Receipts: This is the interest that the union government receives on loans made to States and Union Territories.

Dividends and Profits: This is the amount that the government receives when public sector enterprises and the Reserve Bank of India transfer their income to the government.

Other Non-Tax Revenue: This broadly refers to the charges levied by the government for particular services, such as economic services, general services, etc. Some examples of such charges are: revenue earned by the railways, postal fees, shipping, civil aviation, user fees, etc.

Non-Debt Capital Receipts

Disinvestment: This, as the name suggests, is the sale of assets owned by the government. These could be part or full ownership of a public sector enterprise, land or other assets owned by the government.

Loan Recovery: This refers to the recovery of loans that the union government normally provides to State governments and Union Territories.

Debt Capital Receipts

Borrowing: This is the amount that the government borrows and hence needs to repay in future. It is also known as a debt receipt.

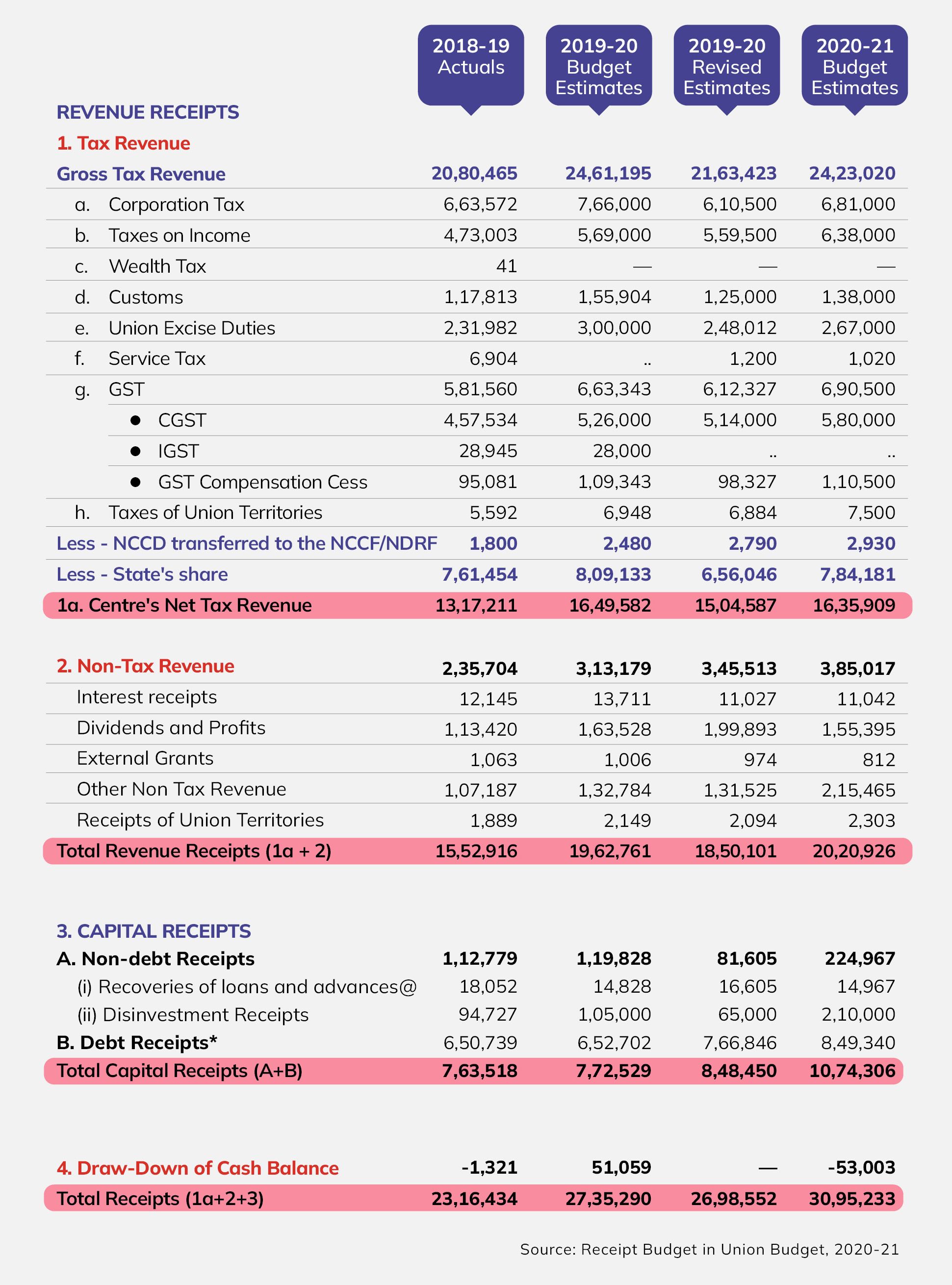

The government’s Receipts budget is presented in different levels of detail. Further descriptions / deep dives for each of the entries are also given in the budget document. Figure 2 is a summarised snapshot of the actual Receipts in Union Budget 2020-21.

Figure 2: Receipts budget in Union Budget 2020-21

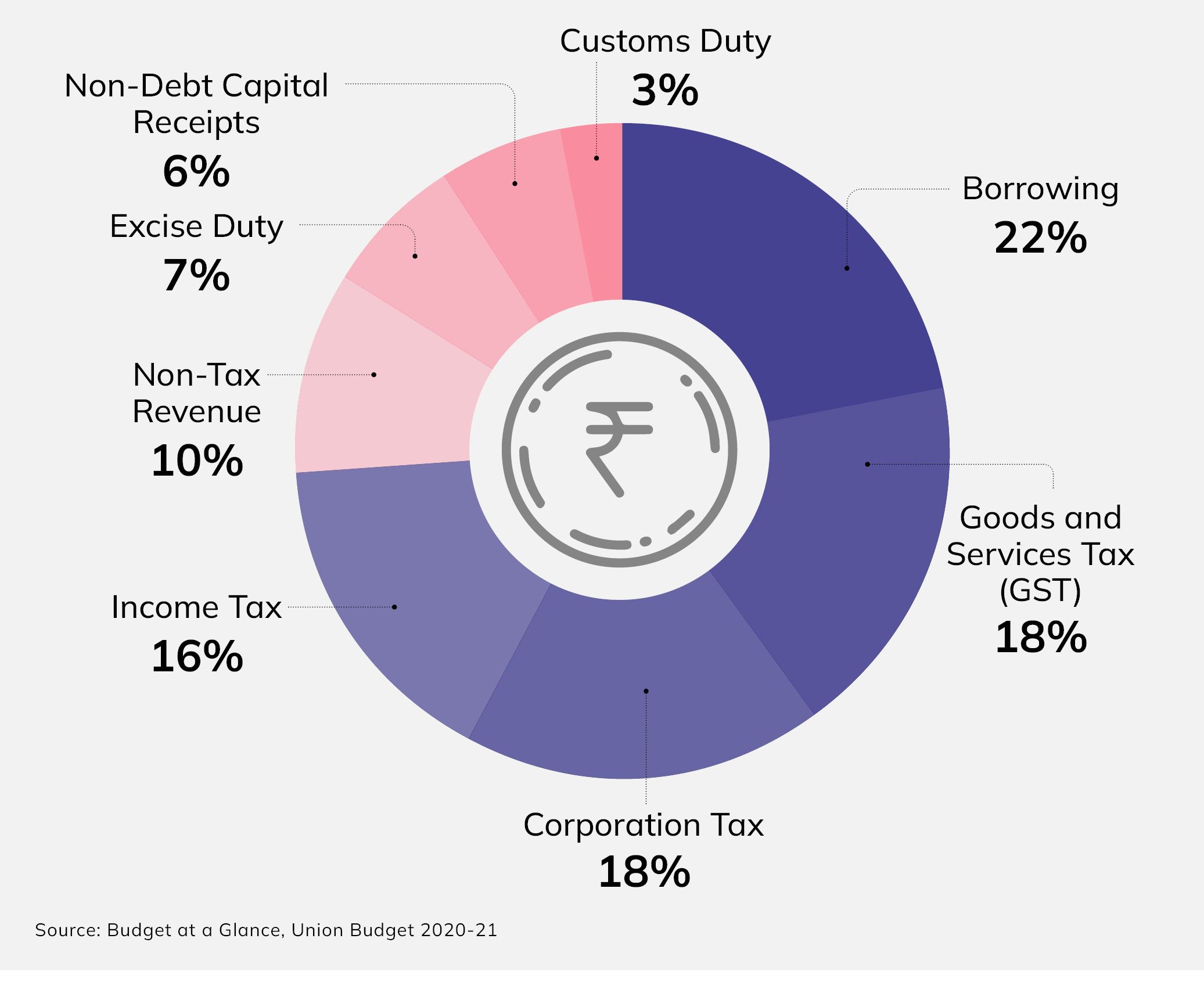

While the numbers provided in the above receipts budget do provide data points; often, to draw useful insights, it is preferable to modify or present the numbers in a manner more suited for one’s analysis. One such presentation is given in Figure 3, which summarises the sources of money for the union government as given in Budget 2020-21.

Figure 3: Where the money comes from, Union Budget 2020-21

Note – this includes the tax revenue which are part of states’ share in central tax collection.

While presented in this form, it is easy to see that 62 per cent of the union government’s receipts come from taxes, while non-tax, non-debt sources make up about 16 per cent. Borrowing accounts for 22 per cent of the resources of the union government.

As with receipts, expenditure, too, can be classified in different ways. And much as with receipts, expenditure can be classified as capital expenditure and revenue expenditure. In addition, there are other classifications at the sectoral or ministry wise levels. Here, we look at three types of classification (a) Voted vs Charged (b) classification given in the ‘Budget at a Glance’ document (c) Ministry-wise classification.

Voted vs Charged

Expenditure that has to be authorised by Parliament is called ‘Voted Expenditure’, while expenditure that is automatically debited from the Consolidated Fund of India is called ‘Charged Expenditure’.

Expenditure that is part of the budget, wherein the government decides how much it wants to spend, is voted expenditure. It includes expenditure on areas like education, health, sanitation, infrastructure, etc. In contrast, charged expenditure is independent of the government’s authorisation or voting. Examples of charged expenditure are interest payments, salaries of the President, Lok Sabha speaker, etc.

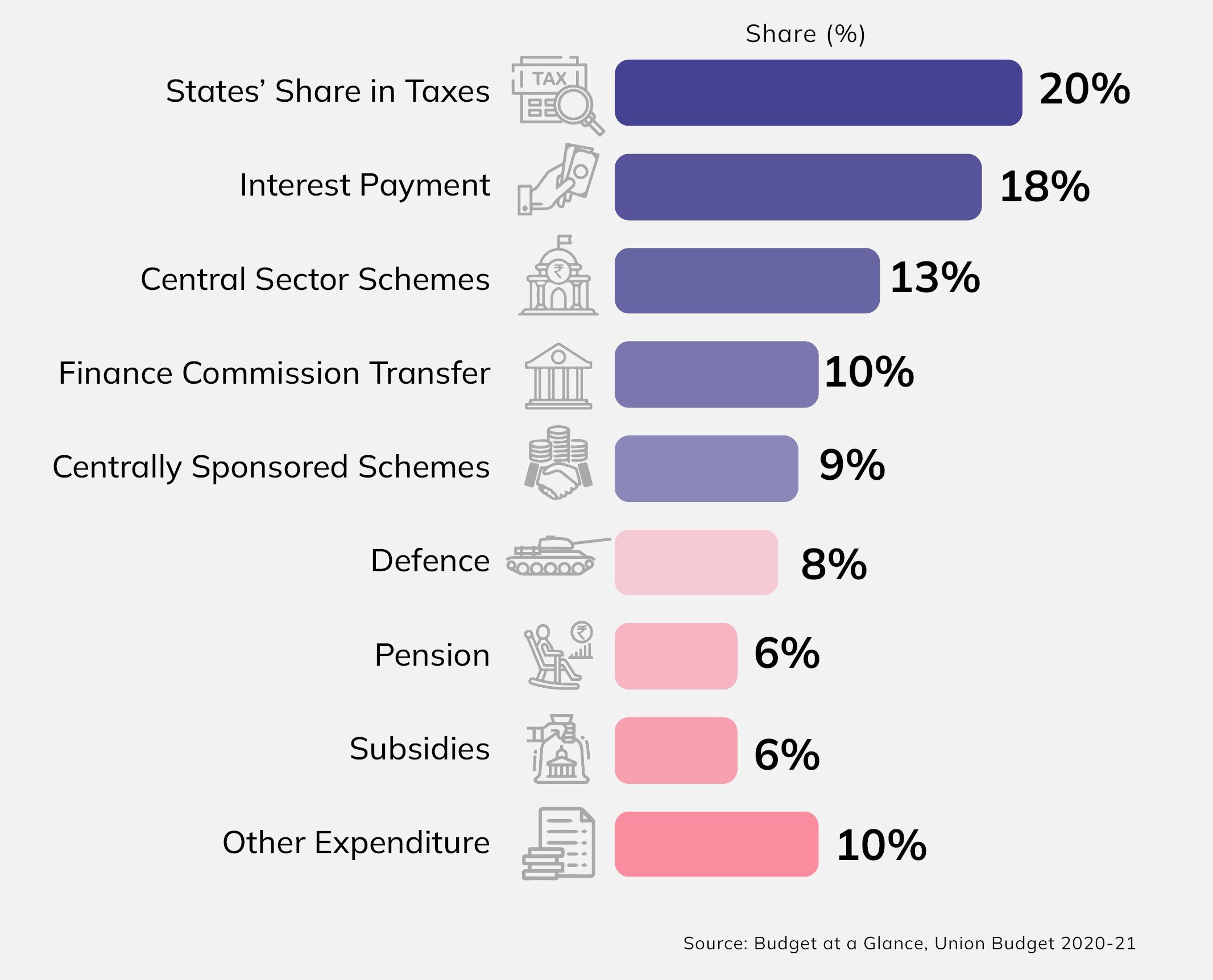

Expenditure as classified in the ‘Budget at a Glance’ Document

Figure 3 provides the breakup of union government expenditure as reported in the Budget at a Glance document.

Figure 3: Where the Money Goes, Union Budget 2020-21

Some of the items of expenditure are explained below.

States’ Share in Central Taxes: The constitution of India requires the Union Government to share a part of the taxes it collects with the States. This head refers to that amount. However, States Share in Central Taxes does not constitute part of the Consolidated Fund of India or the Union Budget. This amount is kept outside the Consolidated Fund of India and shared with the Sates before the Union Budget is decided every year.

Interest Payments: This includes interest paid on debt such as Treasury Bills, Market Loans, securities issued against small savings collection, State provident funds and insurance and pension funds.

Central Sector Schemes: This is the expenditure incurred on schemes that are financed fully by the Union Government. Some examples of this type of schemes are - Pradhan Mantri Kisan Samman Nidhi (PM-Kisan), Urea Subsidy, North East Special Infrastructure Development Scheme (NESIDS), Scholarship for College and University students, Pardhan Mantri Swasthya Suraksha Yojana, Prime Minister Employment Generation Programme (PMEGP), etc.

Centrally Sponsored Schemes: Some schemes receive funding both from the union government and States. This head refers to the expenditure of the union government on such schemes. Some examples of this type schemes are - Mahatma Gandhi National Rural Employment Guarantee Programme, Green Revolution, Pradhan Mantri Krishi Sinchai Yojana, Pradhan Mantri Gram Sadak Yojna, Swachh Bharat Mission, National Health Mission, Integrated Child Development Services, etc.

Finance Commission Transfers (Other than Share in Central Taxes): A finance commission, constituted every five years or earlier, makes recommendations to the union government on the sharing of resources between the Union Government and the States. This head refers to the transfer to States on the basis of the recommendations of the finance commission.

Defence: This includes expenditure incurred on the Army, Navy and Air Force in terms of miscellaneous services such as Rashtriya Rifles, J&K Light Infantry, Coast Guard and Research and Development. It also includes revenue expenditure such as pay and allowances, transportation, stores, capital outlay on construction, aircraft and aero engines, vehicles, equipment, the naval fleet, dockyards, etc. This head does not include defence pensions, which are calculated separately under the allocation for pensions.

Pensions: This is the provision for pensions and other retirement benefits of retired personnel of the Defence Services and other civil departments, including pensioner benefits of the employees of the Department of Telecommunications, together with employees absorbed in Bharat Sanchar Nigam Ltd., and funds for the medical treatment of central government health schemes (CGHS) pensioners. This does not include expenditure on social pensions or security measures for widows, mothers, the aged and persons with disabilities.

Subsidies: These include subsidies on food, fertiliser, petrol and petroleum products, interest subsidies, etc.

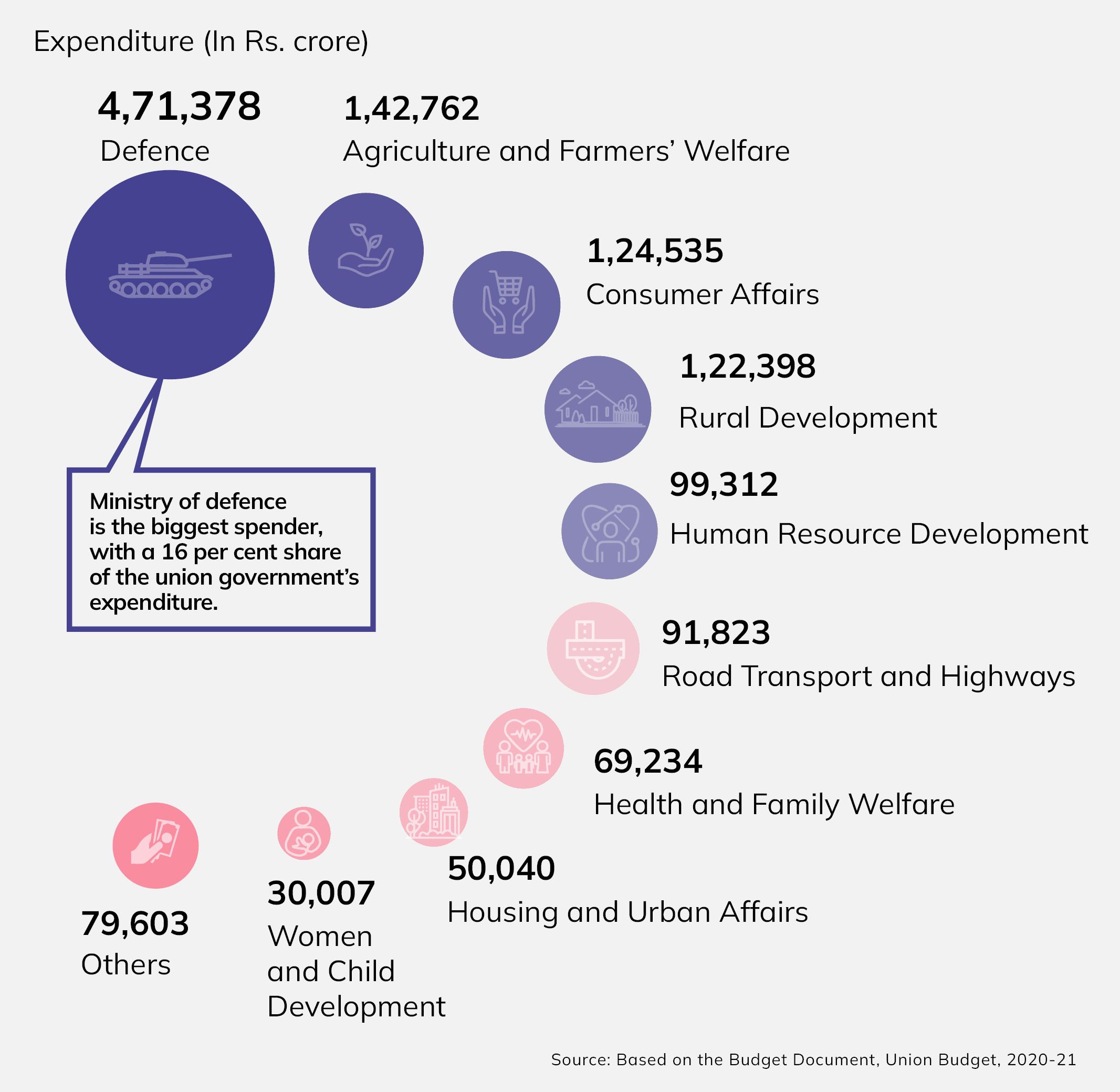

Ministry-wise Expenditure

The expenditure of the Union government can also be classified according to its ministries. It should be noted though that all the expenditure does not go through ministries, most notably, expenditure such as transfers to States and interest payments. Barring such exceptions, the union government’s expenditure can be classified according to its ministries, as shown in figure 4.

Figure 4: Expenditure by Major Ministries, Union Budget 2020-21 (In Rs crore)

At the ministry level, the ministry of defence is the biggest spender, accounting for about 16 per cent of all the expenditure incurred by the union government. Ministry-level expenditure data is helpful in a way that it provides insights on the priorities of the government. The year-on-year change can also be studied to see how the government’s priorities are changing.

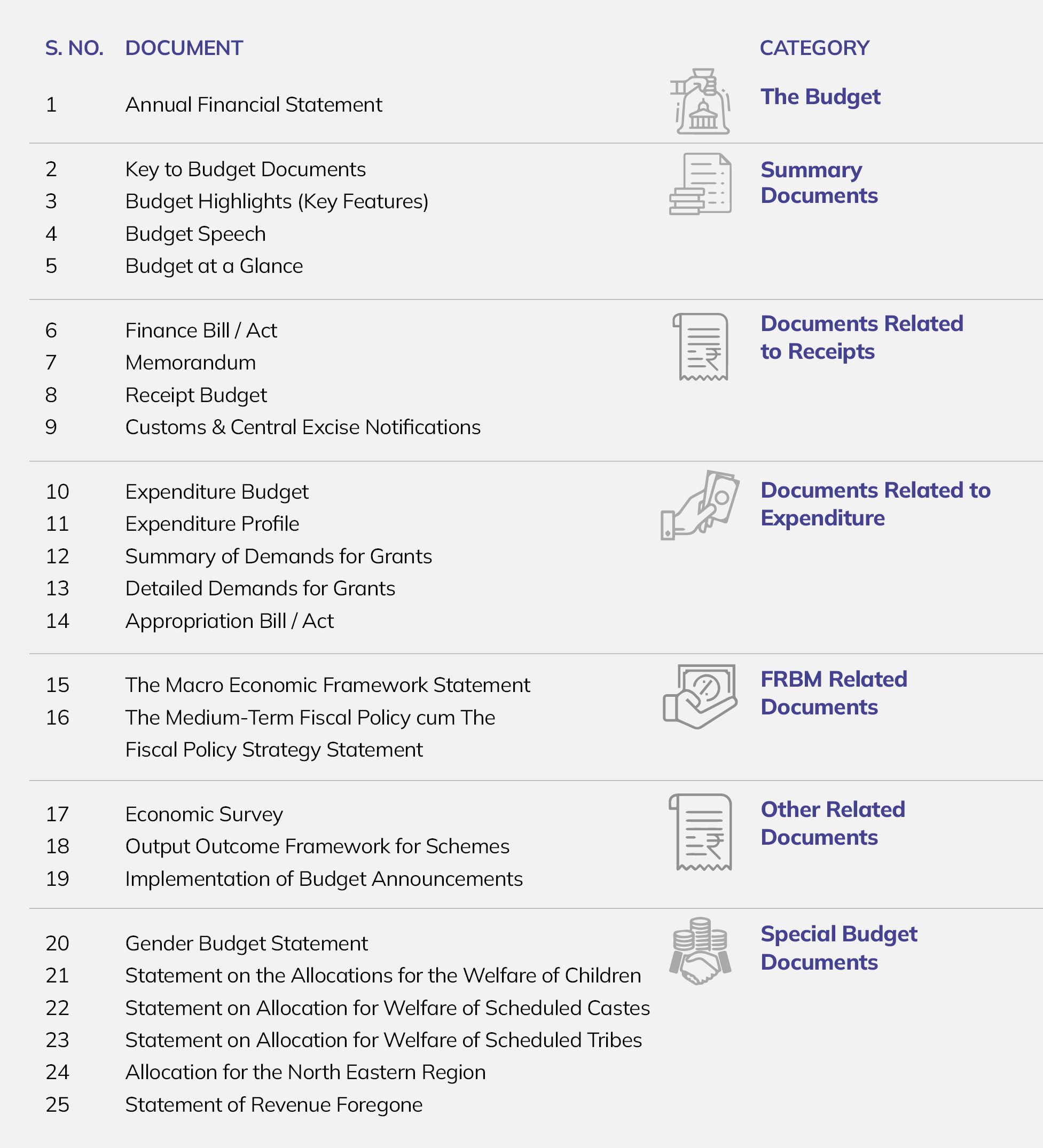

Article 112 of the Constitution mandates the Union Government to lay before both the Houses of Parliament a statement of the receipts and expenditure of the Government of India. This statement is known as the ‘Annual Financial Statement’. Apart from the Annual Financial Statement, the Union Budget has a number of other accompanying documents / reports / statements. Given below is the list of all the documents that are presented with the Union Budget:

Table 1.6: List of Union Budget Documents

All the documents are discussed in detail below –

Annual Financial Statement: This is the ‘Budget’ of the Union Government and is mandated by Article 112 of the Constitution of India. This document provides the estimated receipts and expenditure of the Union Government of India for the financial year for which government presents the budget along with the budget and revised estimate of the on-going financial year and actual for the previous financial year. The receipts and expenditures are shown under three parts in which Government accounts are kept viz., (i) The Consolidated Fund of (ii) The Contingency Fund and (iii) The Public Account. The information presented in this document distinguishes the expenditure on revenue account from the expenditure on other accounts, as is mandated in the Constitution of India. The Revenue and the Capital sections together, make the Union Budget.

Key to Budget Documents: Provides a brief introduction to all the other budget documents, and explains what information they contain.

Budget Highlights: A brief summary of the main features of the budget.

Budget Speech: A word transcript of the speech that the finance minister makes in Parliament.

Budget at a Glance: A summary document that gives more details on the sources of receipts and heads of expenditure.

Finance Bill: This is a Money Bill, as defined in Article 110 of the Constitution, presented in Parliament proposing required changes in the taxation by the government every year. This bill is put to a vote in Parliament and its passage is necessary for the tax changes to be implemented. This is presented in fulfilment of the requirement of Article 110 (1)(a) of the Constitution of India.

Memorandum: This supplementary document to the Finance bill explains the various legal provisions of the Finance Bill.

Receipt Budget: Provides detailed information on how the government intends / expects to raise money from different sources.

Customs & Central Excise Notifications: Provides details on proposed changes in customs rules and tax rates.

Expenditure Budget: Provides detailed information about all the expenditure the government plans to incur.

Expenditure Profile: A summary of the total expenditure of all ministries. It also presents expenditure according to different categories of interest, that is, the summary of funds allocated to schemes for women, children, scheduled castes, scheduled tribes and religious minorities.

Summary of Demands for Grants: During the preparation of the budget, every ministry is required to submit to the finance ministry its proposal regarding the amount it plans to spend and the corresponding items on which it intends to spend the funds. The expenditure also needs to be divided into ‘voted’ and ‘charged’ expenditures. These documents are called ‘demands for grants’. The document presented in the budget as ‘Summary of Demand for Grants’ gives the total amount for each ministry along with breakup into voted and charged.

Detailed Demands for Grants – These demands for grants provide item wise details for each ministry. Along with voted and charged, they also give the breakup of revenue and capital expenditure.

Appropriation Bill: This is the Bill that provides the government legal authority to incur expenditure, or in more technical terms, the authority to withdraw money from government accounts for expenditure. The Bill provides specific details about the amount being withdrawn and the purposes for which it is being withdrawn.

Macro-Economic Framework Statement: Provides the assessment of the government on the growth prospects of the economy for the next few years.

Medium-Term Fiscal Policy cum Fiscal Policy Strategy Statement: This document details the government’s budget deficit target for the next three years, with the targets broken down for tax and non-tax receipts. The document also explains the government’s policies and its adherence to the FRBM act. Any departure from the Act has to be explained and the remedy for the same has to be suggested. Earlier there were two separate documents: medium-term fiscal policy statement and the fiscal strategy statement.

Economic Survey - It is a document prepared by the ministry of finance which provides details of the state of economy of the ongoing year. The entire document is generally divided into two parts, where the first part presents the analytical/qualitative description of economy and country in general, second part provides the statistical data of all major sectors, as well as any other important economic data.

Output Outcome Framework for Schemes: This document is the result of the outcome budgeting practice adopted by India, and provides a tool to evaluate performance of various schemes. The document provides the output and outcome indicators for major central sector schemes and centrally sponsored schemes.

Implementation of Budget Announcements: This document is also an evaluation tool. It presents the major announcements / targets mentioned in the budget speech of the previous year, and details the extent to which those targets have been achieved.

While the above documents are stand-alone papers presented with the Union Budget, there are others that are part of some of the above documents. Because of their importance, these documents deserve a separate mention. They are:

Gender Budget Statement: Captures budgetary resources earmarked for women and girls by various Union Ministries and Departments. It comprises two parts: Part A lists schemes and programmes that allocate their entire budget for the benefit of women and girls, while Part B reports schemes meeting the minimum floor requirement of 30 per cent allocation for the benefit of women and girls. The number of Demands for Grants reported in the GBS in Part A is 25 and Part B is 33.

Statement on the Allocations for the Welfare of Children: This is one of the primary tools for child-responsive budgeting, both at the Union and State levels. Statement 12, titled ‘Allocations for the Welfare of Children’, has been brought out by the Union Government consistently since 2008.

Statement on the Allocations for the Welfare of Children: This is one of the primary tools for child-responsive budgeting, both at the Union and State levels. Statement 12, titled ‘Allocations for the Welfare of Children’, has been brought out by the Union Government consistently since 2008.

Statement on Allocation for Welfare of Scheduled Castes: Given the lagging development status of schedule castes, government makes plans/schemes which are aimed at the welfare specifically of schedule castes. This document provides the allocation for schemes which are either fully or partially aimed at welfare of scheduled caste.

Statement on Allocation for Welfare of Scheduled Tribes: Similar to ‘schedule caste’, the schedule tribes also lag in the development indicators relative to general population. To correct this, government makes specific plans/schemes for scheduled tribe. This document provides the allocation for schemes which are either fully or partially aimed at welfare of scheduled tribes.

Allocation for the North Eastern Region: The north-eastern states are economically disadvantaged region because of their geography. To compensate for this disadvantage, Union Government makes additional provisions for the north-east states. This document provides the details of such allocations.

Statement of Revenue Foregone: When government provides tax incentives, it results in loss of tax revenue that it would have otherwise collected. This statement provides estimates of such tax losses for each major tax.

The large number of documents also indicate the number of different issues the Union Budget has to focus on. It should be also mentioned that while this list provides an overall list of all main documents/statements, depending on the need, one can deep dive into one or more documents to get desired information.