The Indian political governance system is known as a ‘federal structure’. In a federal structure, power and responsibility are distributed across different layers of Government. In the case of India, the power to raise money as well as the power to spend is distributed across the Union Government, State Governments and Local Governments. These three levels of Government have the power to raise resources through various taxes and non-tax sources, and spend these resources on different sectors/issues.

India’s need for a federal structure arose due to the vastness and diversity of the country. These two factors mean that the governance requirements in terms of policies and implementation vary across regions. The federal structure provides different tiers of Government the necessary flexibility to work on areas best suited to them. However, this multi-tier governance system also results in a complex structure in terms of the division of responsibilities and power to raise resources, and leads to overlaps across different tiers.

This section aims to simplify issues related to the Indian federal structure, and with that objective in mind, it has been divided into three sub-sections:

Division of responsibilities across the three tiers of Government

How different levels of Government carry out their responsibilities

Division of resource raising powers across the three tiers of Government

2.

Division of responsibilities across the three tiers of Government

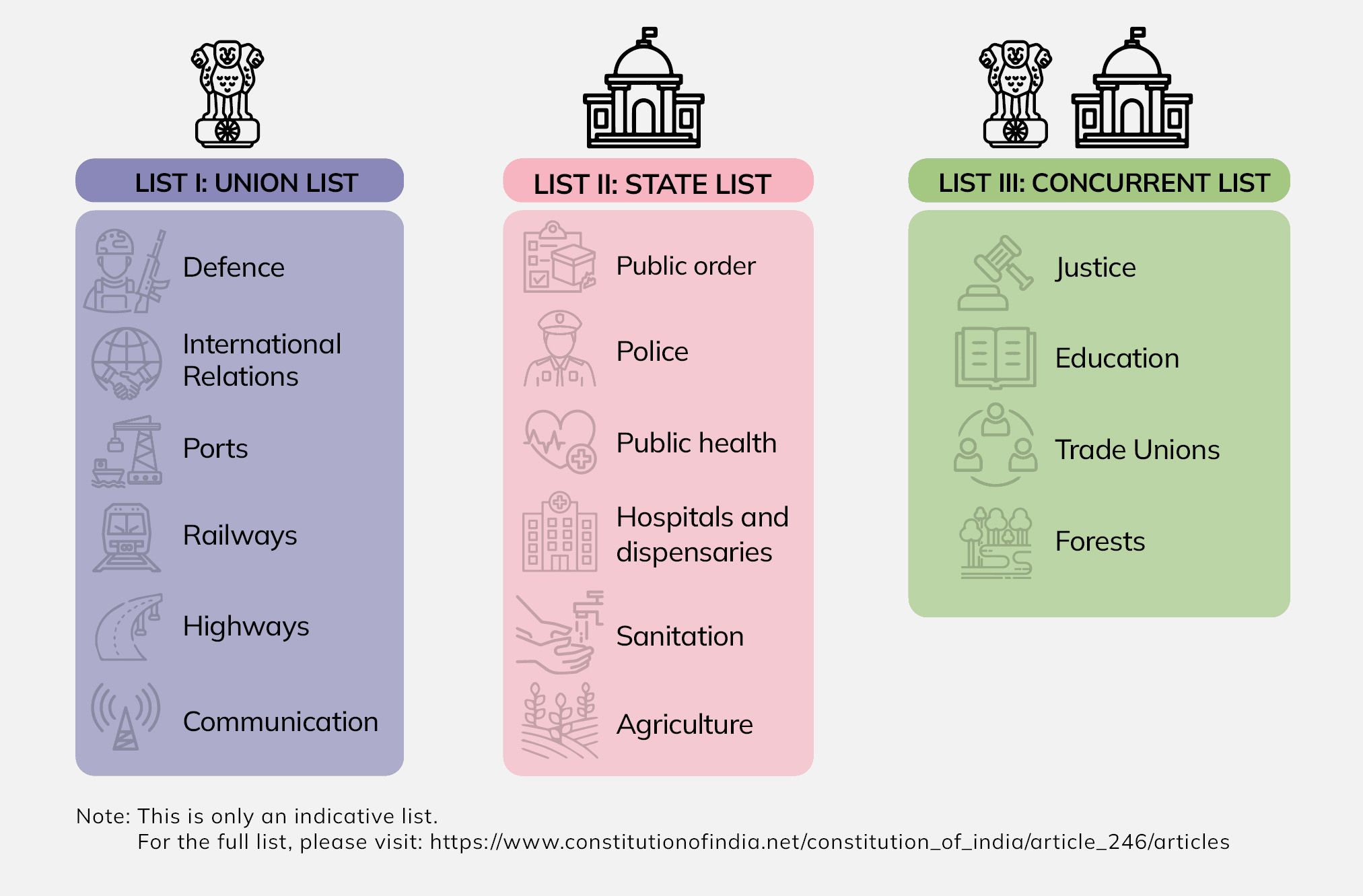

Article 246 of the Indian Constitution deals with the Seventh Schedule, which divides the responsibilities of the Union and State Governments into three lists: the Union, State, and Concurrent lists. The first two lists, as their names suggest, are about the responsibilities of the Union and States, respectively. The concurrent list mentions areas where both Union and State Governments can make laws; in case of a conflict, the law made by the Union Government prevails over the one made by the State Government. Figure 1 lists the main areas under the three lists.

Figure 1: Division of Responsibility

The main responsibilities of the three tiers of Governments are discussed in further detail below.

Union Government

Defence: The security of the country, both internal and external, is the responsibility of the Union Government of India. To this end, the Government manages the army, navy, air force, and other forces like - Central Reserve Police Force (CRPF), Central Industrial Security Force (CISF), etc.

International Relations: International relationships with other countries and multilateral organisations are the prerogative of the Union Government of India. Though State Governments can also work in this area, they generally need approval from the Centre.

Ports: These include ports for international transport as well as inland (within the country) waterways.

Railways: The Union Government has full responsibility for the country’s railway system.

National Highways: All roads in India are categorised as National highways, State highways, and others. Of these, the Union Government is responsible for national highways. These roads generally connect State capitals, bigger cities and pass through more than one State.

Airways: Aircraft, air-navigation, and all matters related to airways are under the jurisdiction of the Union Government.

Monetary Policy: Matters related to monetary economy (such as issuance and withdrawal of notes), regulation of financial institutions, etc. are the responsibility of the Union Government. To this end, it has established many institutions, including the Reserve Bank of India (RBI) and Securities and Exchange Board of India (SEBI), and delegated some of those responsibilities to these institutions.

State Governments

Public order: While public order can have a more legal and philosophical meaning, for simplicity, it can be taken to mean maintenance of peace and prevention of any actions by individuals or groups that impinge on the human rights of others. The responsibility of maintaining public order is on state governments.

Police: Police forces are the state instrument meant to maintain public order, as well as enforce law and justice.

Public health: Issues related to health, including prevention of diseases.

Hospitals and dispensaries: hubs of health services, both for cure and prevention

Sanitation: Issues related to sanitation, such as waste collection and management, water supply and so on.

Agriculture: All matters related to agriculture, including agricultural education and research, protection against pests and prevention of plant diseases.

Combined Responsibilities of Union and State Governments

Justice: Matters related to enforcement of law, including courts, except the Supreme Court.

Education: All matters related to education, including technical, medical education and universities.

Trade Unions: Issues related to labour.

Forests: Policies related to forests.

Local Bodies

In India’s three-tier governance system, the Union and State Governments are complemented by Local Governments. Local governance in India takes place in two very distinct forms, depending on whether the locality is Urban or Rural.

An Urban Local Government / Body is the layer of Government that has the responsibility of development in cities and towns. Urban Local Governments are further classified into three types:

Municipal Corporations / Nagar Nigam: For large urban areas

Municipal Councils / Municipalities / Nagar Palika: For smaller urban areas

Town Area/Notified Area Councils / Nagar Panchayats and suburban Government Bodies: For areas in transition from a rural to an urban area

The Rural Local Government / Panchayati raj system is a three-tier system with elected bodies at the village, taluka and district levels. These bodies are also known asPanchayati Raj Institutions (PRIs).

Most of the financial powers and authorities to be bestowed on local bodies are at the discretion of State legislatures. Consequently, the powers and functions vested in local bodies vary from State to State.

The Twelfth Schedule of the Constitution lists the various functions of Urban Local Bodies. Of these, some functions are obligatory in nature and some are discretionary, as given in Figure 2:

Figure 2: Responsibilities of Urban Local Bodies

There is a lot of difference in the assignment of obligatory and discretionary functions to Urban Local Bodies across the States. For instance, while functions such as planning for social and economic development, urban forestry, protection of the environment, and promotion of ecology are obligatory for the municipalities of Maharashtra, these are discretionary in Karnataka.

For Panchayati Raj Institutions, an indicative list of 29 items has been given in the Eleventh Schedule of the Constitution. Rural Local Bodies are expected to play an effective role in planning and implementation of works related to these 29 items. The notable items among these are given in Figure 3:

Figure 3: Major Responsibilities of Panchayati Raj Institutions

3.

How different levels of Government carry out their responsibilities

The previous section highlighted the responsibilities of the different tiers of Government in India. This section explains how those responsibilities are carried out.

Broadly, the Government carries out its responsibilities by implementing various development schemes, programmes, and other kinds of expenditures. All government expenditure can be divided into two broad categories – Schematic / Programmatic expenditure, and non-Schematic expenditure.

Schematic / Programmatic Expenditure

Government expenditure happening through schemes (big or small-depending on the scale of funding) or programmes is known as schematic / programmatic expenditure. For example, expenditure through Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS) is coming in this category. Depending on which level of Government is funding them, all the schemes can be divided into the following three categories: –

Central Sector Schemes

Centrally Sponsored Schemes

State Schemes

All of these programmes are discussed below in greater detail.

Central Sector Schemes

Schemes related to sectors that fall under the Union list, such as defence, highways and railways, are formulated, implemented and funded by the Centre as Central Sector Schemes. In addition, there are some other Central Sector Schemes that various Central Ministries implement directly in States and UTs. The financial resources for Central Sector Schemes are not shifted to the States. Examples of such schemes include Bharatnet, Namami Gange – National Ganga Plan, Liquid Petroleum Gas (LPG) connections for poor households, Crop Insurance Scheme, National Means cum Merit Scholarship Scheme, National Scheme for Incentive to Girl Child for Secondary Education, interest subsidy for short-term credit to farmers, metro railway projects, Pradhan Mantri Mudra Yojana, etc.

Centrally Sponsored Schemes

Given the federal structure of the country, where the Centre has more access to tax revenues and the States are more in sync with regional needs, schemes designed for the country are of two types: Central Sector Schemes, which are entirely funded by the centre, and Centrally Sponsored Schemes, where the State and the Centre share the funding. A centrally sponsored scheme comprises programmes that have a national character or a regional character.

Before the 14th Finance Commission recommendations were implemented, there were about 67 Centrally Sponsored Schemes. This then declined to 29 schemes. These schemes are framed on the sectors listed in the concurrent list. The Centre assists State Governments financially to get Centrally Sponsored Schemes implemented.

All Centrally Sponsored Schemes are divided into three categories: Core of the core schemes, Core schemes and Optional schemes.

Core of the Core Schemes

Six Centrally Sponsored Schemes are categorised as core of the core schemes, which are the most crucial schemes for the Government of India.

National Social Assistance Programme (NSAP)

Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA)

Umbrella Scheme for Development of Scheduled Castes

Umbrella Programme for Development of Scheduled Tribes

Umbrella Scheme for Development of Minorities

Umbrella Scheme for Development of Other Vulnerable Groups

Most of the flagship schemes of the Union Government are covered under this category. There are several models for funding of Centrally Sponsored Schemes.

CoreSchemes

There are 20 other Centrally Sponsored Schemes, which are listed as core schemes. The fund sharing ratios between the Centre and State Governments under these is given below:

For 8 North Eastern States and 3 Himalayan States: - Centre: State = 90:10

For other States: - Centre: State = 60:40

For Union Territories

without a Legislature: Centre 100%

with a Legislature: - Centre: UT = 60:40

OptionalSchemes:

There are two schemes under the optional scheme category:

For 8 North Eastern States and 3 Himalayan States: - Centre: State = 80:20

For other States: - Centre: State = 50:50

For Union Territories:

without a Legislature: Centre 100%

with a Legislature: Centre: UT = 80: 20

The Union Government spends nearly 12 per cent of its annual budget on Centrally Sponsored Schemes.

State Schemes

These schemes are for sectors that fall in the State list. The State is the formulator and implementer of these schemes and funds them entirely.

Some of the main areas in which State Governments spend their money are: Police and justice system, education, health, water and sanitation, labour, rural development, electricity, transport, devolution to local bodies, etc.

Non-Schematic / Programmatic Expenditure

As the name suggest, these expenditures are on the items other than schemes / programmes. Three major components of this expenditure are

Establishment / Administrative Expenditure

The Establishment Expenditure of includes all the establishment related expenditure of the various Ministries/Departments, including establishment expenditure of attached and subordinate offices. This type of expenditure heads includes: among others, salaries, medical expenses, wages, overtime allowances, foreign travel expenses, domestic travel expenses, office expenses, materials and supplies, publications, advertising and publicity, training, other administrative expenses, rent rates and taxes, royalty, pensionary charges, rewards and minor works, motor vehicles, information technology, etc.

Expenditure on Public Sector Enterprise and other Autonomous Bodies

As the name suggest, these are the expenditure incurred by the government on the enterprises in public sector, as well as autonomous bodies. Examples of autonomous bodies are – various government owned and operated research and training institutes, cultural societies, museums, etc.

Transfers and Other Expenditure

The category includes the transfers by Union Government to States excepts those recommended by the finance commission, and transfer from states to local bodies expect those recommended by finance commission. Some examples included transfers to State made under National Disaster Relief Fund, Assistance to schemes under proviso (i) to Article 275(1) of the Constitution, etc. This category also includes expenditure on items such as Interest Payments, Repayment of Debt, contribution to international organizations, etc.

4.

Resource raising powers across the three tiers of Government

Much like the division of responsibilities, the power to raise resources is also divided across the three tiers of Government. All sources of receipts can be classified into two broad categories: Tax revenue and Non-tax revenue. Tax revenue refers to money collected by the Government through payments imposed by legislation. Non-tax revenue refers to revenue raised by the Government through instruments other than taxes, such as fees / user charges, dividends and profits of Public Sector Undertakings (PSUs), interest payments, penalties and fines. The main sources of receipts under both categories are discussed below.

Tax Revenue

Given below is the list of all the major taxes that are levied currently or have been levied in the recent past:

Personal Income Tax: A tax on the income of individuals, firms, etc. other than Companies under the Income Tax Act, 1961.

Corporate Income Tax: Levied on incomes of registered companies/corporations in the territory of India (whether national or multinational/foreign). National companies are taxed on the basis of their aggregate income, irrespective of source and origin, whereas foreign companies are taxed only on the income that arises from operations carried out in India.

Union Excise Duty: A production tax imposed by the Union Government on goods manufactured in India for domestic consumption under the Central Excise Act, 1944, and the Central Excise Tariff Act. From 1999 onwards, it has been called the Central Value Added Tax (CENVAT).

State Excise Duty: Unlike Union Excise Duty or CENVAT, State Excise Duty is charged on alcohol and related products, narcotics, etc.

Service Tax: Levied on services provided by an entity / individual. The responsibility for payment of this tax lies with the service provider.

Cess: In India, cess is applied on a specific commodity or service and is imposed as an additional tax on an already existing tax. The revenue raised from such cesses is meant to meet certain specific objectives/expenditure. For instance, the Swachh Bharat cess is meant to be spent only on sanitation-related activities and not on, say, education.

Surcharge: An additional charge levied on any tax. But unlike a cess, revenue from a surcharge can be spent on any purpose.

Customs Duty: Imposed on goods imported from other countries.

Equalisation levy: Introduced in India in 2016, the aim of this levy is to bring under the tax net the digital transactions by companies who don’t have taxable presence in India but earn revenue from India. It is imposed on payments made from Indian companies to foreign digital/e-commerce companies. It is colloquially known as the Google tax.

Sales Tax: Generally charged at the point of purchase or exchange of certain taxable goods, this tax is charged as a percentage of the total value of the product. In India, Sales Tax used to be levied under the authority of both Central Legislation (Central Sales Tax) and State laws (Sales Tax) before the introduction of Value Added Tax (VAT).

Value Added Tax: A tax on transactions. Instead of taxing the value/volume of a transaction, the tax is only levied on the value added at a particular stage of production and supply. In India, VAT was levied by States from 2005.

Goods and Services Tax (GST): In 2017, India introduced a Goods and Services Tax, which replaced a number of Central and State taxes, such as – excise duty, VAT, service tax, sales tax, etc. GST is an indirect tax levied on the value added to goods and services. It replaced many indirect tax laws and introduced one indirect tax for all of India. GST is currently levied on every product except petroleum, alcohol, tobacco, and stamp duty on real estate in four slabs: 5, 12, 18, and 28 per cent. Many essential items are exempted from GST as well. To govern this new tax, a new GST council was created with representation from the Union and States Governments.

GST compensation cess: Levied in addition to regular GST on certain goods such as tobacco and related products, coal, aerated beverages, luxury cars, etc. The revenue generated from the cesses is to be used to finance compensation to States in case there is a shortfall in the revenue collected from GST.

Stamps and Registration Duty: Charged on the sale and transfer of property. It is a major source of tax revenue for most States.

Motor Vehicles Tax: A tax levied on every motor vehicle by a State under its Motor Vehicles Taxation Act. The State Government has the power to increase or decrease the rate of tax from time to time.

Property Tax: Levied by local bodies on immovable property, i.e., on land and/or buildings.

Entertainment Tax: Generally levied on movie tickets, amusement parks and other entertainment activities.

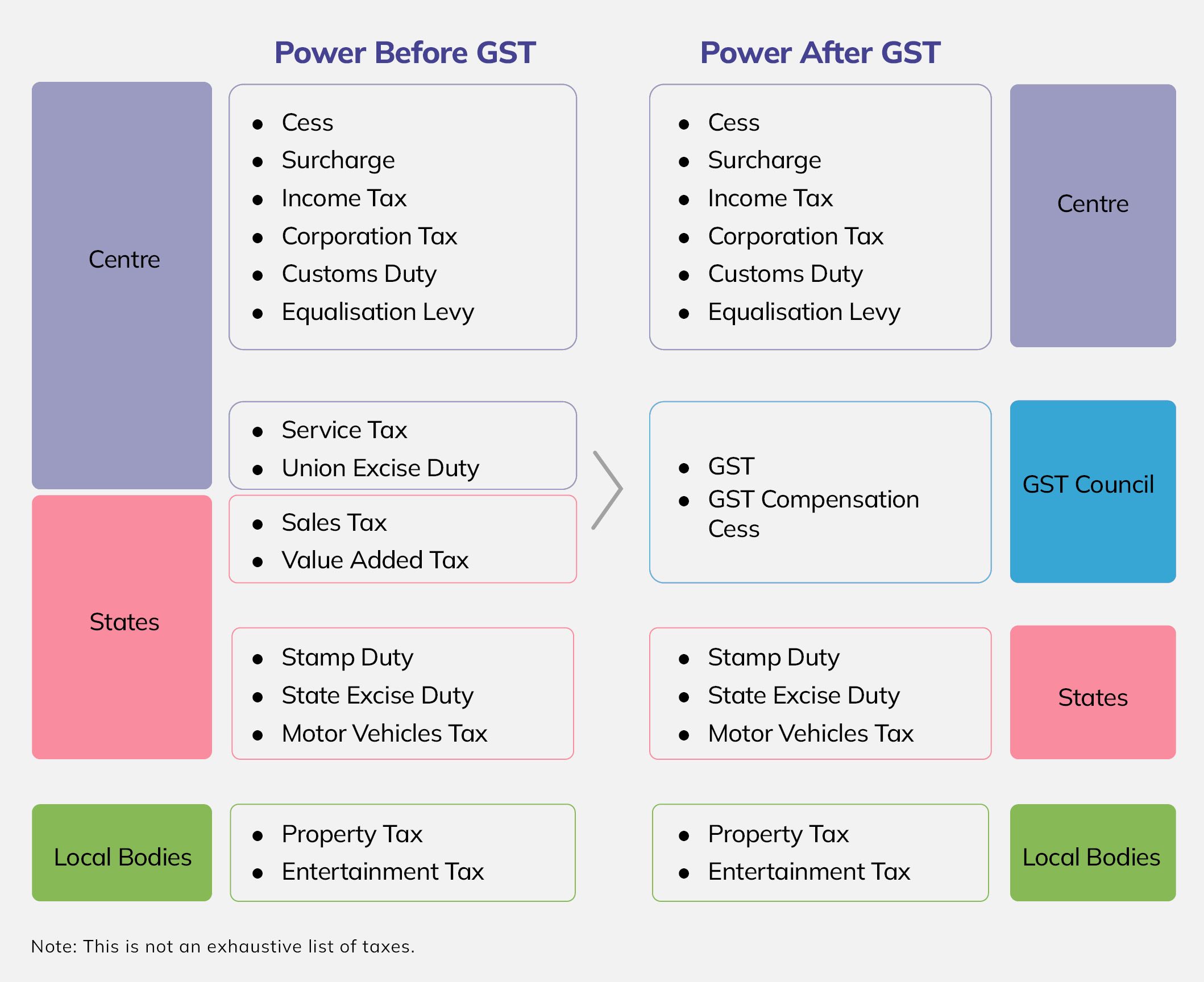

Distribution of Tax Revenue

The distribution of major taxes to different levels of Government is given in Figure 4. The table also shows the distribution pattern before and after implementation of GST.

Figure 4: Distribution of Power for Major Taxes

From the table above, it can be seen that some of the major taxes were replaced by GST. They are: Service tax, Union excise duty, Sales tax and VAT. Currently, four bodies — three Governments and the GST Council — administer the raising of tax revenues.

Sharing of Tax Revenue Across the Three Tiers of Government

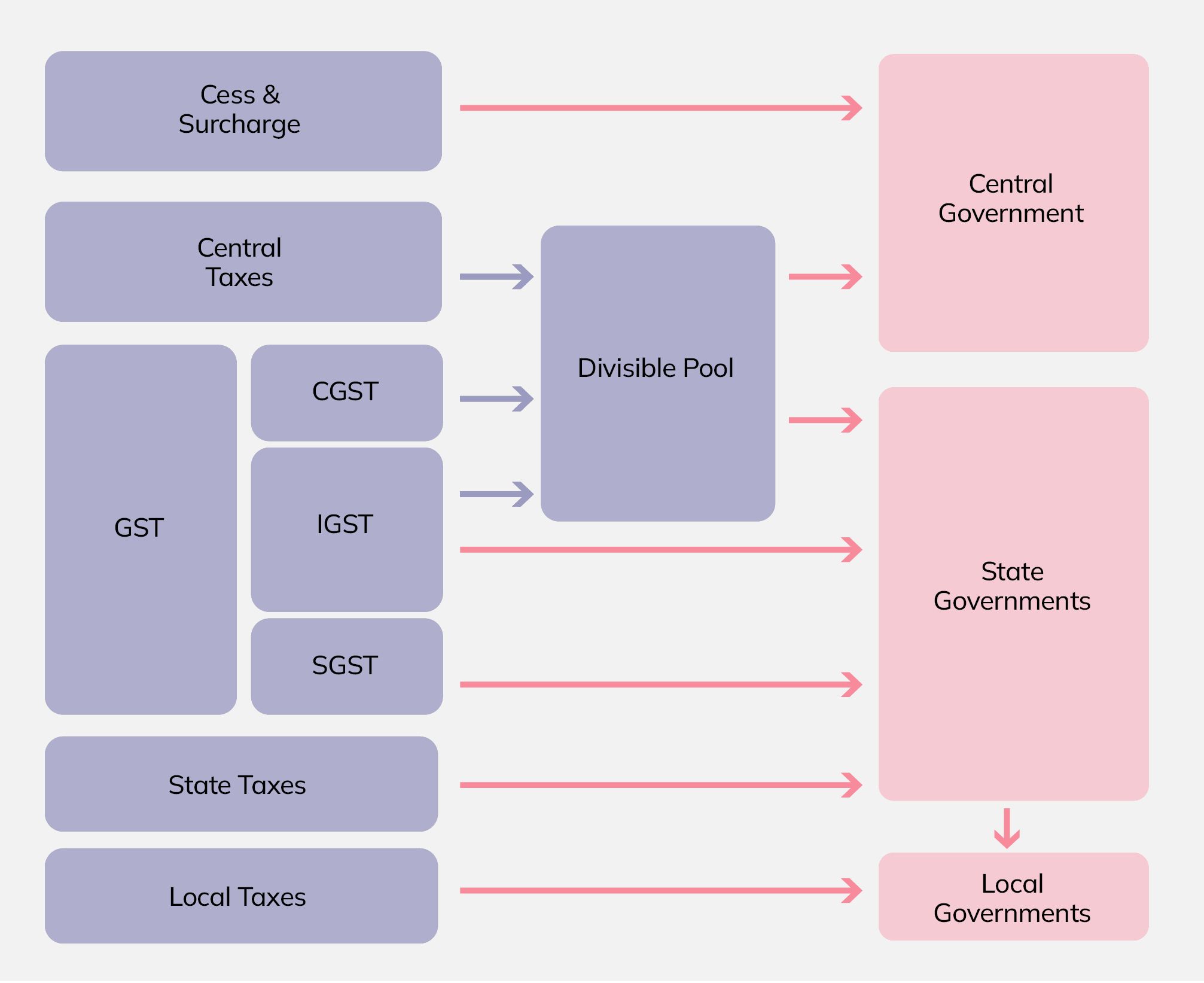

As mentioned previously, different levels of Government in India have different taxing powers. The tax revenue collected by the Centre and States is shared among the three tiers of Government. This sharing of resources is done to promote equity between States. If all the States are left to raise their own resources, then developed States are likely to raise more taxes. Once they employ those taxes in development projects, interstate inequality will only worsen. To address this, some taxes are raised by the Central Government and shared with State Governments. The sharing of tax receipts is summarised in Figure 5.

Figure 5: Sharing of Tax Revenue between Governments in India

This figure can be explained as follows:

The revenue raised through imposition of a cess or a surcharge goes directly to the Central Government

Central taxes and the part of GST known as Central Goods and Services Tax (CGST) form the divisible pool, which is shared between the Centre and States in line with the recommendations of the Finance Commission, which is constituted every five years.

Integrated Goods and Services Tax (IGST), the component of GST which is levied on the inter-state transactions, is shared equally between the Centre and States. The IGST that the Centre collects is part of the divisible pool.

The responsibility to collect revenue from taxes in the divisible pool lies with the Central Government, and it then shares the amount with the State, as recommended by the Finance Commission. Currently, in FY 2021-22, 41 per cent of the divisible pool is to go to the States, while the remaining 59 per cent goes to the Centre.

As the name indicates, the State Goods and Services Tax (SGST) component of GST goes to the States.

State taxes go to State Governments.

Local taxes go to Local Governments.

Local Governments also get a share of resources from State Governments own resources. The proportion of such a share is decided based on the recommendations of the State Finance Commission.

The Central Finance Commission

India’s Constitutional arrangements generally result in a mismatch between the ability of the three tiers of Government to raise resources and spend them. Hence, a Central Finance Commission is set up every five years or before by the President of India to suggest how financial resources should be shared between the Centre and the States. A major part of this pertains to the sharing of revenue collected through the Central Tax System. The central taxes that are devolved to States are untied funds and can be used at the discretion of the States.

The Finance Commission is constituted under Article 280 of the Constitution.Before the year 2000, only Income tax and the certain Union excise were shared. But after a constitutional amendment in 2000, all central taxes were allowed to be shared with States. The constitution has been amended twice since then — through the 80th constitutional Amendment Act (CAA) and 88th CAA in 2000 and 2003, respectively — to change the scheme of distribution of taxes between the Centre and States.

In the recommendation period of the 14th Finance Commission (from 2015-16 to 2019-20), 42 per cent of the shareable/divisible pool of Central tax revenue is to be transferred to States every year, and the Centre is to retain the remaining amount for the Union Budget. The 15th Finance Commission (from 2020-21 to 2024-25) was constituted on 27th November 2017. The Commission’s first report, consisting of recommendations for the financial year 2020-21, was tabled in Parliament on February 1, 2020. The final report, with recommendations for the period 2021-26, was submitted on 9th November, 2020. The report recommends that the share of States in Central taxes be decreased from 42 per cent during the 2015-20 period to 41 per cent. The 1 percentage point decrease is to provide for the newly formed Union territories of Jammu and Kashmir, and Ladakh, from the resources of the Central Government.

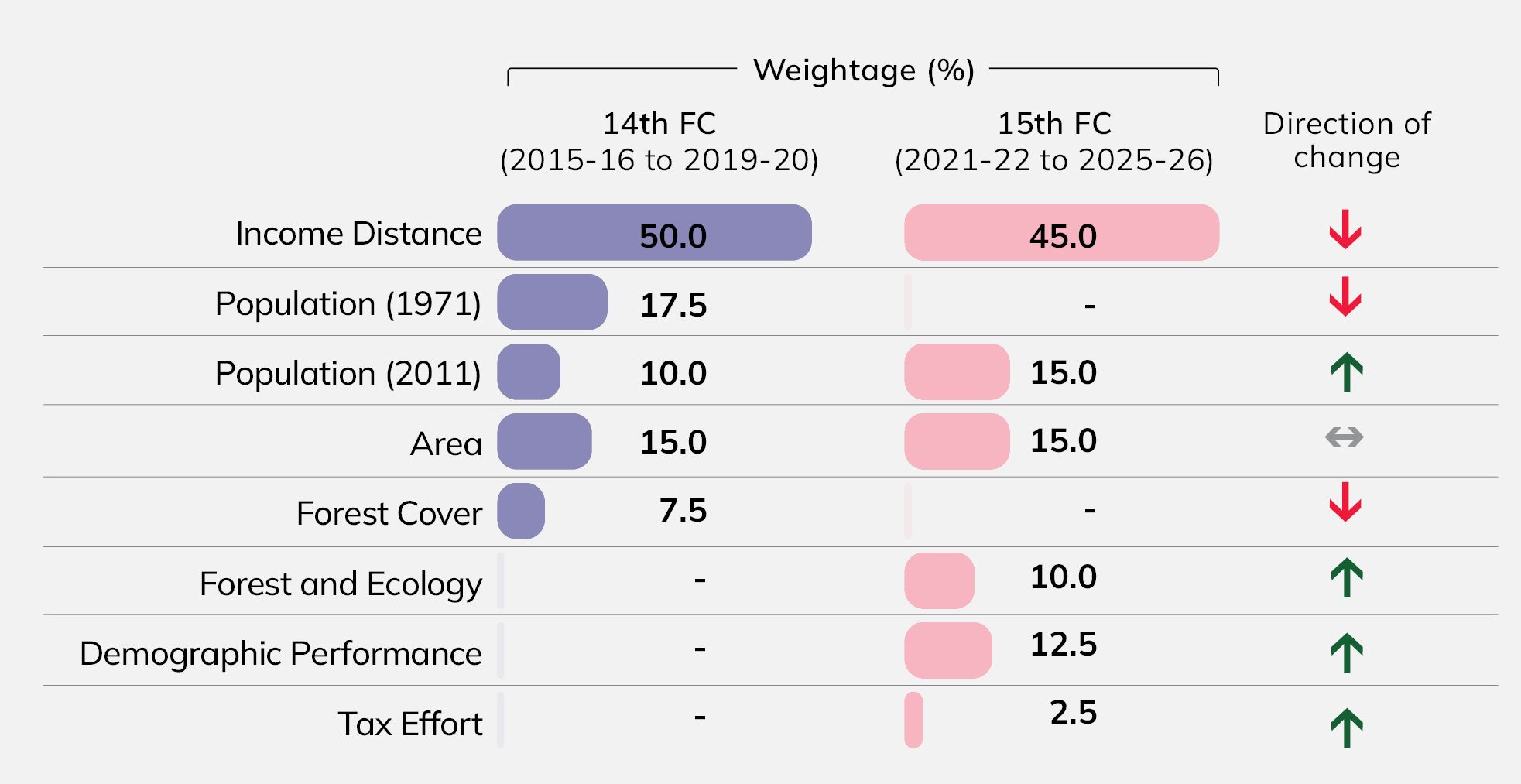

Figure 6 provides the formula used by the 14th and 15th Finance Commissions for sharing of resources among States:

Figure 6: Weightage of Different Factors – 14th FC vs 15th FC

For 2020-21, the Fifteenth Finance Commission had submitted its first report, which has the same formula as for the final report of the 15th FC for the period 2021-26.

The criteria used in the table are explained below:

Income Distance: The gap between the State with the highest per capita State Gross Domestic Product (GSDP) and any particular State. In the current calculation, the two States with the highest per capita income are Goa and Sikkim. But since these are smaller States, the next State, Haryana, has been taken as the one with highest per capita GSDP.

Population (1971): The population of States as estimated by the census conducted in 1971.

Population (2011): The population of States as estimated by the census conducted in 2011. Population data from 1971 has been used by the Sixth FC onwards, but it was argued that the current population is different, and the new terms of reference (TOR) mentioned use the latest Census population data.

Area: Geographical area of the State.

Forest Cover: Percentage of geographical area of a State that is forest.

Forest and Ecology: Slightly modified criteria from the erstwhile ‘forest cover’, as it also considers the impact of forests on a State’s resources and cost.

Demographic Performance: This is to reward States that have performed better in controlling population growth. The indicator of fertility rate is taken as the measure of demographic performance.

Tax Effort: An indicator of a State collecting its own tax revenue in relation to its GSDP. This indicator is to reward States that are performing better in terms of collecting their own tax revenue.

All these indicators are based on three principles: Need and cost, Equity, and Performance. Population, area, and forest ecology are indicators of Need and Cost. Income distance is the indicator for Equity. Demographic performance and tax effort are indicators for Performance.

The total Union Government resource transfers to States consist of those determined by the Central Finance Commission (i.e., States’ share in Central taxes and Grants) and Plan Grants (which include funds for Centrally Sponsored Schemes). Resources transferred according to the Central Finance Commission’s recommendations to the States are called ‘untied’ resources.

There are various types of non-plan grants or grants shared by the Union Government with States as per the recommendations of the Central Finance Commission, from time to time. One of them is the ‘Post-Devolution Revenue Deficit Grant’. This grant is determined by the Union Finance Commission and awarded to States as per the projected fiscal positions of States and the deficit that arises in the non-plan revenue account of a State. The grant covers the gap between the State’s revenue and expenditure. It is given to deal with the State’s burgeoning revenue deficit through a mechanism provided by the Finance Commission for compensation (from the Centre) of any loss incurred by States in their revenue account.

Another grant recommended by the Central Finance Commission is the ‘Local Bodies Grant’. This grant is determined under Article 275(1) of the Constitution and consists of grants to both urban and rural local bodies.

There are specific-purpose grants and sectoral grants. From time to time, the Central Finance Commission recommends counter balancing the burden on States to finance Centrally Sponsored Schemes. The basic purpose of these types of grants is to enable States to finance public services (mostly in social sectors) and bring parity across States.

These four components together (State’s Share in Central Tax + Revenue Deficit Grant + Local Bodies Grant + Specific Purpose Grant and Sectoral Grants) consist of the constitutionally determined transfer of resources from the Union Government to State Governments. The rest is determined by the Central Government at its discretion.

In this context, it should be noted that when allocations of funds are made across Union Ministries / Departments from the Union Budget, the State’s share of Central taxes is kept outside the purview of expenditure in the Union Budget (Consolidated Fund of India).

One notable aspect in the sharing of tax revenue between the Union and State Governments is the role of cesses and surcharges. Though both these levies are part of tax collections, they are not part of the divisible pool of resources, and are hence not shared with the States. This aspect has become much more prominent in the last few years as the share of cesses and surcharges has increased in the overall tax collection.

Grants-in-Aid

Grants-in-Aid are provided from a higher tier of Government to a lower tier. In this case, it is provided by the Union Government to the States and Local Bodies. It is different from loans since these are provided without the expectation of any repayment. Apart from distribution of taxes between the Centre and States, the Constitution provides for two types of Grants-in-aid, viz. Statutory grants and Discretionary grants:

Statutory Grants:Article 275 makes provisions for statutory grants to States which are in need of financial assistance. These are charged to the Consolidated Fund of India. Such grants include specific grants to promote the welfare of Scheduled Tribes in a State or to raise the level of administration of the Scheduled Areas in a State, including the State of Assam. The bases of these grants are recommendations by the Central Finance Commission.

Discretionary Grants: Under article 282, both the Centre and States are able to make grants for public purposes even if these are not within their legislative competence. Since such grants are discretionary, there are no obligations to make them. During the Planning Commission era, Discretionary grants were bigger than Statutory grants, which made the role of Planning Commission very important.

Non- Tax Revenue

Non-tax revenue refers to the receipts earned by the Government from sources other than taxes. Non-tax revenue is usually charged against services provided by the Government.Given below is the list of major non-tax revenue sources of the Union, State and Local Governments: -

Sources of Non-Tax Revenue for the Union Government

The following are the main sources of non-tax revenue for the Union Government:

Interest Receipt: This is received on loans given to States and Union Territories for reasons such as non-plan schemes (e.g. flood control) and planned schemes with a maturity period of 20 years (e.g. modernisation of police forces). In addition, the government earns interest on loans advanced to Public Sector Enterprises (PSEs), Port Trusts and other statutory bodies.

Dividends and Profits: These are earned from PSEs and from the transfer of surpluses by the central bank.

Petroleum License: These are fees to get the exclusive right for oil and gas exploration in a particular region. Such fees may be in the form of a royalty, a share of the profit earned from contract areas during a specific period, a Petroleum Exploration License (PEL) fee or Production Level Payment (PLP).

Power Supply Fees: This includes fees received by the Central Electricity Authority for the supply of power.

Fees for Communication Services: This mainly includes license fees from telecom operators on account of spectrum usage charges that licensed Telecom Service Providers pay the government

Broadcasting Fees: These include the license fee paid by direct to home (DTH) operators, commercial TV services, commercial FM radio services etc.

Road, Bridge usage fees: This includes receipts through toll plazas on account of the usage of national highways, permanent bridges etc.

Sale of stationery, gazettes etc: This comes under ‘Stationery and Printing’ and relates to the sale of stationery, gazettes, government publications, etc.

Fee for Administrative Services: This includes fees received for providing audit services, issuance of passport, visa and other services.

Currency, Coinage and Mint: This category covers the receipts of the Currency Note Press; Security Paper Mill; Bank Note Press and of the Mints as well as the profit from circulation of small coins.

Other non-tax receipts: This category covers revenue from various Government activities and services such as administrative services, public service commission, police, jails, agriculture and allied services, industry and minerals, water and power development services, transport and communications, supplies and disposal, public works, education, housing, information and publicity, broadcasting, grants-in-aid and contributions.

Sources of Non-Tax Revenue for State Governments

The following are the main sources of non-tax revenue for State Governments:

Interest Receipt: Like the Union Government, State Governments, too, provide loans to Local Governments or other public sector enterprises. These receipts refer to the interest earned on those loans.

Licensing fee for mineral exploration: States also earn revenue when they lease out the exploitation of mineral resources.

Fee levied in relation to forestry: These are the fees levied on usage of forestry.

Other Non-tax revenue: These generally refer to the revenue earned when States provide economic services, such as irrigation, health, education, transport, lotteries, etc.

Sources of Non-Tax Revenue for Local Bodies

The following are the main sources of non-tax revenue for Local Governments:

Grants: Amounts local bodies receive from State Governments. There is no specific system of grants-in-aid; the grants are given either to incentivise tax efforts or to match the effort in maintenance of services.

License fee: Earned by issuing trade licenses to private markets, cinema houses, slaughterhouses, burial grounds, commercial animal stalls etc.

Gate Fees: Entry fees obtained from the highest bidder, who, in turn, regulates entry based on certain fees. Major sources of gate fees are public markets, public parking and halting places, public slaughterhouses etc.

Income from Property (Rent): Rent from buildings, lands, cloakrooms, comfort stations etc.

Income from property other than rent: Proceeds from sale of rights to collect river sand, sale of rights to fish, sale of usufructs etc.

Permit fees: These are of two kinds: fee for building permits and fee for permits for the construction, establishment or installation of factories, workshops or workplaces where electricity is used.

Registration fees: Registration of hospitals and paramedical institutions, tutorials, births and deaths, contractors (only in Urban Local Governments), etc.

Service Charges: Charges collected for use of utilities and amenities provided by Local Governments. User charges are more a potential area of finance than a reality now. Charges are levied on the direct recipient of a service.