Government budget processes are complex, and though a budget is drawn up for one year, known as financial year, the budgetary process itself generally runs over more than one financial year and involves many stages. This section provides details on the four major stages of the budgetary process.

As India is a federal country, and has a three-tier governance structure, Governments at the Union, State, and local level each have their own budgetary processes. All three, though, follow the same financial year, which runs from April to March.

Keeping in mind the multi-stage budgetary process, and the three-tier governance structure, this chapter has been divided into four sections:

A budget generally contains details of where money comes from and where it goes. A Government budget, however, is a far more complex and detailed document. It reveals what policies the Government has formulated for the country, how the Government plans to tackle various socio-economic challenges, what outcomes it hopes to achieve by the end of the fiscal year, and many other things. Given that the budget has to serve myriad objectives; the entire budgetary process is a lengthy affair. Broadly, a Government’s budget-related processes can be divided into four distinct stages:

Formulation or preparation

Enactment or legislative approval

Implementation or execution

Audit or review

All four stages are discussed in detail in this section.

Formulation

The first stage of the budgetary process takes place completely with the executive branch of Government, and can include numerous actors within the branch. At this stage the parameters of the budget are set and decisions are taken about how the revenue generated will be distributed across programmes and activities. The outcome of this process is the proposed budget, which is essentially the action plan of the Government for the coming fiscal year, as well as a statement of the Government’s priorities and commitments.

The formulation of the annual budget generally happens behind closed doors, but occasionally, the Government engages in consultations with different stakeholders such as subject matter experts, businesses, trade groups, labour Unions, civil society organisations, etc.

Enactment

This step refers to the presentation of the budget in Parliament/the State Assembly by the finance minister.

The budget presentation highlights the priorities of the Government, as well as its policy choices. Approval by the legislature is required for two different items:

The Finance Bill

The Appropriation Bill

The Finance Bill provides the Government legal authority to raise resources, mainly through taxation. The Appropriation Bill, on the other hand, provides the Government legal authority to incur expenditure as stated in the budget and approved by the legislatures. According to the Constitution, no expenditure can be incurred from the ‘Consolidated Fund of India’ without authorisation of legislature and passing of the Appropriation Bill.

Implementation

The stage refers to the Government implementing the budget proposals, i.e., raising resources as envisioned in the budget, as well as incurring expenditure according to the budget.

The receipts in the budget are estimates, and actual collections are often different from the estimates. In such cases, one part of implementation also requires balancing receipts and expenditure throughout the year to meet the deficit targets mentioned in the budget.

On the expenditure side of the budget, the key issues are whether the expenditure is likely to be within the budget figure, whether changes in expenditure priorities (as against past patterns) are being implemented in specific areas as planned, and whether problems are being encountered in budget execution, such as the build-up of payment arrears.

Audit

Public financial management and good practices of budgetary control require that a body that is independent from the executive evaluate the Government’s budget execution and issue an annual audit report. The institution vested with this responsibility is often referred to as the supreme audit institution (SAI) or the office of the Auditor and Comptroller General of India. The basic purpose behind the audit is to make sure the Government is following the rules and regulations governing the overall processes related to raising money and expenditure. These reports help in holding the Government accountable and also help in improving budgetary processes.

The Union budget of India is presented in Parliament on the 1st of February every year, but this presentation is preceded and succeeded by elaborate processes through which the budget is formulated, implemented and audited. This section lays out the processes, institutions and actors involved in each of these stages, and details when each stage occurs.

Formulation

The process of budget formulation starts in the last week of August or the first half of September every year. To get the process started, the Budget Division in the Department of Economic Affairs, under the Ministry of Finance, issues the annual ‘Budget Circular’ to all Union Government ministries/departments /agencies / institutions around August / September. The Budget Circular contains detailed instructions / guidelines for these ministries/departments / agencies on the form and content of the statement of budget estimates to be prepared by them.

The Expenditure Department of the Finance Ministry calls for projected expenditure in October, under the following heads

Actual expenditure of the previous financial year

Original budget estimates for the current financial year

Revised estimates for the current financial year

Budget estimates for the next financial year.

This is followed by a series of bilateral discussions between the Ministry of Finance and major stakeholders (Expenditure Ministries / Departments) such as the Ministry of Health Ministry of Education, Ministry of Rural Development and Panchayati Raj and so on.

In November / December, the Finance Minister starts a series of consultations with sectoral representatives such as economists, farmers, small-scale industries, exporters, industrialists, trade unions, social sector experts and so on. The objective of this exercise is to get their inputs as well as a sense of their expectations on the expenditure side and on the tax issues.

The first part of the budget to be finalised is the expenditure budget, and this generally happens in January every year.

Sometime in January, the Finance Minister asks for the first “blue sheet” from the Budget Division. The blue sheet is essentially a single sheet of paper with the broad numbers: how much expenditure is needed; how much revenue is expected; what the deficit will look like. This is only the first of many blue sheets. Each blue sheet is discussed by the Budget group and destroyed the day the discussion on it ends. No record of these sheets is maintained.

The Budget group has a core team of five members: the Finance Minister, Finance Secretary, Revenue Secretary, Expenditure Secretary and the Chief Economic Advisor. Aiding them are the Additional Secretary – Budget and the Chairpersons of the two tax boards, the Central Board of Direct Taxes and Central Board of Indirect Taxes and Customs. This group discusses the tax changes that can be made.

After the Finance Minister has decided on the broad numbers, he/she goes to the Prime Minister for a first round of consultations. The Prime Minister may suggest some broad changes, which are incorporated before a second and more detailed round, where the new schemes are carefully considered. A third round of discussions is held on the tax proposals followed by a final round, if required, on the actual speech. All these discussions carried out in the first half of January every year.

India’s Union budget is formulated under extraordinary secrecy so that the building of Finance Ministry in which the budget preparation takes place is put under extra security. A pass is required to enter the building and every entry and exit is recorded. Once the budget documents start getting printed, only the core budget group can leave the building. The secrecy also applies to all budget documents and no one outside those working on budget have any access to information on the budget documents and numbers therein.

Enactment of the Budget

The Central Government can raise revenue and incur expenditure only upon the approval of the Appropriation Bill and the Finance Bill by the Lok Sabha (Lower House of the Parliament) and subsequently by the Rajya Sabha (Upper House of the Parliament).

Presentation of Budget in Parliament

The Presentation of Budget starts with the budget speech of the Finance Minister. The Budget speech is classified into two parts. Part A gives an overview of the economy over the previous and the current financial year. It also presents budget estimates of different expenditure items for the upcoming financial year. Part B presents tax proposals for the upcoming financial year. At the end of the Finance Minister’s speech in the Lok Sabha, the Budget documents are made available (both online and hardcopy) for the Member of Parliament and uploaded on the designated web portal of the Finance Ministry. In the Rajya Sabha, a junior minister in the Ministry of Finance lays down the budget documents.

General Discussion

After the budget is presented, a general discussion is held in both the Lok Sabha and the Rajya Sabha. At this stage the discussion is limited to a general examination of the budget and the proposals of the Government. The details of the budget, i.e., the proper distribution of the resources, the policy of taxation, as well as the volume of surplus or deficit, are not discussed at this stage. This general discussion is confined to fiscal policy issues, including a review and criticism of administration by the Government and its departments. The members of the Parliament, thus, have the opportunity of placing the grievances of taxpayers before the House. At the end of the discussion, the Finance Minister gives a response to the House. No voting on demands takes place at this stage.

Reports of the Department Related Standing Committees

As of now there are 24 Department Related Standing Committees that together oversee the work of all the ministries / departments of Government of India. One of the functions of Standing Committees is to scrutinise the allocation of funds to the ministries / departments under their supervision. These Committees examine the: (i) amount allocated to various programmes and schemes under the ministry, and (ii) trends of utilisation of the money allocated to the ministry. Officials of the ministry are required to depose before the Committees to respond to queries and provide additional information in connection with the Demands for Grants that are being examined. While examining a ministry’s expenditure, the Committees may consult or invite views from individual experts and organisations.

Based on these consultations, the Committees submit their reports to Parliament. The Committees’ recommendations are useful for Member of Parliaments (MPs) to understand the implications of the proposed expenditure across ministries and enable an informed debate before approving such expenditure.

Detailed Discussion on Demands for Grants

Typically, the Lok Sabha decides to hold a detailed discussion on four or five Demands for Grants. The ministries identified for discussion vary every year and are decided by the Business Advisory Committee of the Lok Sabha. This discussion on these Demands is followed by voting. Demands that have not been discussed and voted on by the last day are ‘guillotined’, i.e., they are voted upon together. In 2004-05, 2013-14 and 2018-19, all Demands for Grants were guillotined i.e., passed without discussion. During the voting on Demands for Grants, MPs can express their disapproval through ‘cut motions’. If a cut motion is passed, it signifies loss of confidence in the Government and the Cabinet is expected to resign. MPs can move cut motions to reduce the grant amount for the respective ministry: (i) to Rs. 1 to signify disapproval of the policies of that ministry; (ii) by a specific amount (an ‘Economy’ cut); or (iii) by a token amount of Rs. 100 to express a specific grievance.

Passing of the Appropriation Bill (Money Bill)

After the Demands for Grants are passed, they are consolidated into an Appropriation Bill. This Bill seeks to authorise the Government to spend money from the Consolidated Fund of India. This Fund consists of all the receipts and borrowings of the Government, the amount voted by Parliament, and the amount required to meet the expenditure charged on the Consolidated Fund, i.e., the amount does not require voting from the Parliament to carry out expenditure.

Expenditure items which do not require voting are as follows:

The salary and allowances of the President, and other expenditure relating to his/her offices.

The salary and allowances of the Chairperson of the Rajya Sabha and the Speaker and Deputy Speaker of the Lok Sabha.

The debt charges of the Government of India.

Salaries and pensions of the Judges of the Supreme Court.

Salary, allowances and pension of the Comptroller and Auditor General of India.

Any sum required to satisfy any Judgement or award of any court/arbitral tribunal.

Any other expenditure declared by the Constitution or by Parliament by law to be charged.

It thus, gives legal effect to the demands that have been voted on by the House. Here, it also becomes clear as to how Parliament controls public expenditure.

Passing of the Finance Bill

The Finance Bill is introduced with the budget and consists of the Government's financial proposals for the upcoming financial year. The Finance Bill is usually introduced as a Money Bill. The Constitution defines a Money Bill as one that only contains provisions related to taxation, borrowings by the Government, or funds of the Consolidated Fund of India. A Money Bill only needs the approval of the Lok Sabha, after which the Rajya Sabha can only give its recommendations.

It should be noted that the Appropriation Act only authorises the Government to appropriate money from the Consolidated Fund, whereas the Finance Bill enables the Government to collect the money it requires. As the Constitution states that “no tax shall be levied and collected except by authority of law”, a Finance Bill is placed before the Lower House of the Parliament. The Bill, when passed, becomes an Act, which authorises the Government to collect the required money through taxation or provisions that have been made in the budget. This Bill embodies the proposals of the Government to levy new taxes. It also embodies the modifications made to the existing tax structure or signals the continuance of the existing tax structure beyond the period approved by the Parliament.

The budget is said to be passed when the Appropriation Bill and Finance Bill are passed. After the budget has been passed by the Lok Sabha, it goes to the Rajya Sabha. The Rajya Sabha does not enjoy the power of amending or rejecting the budget. The Rajya Sabha can only make recommendations to the Lok Sabha, but within a period of 14 days. The Lok Sabha may either accept the recommendations of the Rajya Sabha or reject them. When the budget has been passed by both the Houses, it goes to the President for assent, after which it is considered final and published in the Gazette of India.

Implementation of the Budget

The responsibility to execute the budget lies with the Government. The execution of the budget has three aspects: (a) Distribution of the grants to different administrative ministries and departments, (b) Collection of revenue, and (c) Proper custody of the collected funds.

Distribution of the Grants

The Ministry of Finance distributes the sanctioned funds to various controlling officers under its purview. The duty of a controlling officer is two-fold:

To see that work is done in accordance with the approved budget.

To see that different ministries and departments do not incur expenditure beyond their sanctioned limit.

Thus, there is control over all public expenditure from both sides: from the administrative/distribution side as well as from the payment end.

Collection of Revenue

There are two kinds of operations involved here:

assessment of revenue

collection of revenue

The Central Board of Direct Taxes, the Central Board of Indirect Taxes and Customs, and the GST administrative body (GST Council) carry out the functions of assessment and supervision of collection and adjudication of revenue disputes. Thus, the administrative responsibility for the assessment and collection of revenue lies with these boards.

Proper custody of the collected funds

The legislature’s authority is not limited to only sanctioning appropriations. Rather, it has the means to ensure that the appropriations are applied towards the purposes approved and are within the limits allowed. In India, Parliament exercises control over public expenditure through the following institutions:

Direct control by Parliament or the Legislature

Control by Parliamentary or Legislative Committees

The Estimates Committee

The Public Accounts Committee

The Committee on Public Undertakings

The Audit Department under the control of the Comptroller and Auditor General (CAG) of India

Each of these committees (noted in point no. 2 above) is formed on the basis of proportional representation and they represent both the houses of the Parliament.

The Estimates Committee

The Estimates Committee is a Parliamentary Committee comprising of 30 members elected every year by the Lok Sabha from amongst its Members to examine the budget estimates of the Union Government. Earlier, this Committee carried out the task of examining proposed estimates of expenditure by various ministries / departments. Since 1993, the Departmentally Related Standing Committees have taken over this function, leaving the Estimates Committee to largely examine the working of certain Government organisations. Among others, main tasks of the Estimates Committee include:

to report what economies, improvements in organisation, efficiency or administrative reforms may be effected that are consistent with the policy underlying the estimates;

to suggest alternative policies in order to bring about efficiency and economy in administration;

to examine whether the money is well laid out within the limits of the policy implied in the estimates; and

to suggest the form in which the estimates shall be presented to Parliament.

The Committee may continue to examine the estimates from time to time throughout the financial year and report to the House as its examination proceeds. It is not binding on the Committee to examine the entire estimates of any one financial year. The Demands for Grants may be finally voted on regardless of whether the Committee has made a report.

Public Accounts Committee

The Public Accounts Committee (PAC) has 22 members, 15 elected from the Lok Sabha and 7 from the Rajya Sabha. It is one of the parliamentary committees that examines the annual audit reports of the CAG, which the President lays before the Parliament of India. The three kinds of reports submitted by CAG are:

Audit report on appropriation accounts

Audit report on finance accounts

Audit report on public undertakings

The Public Accounts Committee examines public expenditure. That public expenditure is not only examined from a legal and formal point of view to look for technical irregularities but also from the point of view of the economy, prudence, wisdom, and propriety. The purpose of this exercise is to bring out cases of waste, loss, corruption, extravagance, inefficiency and unnecessary expenses.

Committee on Public Undertakings (CoPU)

The committee on Public Undertakings is one of the Parliamentary Committees (Standing Committee) in the Indian Constitution that was introduced to expand parliamentary control over PSUs. This committee has 22 members — 15 from the Lok Sabha and 7 elected from the Rajya Sabha. It examines the accounts of Public Sector Units (PSUs) to check the credibility, efficiency and autonomy of their business. It examines the reports of the CAG on PSUs and performs any other tasks assigned by the Lok Sabha speaker with regard to PSUs.

Audit

Despite the fact that the audit phase is the last stage, it is a very crucial part of the entire budget cycle. Although in India it is an ex-post scrutiny, it has huge political implications. The CAG of India, which is the supreme audit institution of India, not only audits the government’s expenditure but also its revenue. It checks, for instance, whether the correct procedures and rules were followed while collecting taxes. But beyond this, it may also analyse the revenue implications of certain Government policies.

In this final stage of the budget cycle, the Controller General of Accounts (CGA), who administers matters pertaining to the departmentalisation of accounts of the Union Government, is entrusted with the following functions:

Prescribing the form of accounts relating to the Union and State Governments

Laying down accounting procedures;

Overseeing the maintenance of adequate standards of accounting by the Central Accounts Offices;

Consolidation of the monthly and annual accounts of the Government of India;

Administering rules under Article 283 of the Constitution relating to the custody of the Consolidated Fund, the Contingency Fund and the Public Account of India.

The CGA prepares a condensed form of the Appropriation Accounts and Finance Accounts of the Union Government. However, the process does not end with just the preparation of accounts by the CGA. Verification of the accounts for accuracy and completeness and to ensure that the expenditure incurred has been sanctioned by Parliament is also critical. Hence, the accounts prepared by the CGA are audited by the CAG of India. The audited accounts are tabled in both the houses of Parliament along with the CAG report. The CAG is responsible for the audit of all the expenditure of the Central and State Governments and for the submission of audit reports to the President or the Governor for placement before the appropriate legislature. The report of the CAG amounts to the issuance of a certificate. The observations of the CAG summarise the objections and irregularities in relation to voted and charged expenditure in the budget.

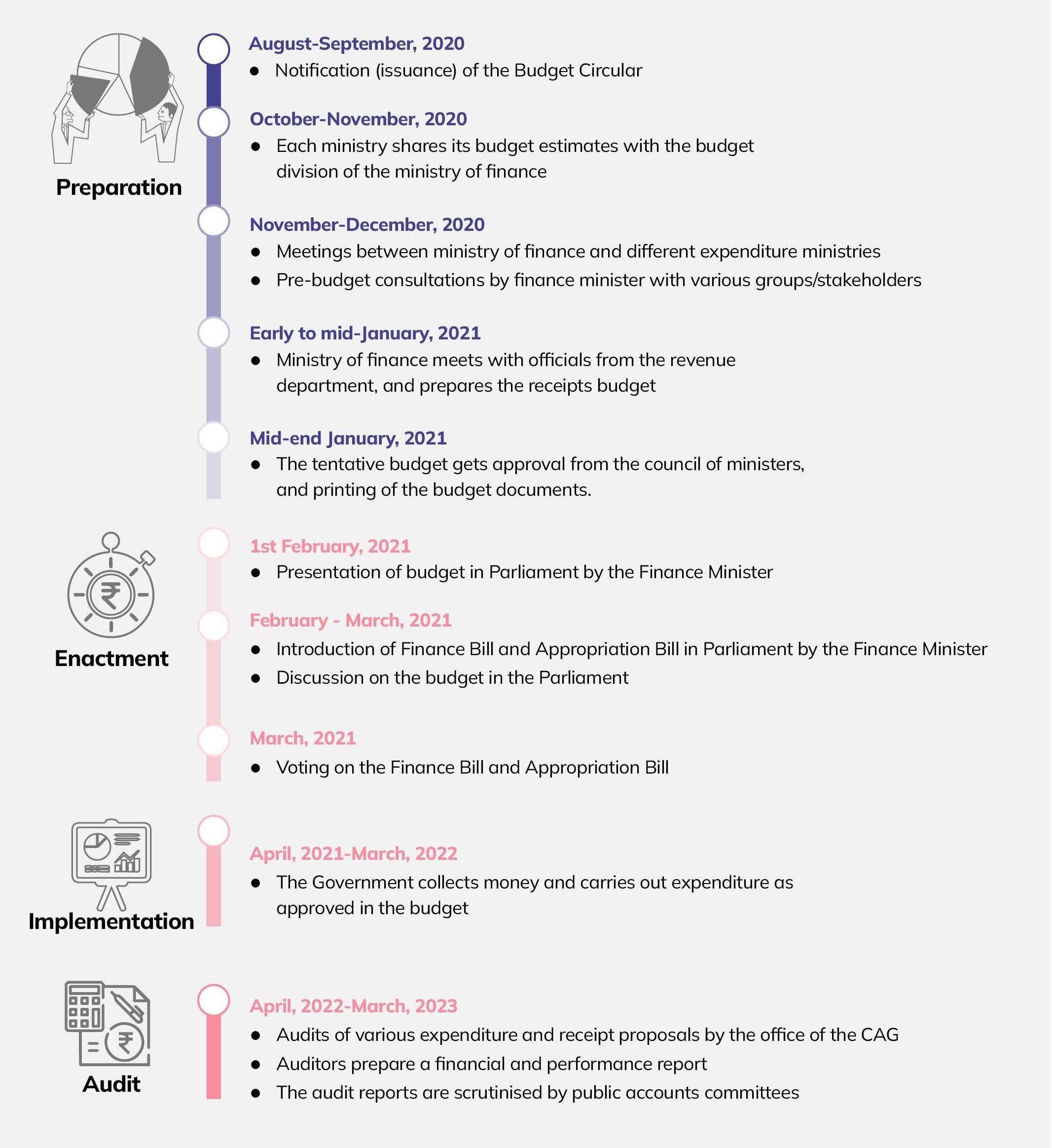

Timeline of The Union Budget

The formulation, enactment, implementation and audit of three different annual budgets take place simultaneously, whether it is for the Union or State Governments. Figure 1 captures the various processes involved in an annual Union budget. While it shows the processes of the 2021-22 budget, in parallel, the implementation of budget 2020-21 is ongoing and the audit of budget 2019-20 is being undertaken.

Figure 1: Different stages of Union Budget 2021-22

The State budget, also known as an Annual Financial Statement, is a statement of the receipts and expenditure that are estimated to be incurred by a State during a financial year. It lists the sources of receipts and projections of expenditure for the year. The structure of State Government Accounts is quite similar to that of the Union Government. For the States, too, the Constitution of India stipulates that no expenditure can be incurred from the Consolidated Fund of a State without the authority of an Appropriation Act. In order to obtain this authorisation from the State Legislature, a Statement of anticipated receipts and expenditure for each financial year, known as the budget, needs to be laid before the State Legislature.

The budget at the State level is prepared by involving various departments, as a State has several departments, each of which overlooks a particular area / sector / constituency of population, such as education, agriculture, health, children etc. The budget is then finalised by the Finance Department and approved by the Legislative Assembly.

It should be noted that State Governments enjoy autonomy in their budgets, and hence all States do not follow the same processes. There can be small differences across States, but overall, the following steps are followed by almost all of them:

Formulation

At this stage, receipt and expenditure estimates are prepared by the departments concerned for final compilation by the Finance Department. For easy comprehension, this process has been divided into two steps, namely: estimation and planning, and budget finalisation.

Step 1: Estimation and Planning / Issuance of budget circular

To begin with, the Finance Department assesses the available financial resources, which include the assistance received under ongoing schemes, expenditure incurred on their implementation, funds of public enterprises and local bodies, outstanding arrears, and so on. Then, in September, the Finance Department issues a budget circular to all administrative departments and agencies of the State government. It contains instructions regarding the preparation of the revised estimates (RE) for the on-going financial year and the budget estimates (BE) for the following year. The circular also consists of information regarding any change in the budgetary process, such as changes in classification, changes in procedure, etc., and the budget calendar, consisting of deadlines for various tasks to be undertaken to prepare the budget.

Determination of budget estimates

After the issuance of the circular, the budget estimates are prepared by various departments. The budget is made up of receipt and expenditure estimates. These estimates are prepared in accordance with the respective State’s Fiscal Responsibility and Budget Management Act

Preparation of resource estimates

The preparation of resource (receipt) estimates (both on Capital and Revenue Accounts) is based on the revenue expected to be received in the following year. This practice is undertaken by estimating officers. While making such an estimation, attention has to be paid to the likely revenue that will be generated, outstanding arrears, and the impact on revenue generation due to economic or policy related factors, etc.

Preparation of expenditure estimates

Expenditure estimates (both on Capital and Revenue Accounts) are prepared on the basis of the financial requirements of various departments. All the expenditure estimates put together reflect the State Government’s total demand to the Legislative Assembly for approval of funds. Estimating expenditure is an important exercise enabling the Government to forecast its expenditure in the following year. Like the process of resource estimates, expenditure estimates are also prepared by Estimating Officers, which contain revised estimates (RE) for the ongoing financial year and budget estimates (BE) for the following financial year. Until financial year 2016-17, expenditure estimates were divided into Plan and Non-Plan expenditure. However, since 2017-18 this distinction of Plan and Non-Plan expenditure has been dropped. Now, the budget estimates for schemes by every department have to be prepared according to the ceiling imposed by the Planning Department.

Step 2: Budget Finalisation

The budget estimates are passed on from the Estimating Officers to the heads of Administrative Departments and finally to the Finance Department. The Finance Department is responsible for the scrutiny of these estimates to check if the budget heads are correct, etc. Other than scrutiny, the Finance Department has the power to make changes such as reducing a budget estimate if the department feels that such an amount will not be spent, correcting the classification of expenditure under heads, etc. The Budget Finalisation Committees (BFCs) formed by various departments then undertake discussions with the Finance Department based on which the budget is finalised. The Finance Department has a separate division for each department. All of these estimates once finalised are compiled by the Finance Department and cannot usually be modified. This compilation will form the State’s total budget. This is then forwarded to the Planning Department for re-examination and suggestions after which it is sent back to the Finance Department. The estimates are modified if the Finance Department finds there is a need to do so.

Before finalising the budget, the Finance Department can also hold pre-budget consultations. These consultations are held with academicians, NGOs, labour organisations, farmer organisations, and social sector groups etc. to gather feedback for the upcoming year’s budget. Other than this, the Finance Department invites online suggestions from public and institutions/ organisations having expertise on public finance and budgeting. The final estimates are then sent to the Cabinet in the form of a memorandum. After approval by the Cabinet the final budget estimates are presented to the Legislative Assembly.

Enactment

After finalisation by the Finance department, the State budget is presented to the Legislative Assembly (Vidhaan Sabha) by the State’s Finance Minister in February/March every year. After the budget is presented, the Speaker of the Legislative Assembly selects a day or a period of days to hold discussions on the budget and the budget documents. Once these discussions come to an end, a vote on Demands for Grants is held. At the end of this entire process, an Appropriation Bill is introduced and voted on. This Bill is meant to sanction funds from the State’s Consolidated Fund for use by the Government in accordance with the budget. This Bill, once approved by the Legislature Assembly is sent for ascent from the Governor. A notification is then published in the Official Gazette. After the grants are passed, the Finance Department communicates the allotments authorised to all the spending departments / agencies / institutions to carry out the spending.

Implementation

Once the Appropriation Bill receives ascent from the Governor, the sanction of funds is communicated to various administrative departments. Funds are then disbursed for the execution of government schemes and programmes. This is followed by monitoring of the utilisation of funds and the implementation of the schemes and programmes.

Disbursal of Funds / Grants

The Finance Department stores the details of the allocations sanctioned for every department in its integrated financial management system (IFMS) software. Within each department, there are Budget Controlling Officers and Drawing and Disbursing Officers who are entrusted with the task of executing schemes by controlling and supervising the allotment of funds. Both these officers receive information about the funds placed at their disposal from the Administrative Department. The Drawing and Disbursing Officers are given the authority of drawing funds from the treasury (on behalf of the Government) so that various schemes and activities can be implemented.

Monitoring

Once funds are sanctioned and disbursed, it is necessary to ensure that the funds earmarked for a specific purpose are utilised to that end. This monitoring is done at many levels. Overall, the Finance Department has the responsibility of managing the State’s finances. Other than the Finance Department, the Budget Controlling Officers and the Disbursing Officers are required to ensure the appropriate use of funds. They maintain registers to track expenditure under each item. Every month, the Budget Controlling Officers send a Statement showing the total departmental expenditure and liabilities to the Accountants General. Similarly, the Drawing and Disbursing Officers submit such Statements to the Budget Controlling Officers. Based on these Statements, the Accountants General produces monthly receipt and expenditure Statements for the Finance Department.

Similarly, there is a Management Information System for schemes such as MGNREGA through which reports are produced for the monitoring of these schemes. The Chief Minister’s Office also monitors the implementation of budget announcements through the Chief Minister’s Information System (CMIS).

The Public Finance Management System has also been introduced by the Union Finance Ministry for the monitoring of Central and State Government schemes. There are a number of Dashboards, at various tiers of Governments have been created to monitor physical and financial progress on the implementation of schemes.

Audit

As per Article 150 of the Indian Constitution, the Accountants General (AG) in each State (part of the Office of the CAG of India) is responsible for audits of Government accounts. Such Audits and Accounting have to be practiced to promote accountability and transparency on the part of the State Government. The office of the Accountants General is responsible for the compilation of the monthly accounts of the State Government, inspection of the State’s treasuries, and preparation of different types of accounts such as Appropriation Accounts and Finance Accounts. For the preparation of these reports, information is gathered from the Budget Controlling Officers. These exercises are undertaken soon after the financial year ends, i.e., in early April each year. A final copy of the Appropriation Account is sent to the Finance Department for review. Based on this, the Finance Department prepares another Statement that is submitted to the Finance Minister. In simple terms, the office of the Accountants General is responsible for producing Audit Reports that list various budgetary irregularities in the Appropriation Accounts of the State. The office of the AG also responsible for maintaining the accounting standard of the annual budgets of the State Government.

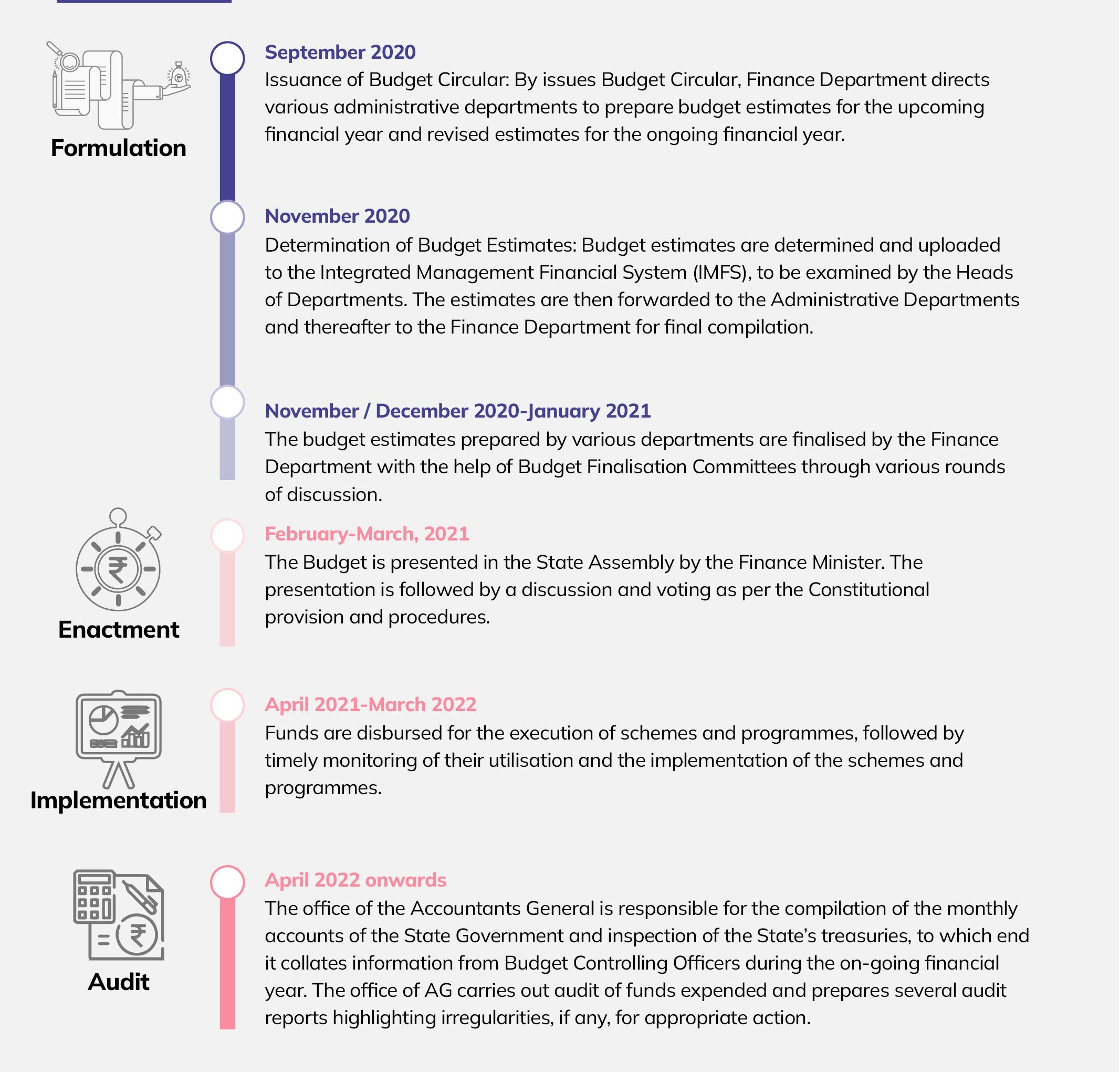

Timeline of The State Budgetary Process

As mentioned in the previous section, the budgetary process is a lengthy and elaborate one and traverses the financial year for which it is made. Figure 2 provides the tentative timeline a State is likely following for its 2021-22 budget.

Figure 2: Different stages of State Budget Processes, 2021-22